July 27th, 2023 by Nikolay Alexandrov

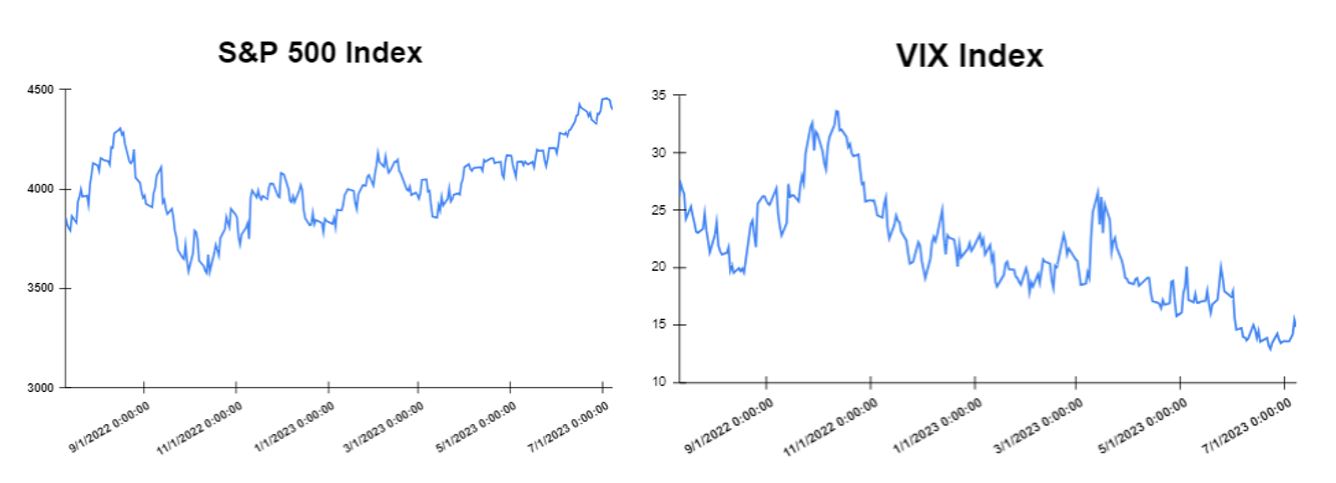

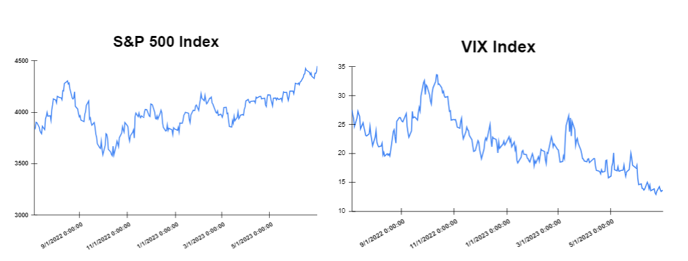

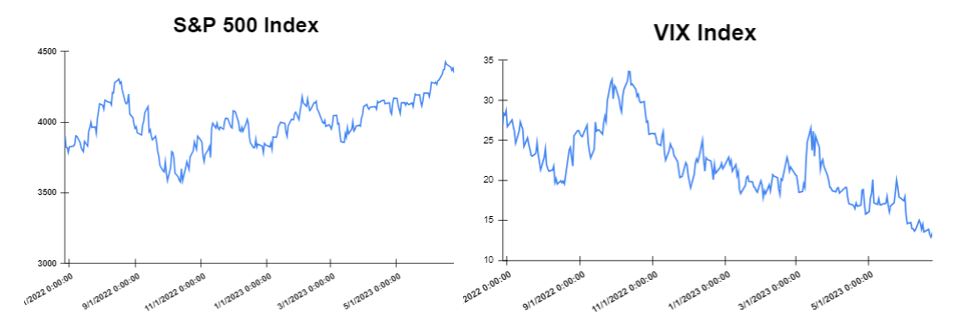

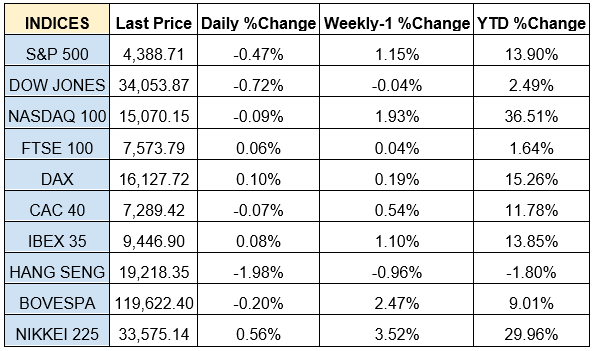

Global markets finished the week almost higher

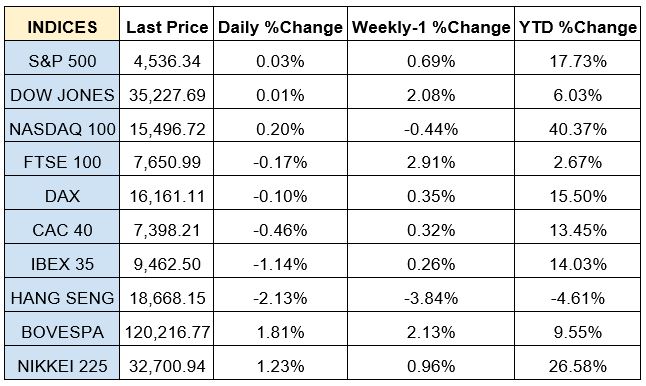

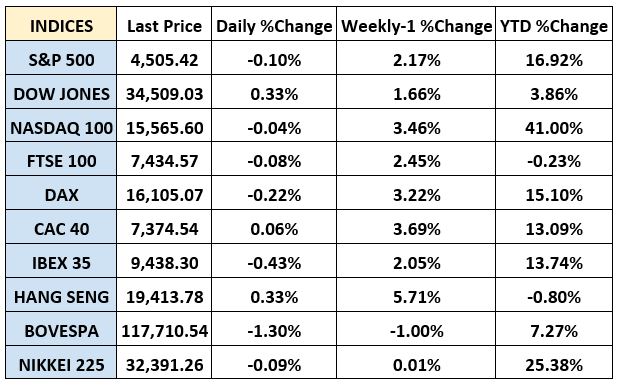

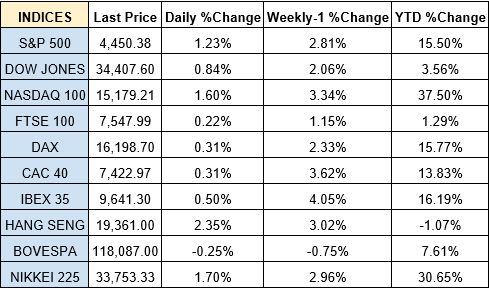

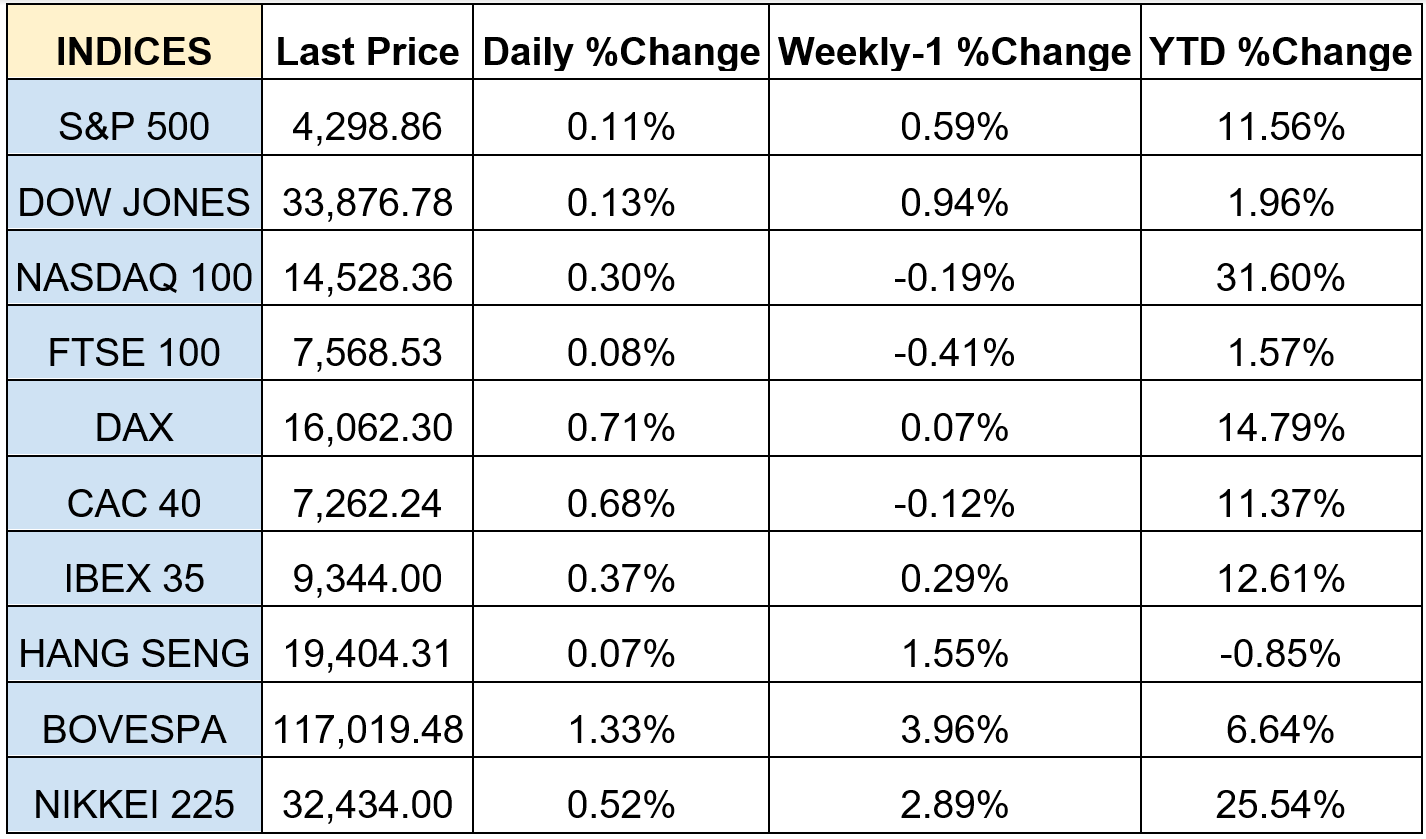

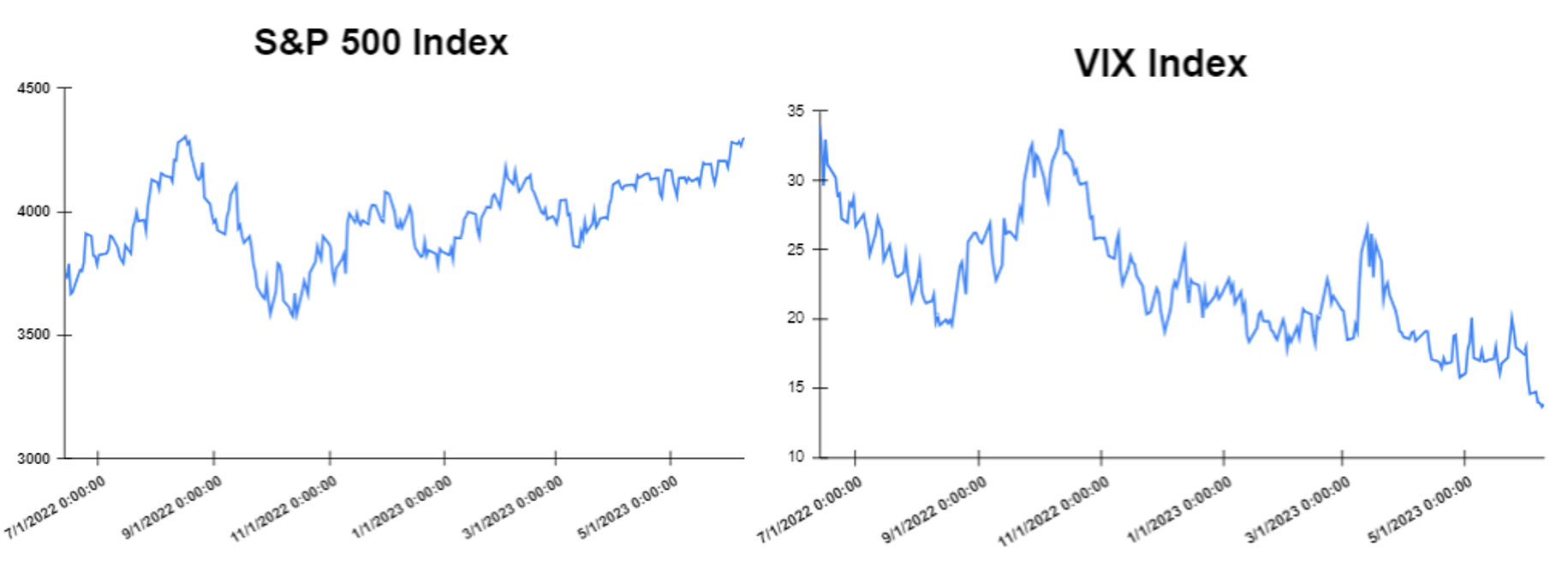

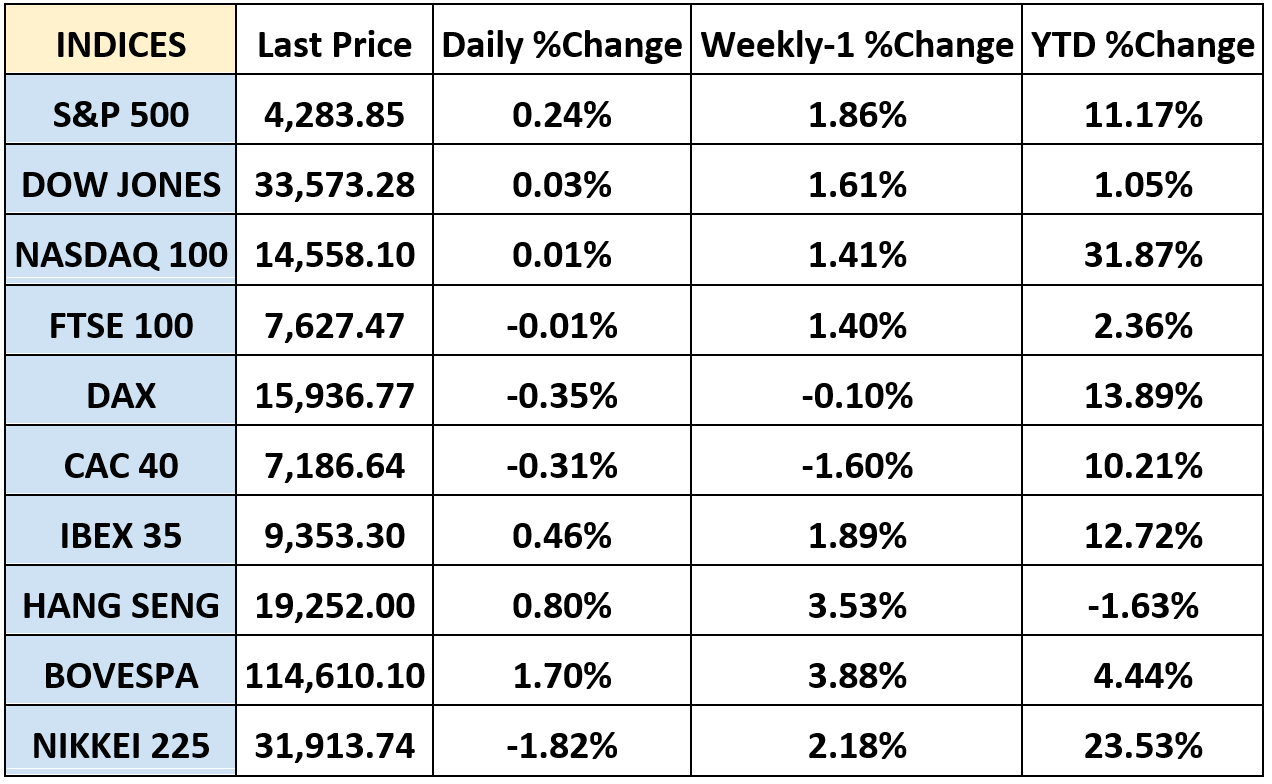

The global markets started the week mixed, , following the massive gains of last week and investors waiting for the incoming economic data. There were not any important data releases on Monday, except for the monthly report of the Deutsche Bundesbank, which showed that the German economy is likely to have recovered slightly in the second quarter of 2023. On Tuesday, the strong earnings gains of the companies turned into gains for the US market. Also, the U.S. retail sales contributed to these gains as they rose less than the forecast for the month of June. On Wednesday, Global markets closed mixed as the annual inflation in the United Kingdom rose by 7.9% on a yearly basis in June. On the same day, the annual inflation rate in the Eurozone (EA20) stood at 5.5% in June, down by 0.6 percentage points compared to the previous month. Also, the U.S. housing data, which are still under the weight of rising interest rates, came in below expectations. On Thursday, the Nasdaq decreased sharply as Tesla and Netflix reported weaker-than-expected Q2 earnings results. Also, the Initial jobless claims in the United States for the week ending July 15 went down by 9,000 compared to the previous week’s revised figure to come in at 228,000. Furthermore, Producer prices in Germany increased by 0.1% year-on-year in June, with the index being 0.3% down in comparison to the previous month. On Friday there were no U.S. economic releases. In Europe, retail sales volumes in the United Kingdom in June rose by 0.7% compared to the month prior. Finally, the Global markets closed almost higher as investors followed a week of data and corporate earnings. The Dow Jones closed flat at the closing bell on Friday. The S&P closed flat. Furthermore, the DAX declined by 0.17% and the CAC 40 jumped by 0.63%. The FTSE 100 gained 0.20%.

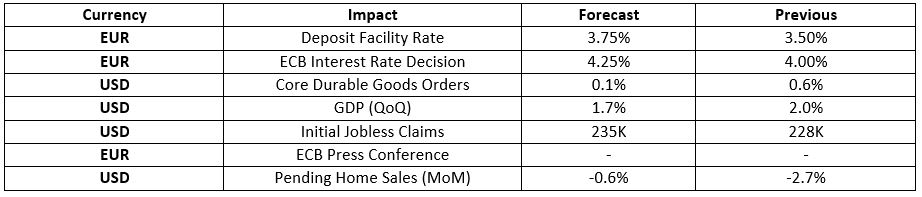

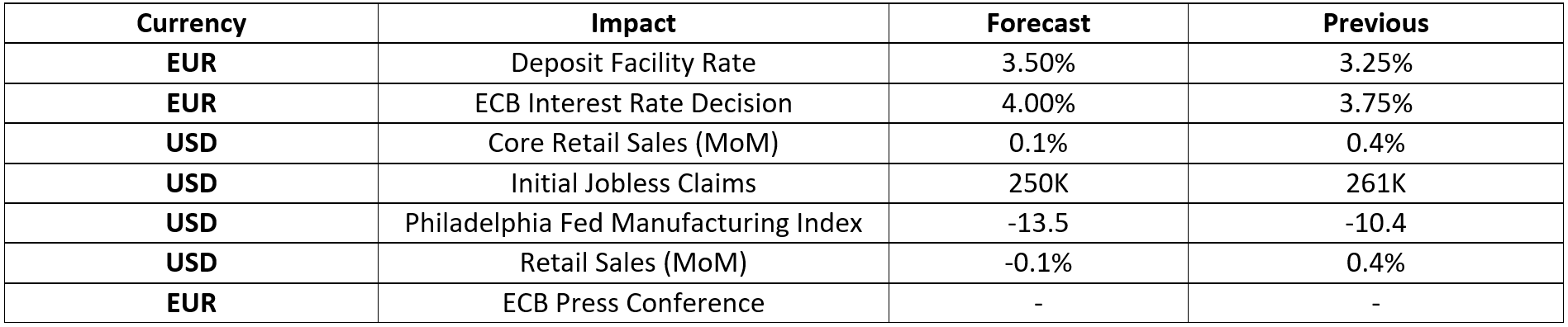

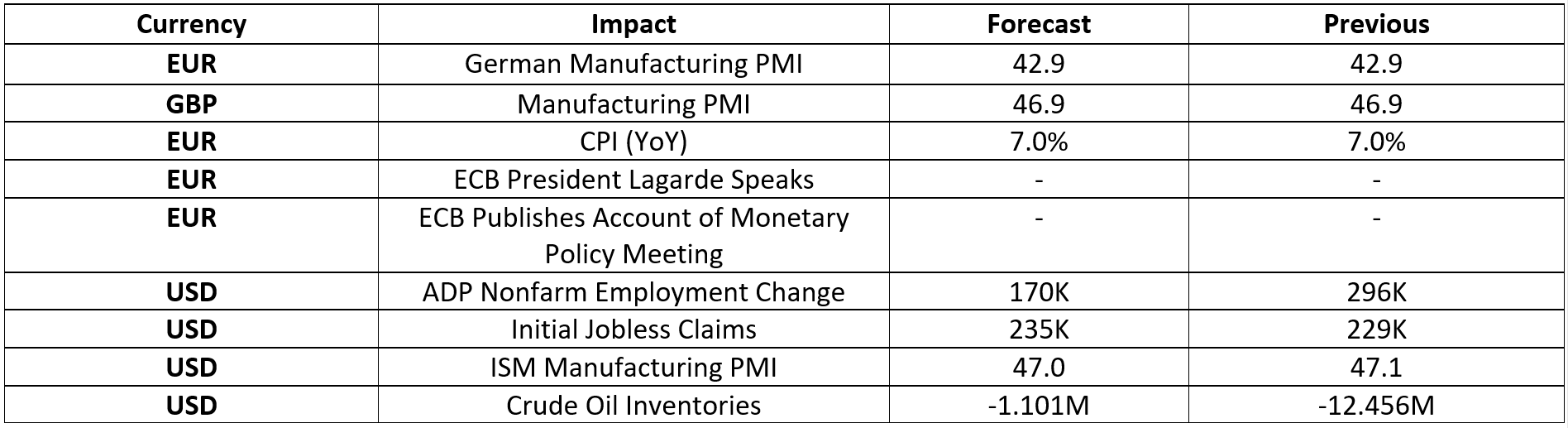

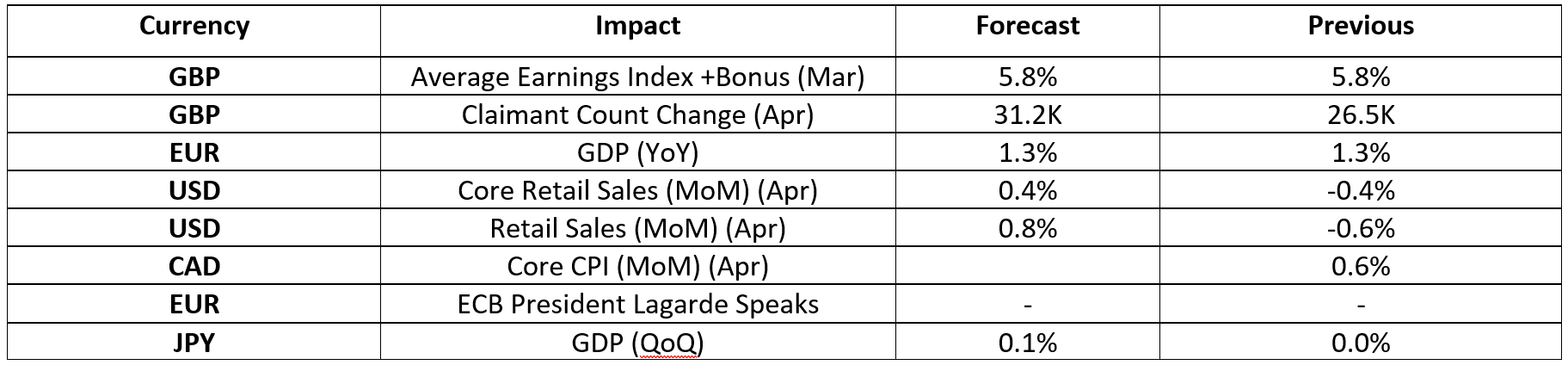

In addition, investors are looking forward to the ECB Interest Rate Decision which is expected to increase to 4.25% from 4.00%

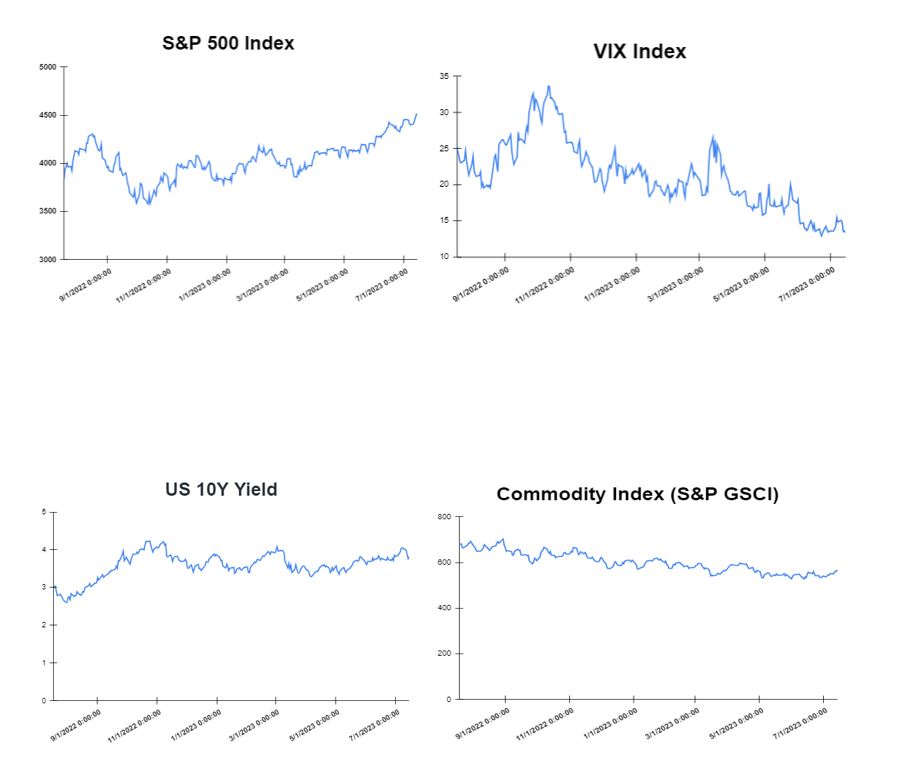

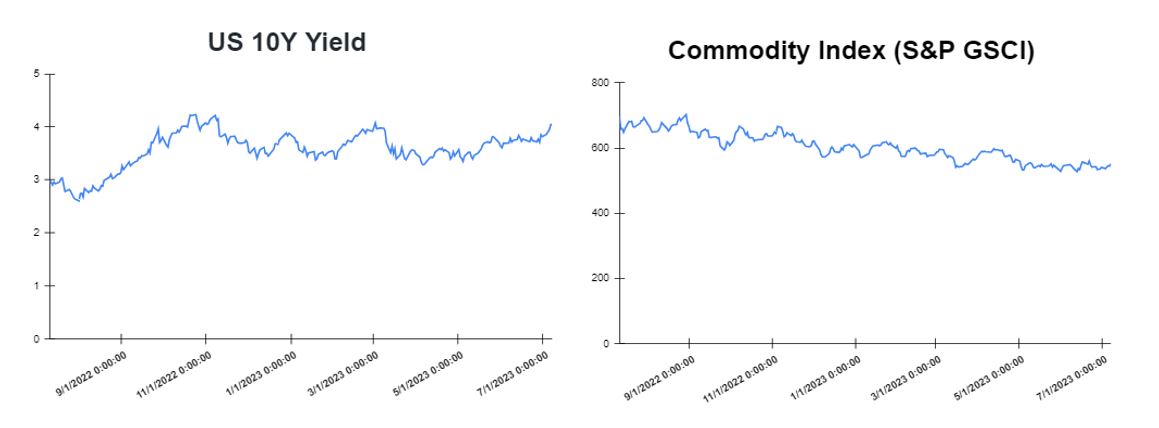

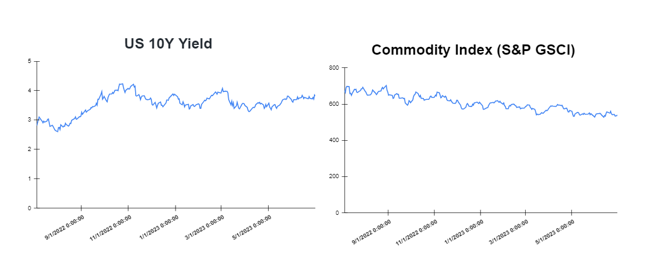

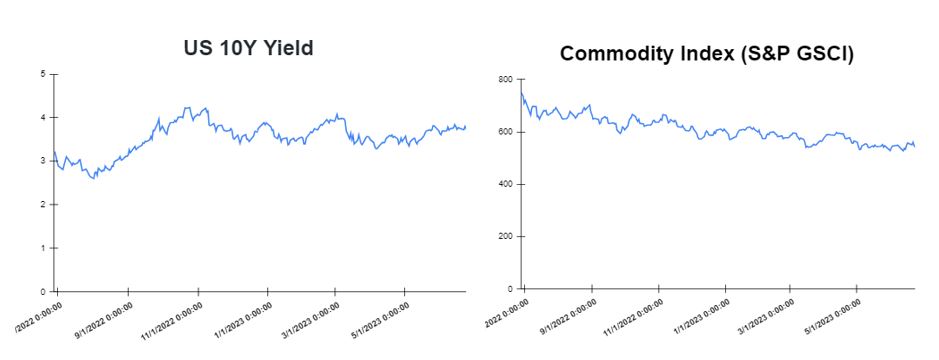

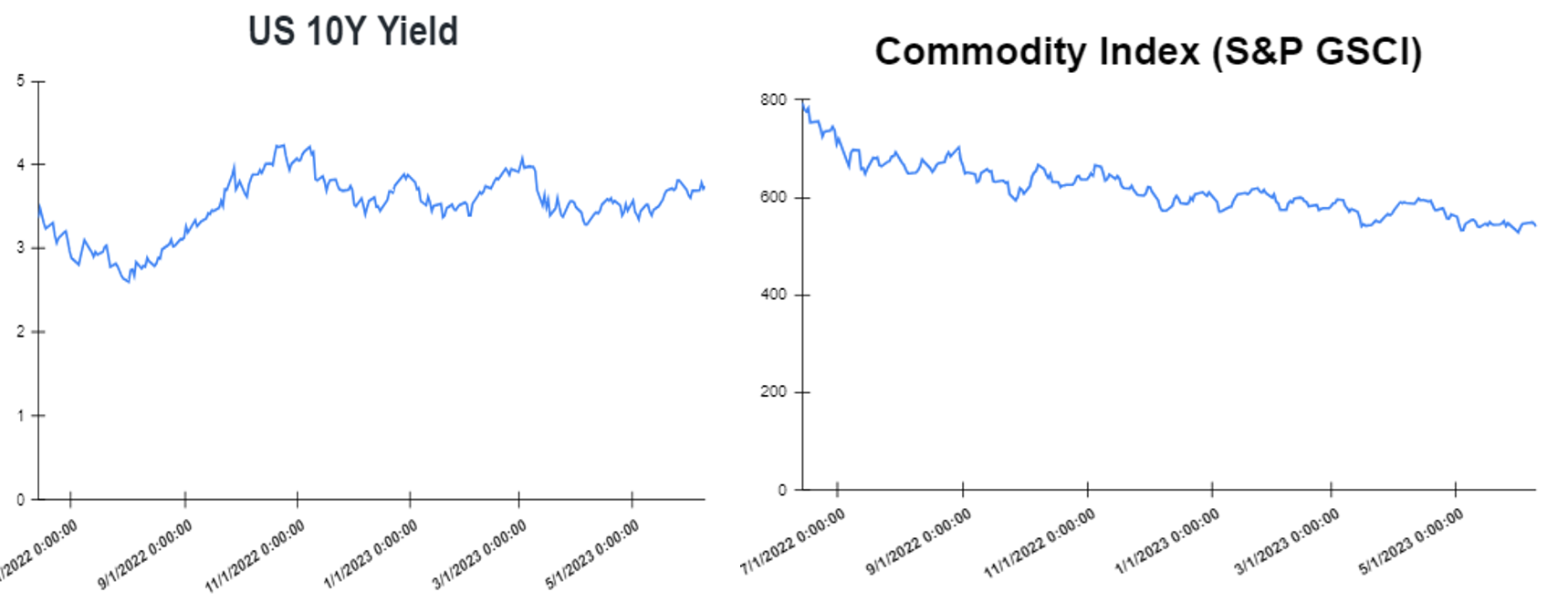

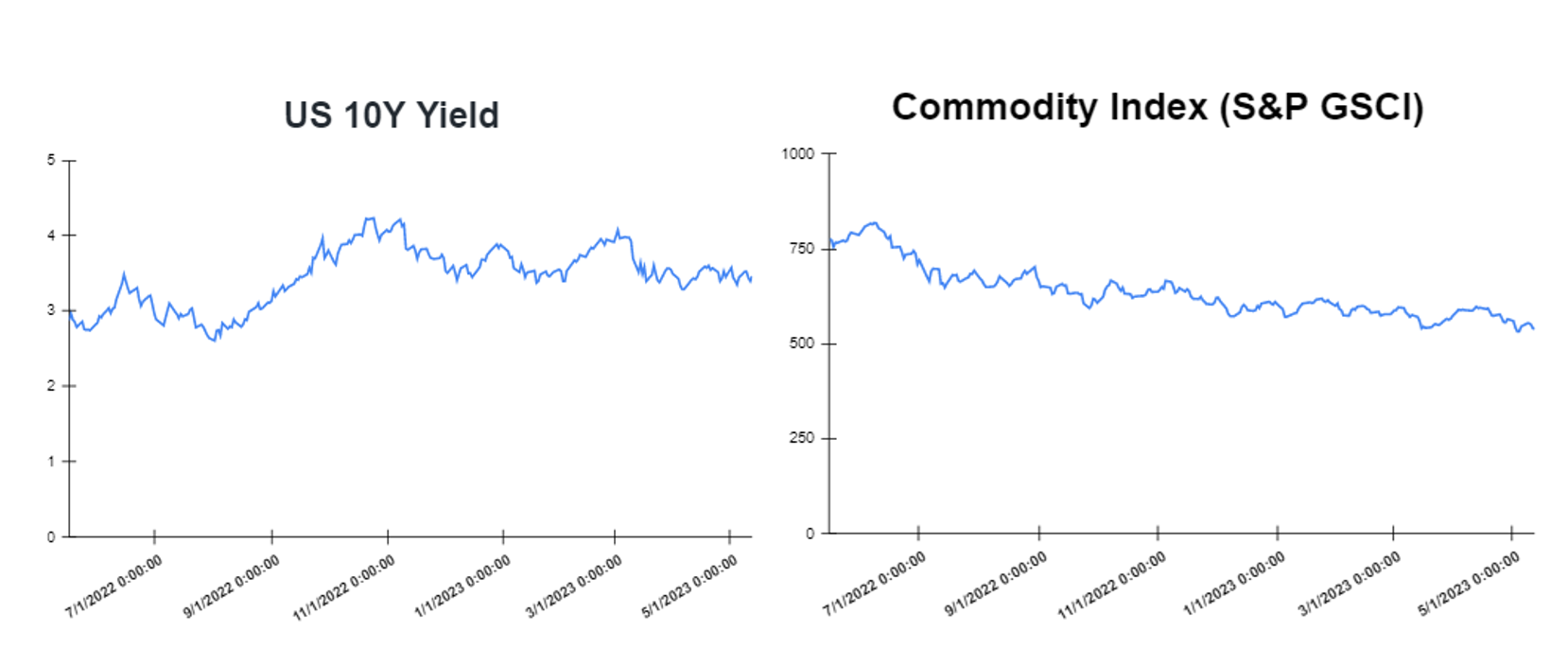

Treasury yields were almost flat towards the end of the week

Yields were higher at the start of the week as investors awaited the economy and monetary policy ahead of a week with few key economic data reports. However, yields moved lower on Wednesday as investors assessed the global economic outlook especially regarding inflation and how it may affect monetary policy after several countries posted their latest inflation figures. On Friday, yields closed the week flat as investors weighed what could be on the horizon for interest rates ahead of the Federal Reserve’s meeting next week. Specifically, on Friday, the yield on the 2-year Treasury decreased to 4.844%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.837%, down by about 2 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.9070%. The spread between the US 2’s and 10’s advanced to -100.7bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) advanced to – 148.0 bps

In addition, investors are looking forward to the Fed Interest Rate Decision which is expected to increase to 5.50% from 5.25%

Volatile week for USD

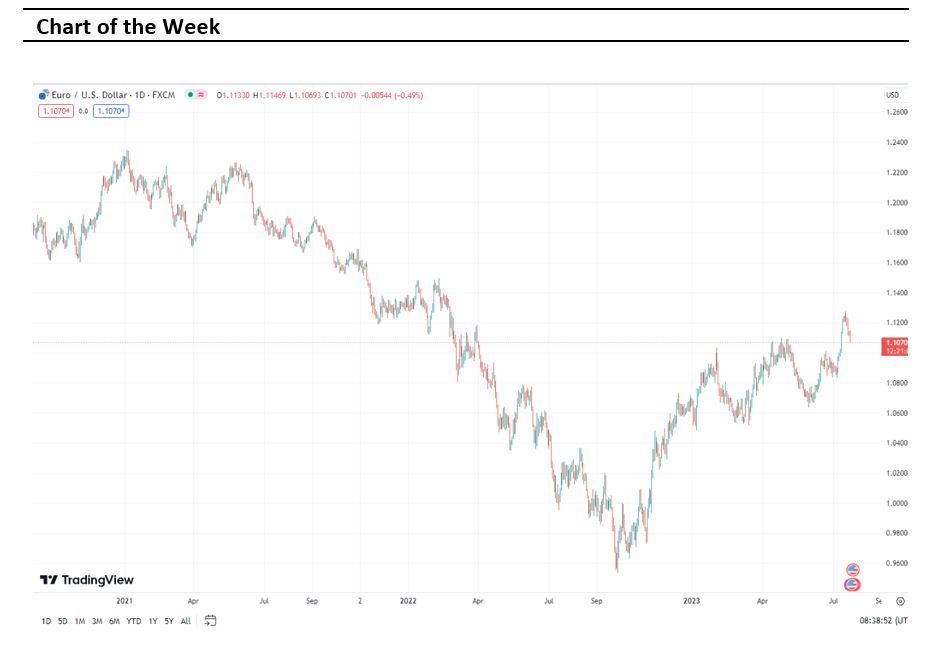

The US Dollar at the start of the week was lower affected by the stronger-than-expected July Empire manufacturing. In the middle of the week the US Dollar advanced as UK Core CPI eased for the first time since January from 7.1% YoY to 6.9% YoY and service inflation fell from 7.4% YoY to 7.2% YoY. However, on Friday, the US dollar finished higher after the sharp decline of the previous week, supported by US economic data. The EURUSD decreased to 1.11, while the GBPUSD decreased to 1.2850. Additionally, the USDJPY increased to 140 Yen on Friday.

Oil and Gold traded mixed towards the end of the week

Gold started the week lower amid a solid recovery in the US Dollar Index (DXY). However, Gold traded lower at the end of the week as investors focus their attention on the Federal Reserve (Fed), which is likely to resume its policy tightening spell next week after skipping in June. On the other hand, oil prices decreased on Monday as supply pressures seemingly eased following media reports that oil production in Libya will partially resume following the protests last week that forced the closure of three key oilfields. However, oil finished higher at the end of the week, as supply woes seemingly continued to dominate the crude market sentiment. Meanwhile, this week’s report by the United States Energy Information Administration showed that the crude oil inventories in the country declined by 700,000 barrels. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show a decrease of 1.692M.

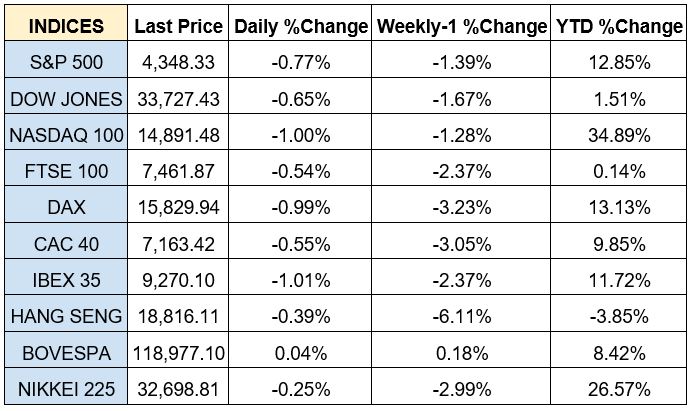

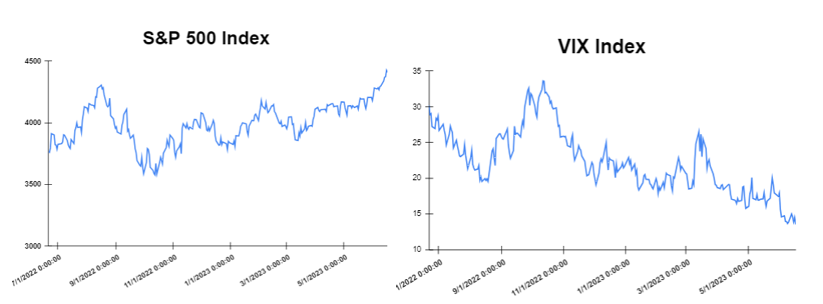

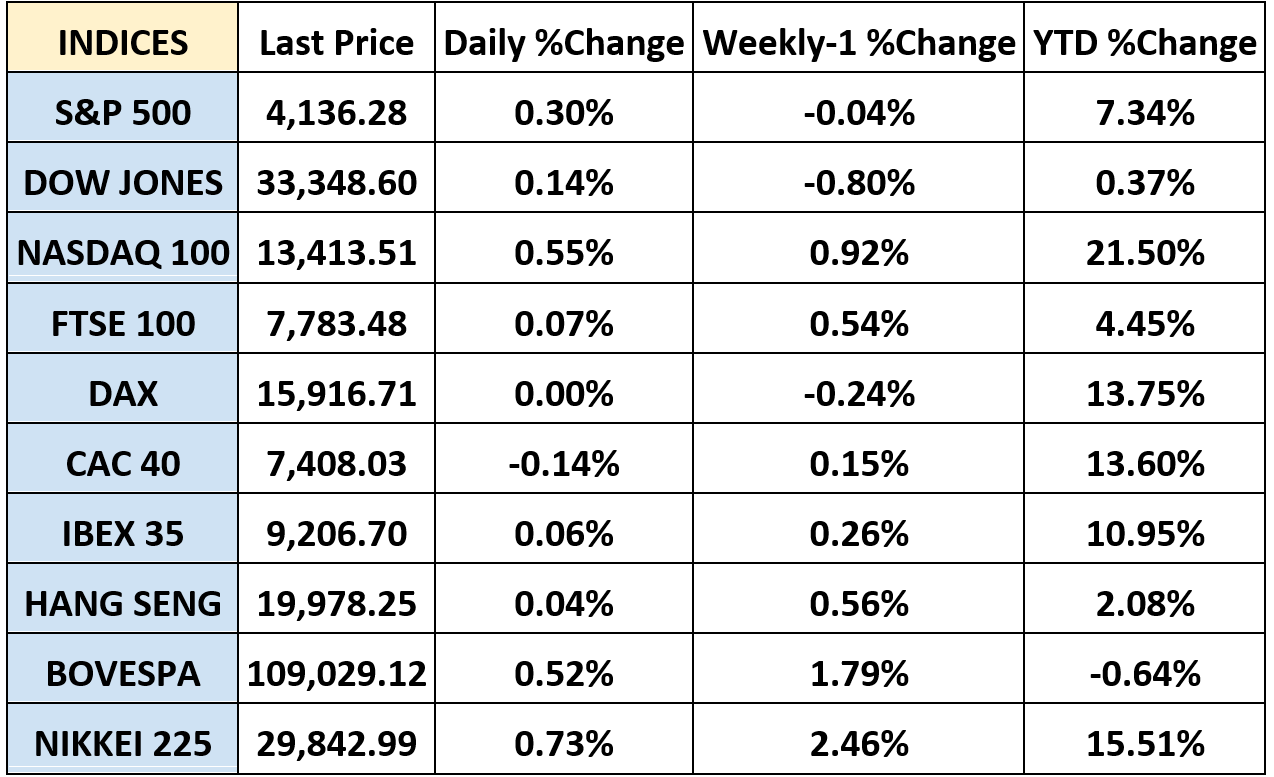

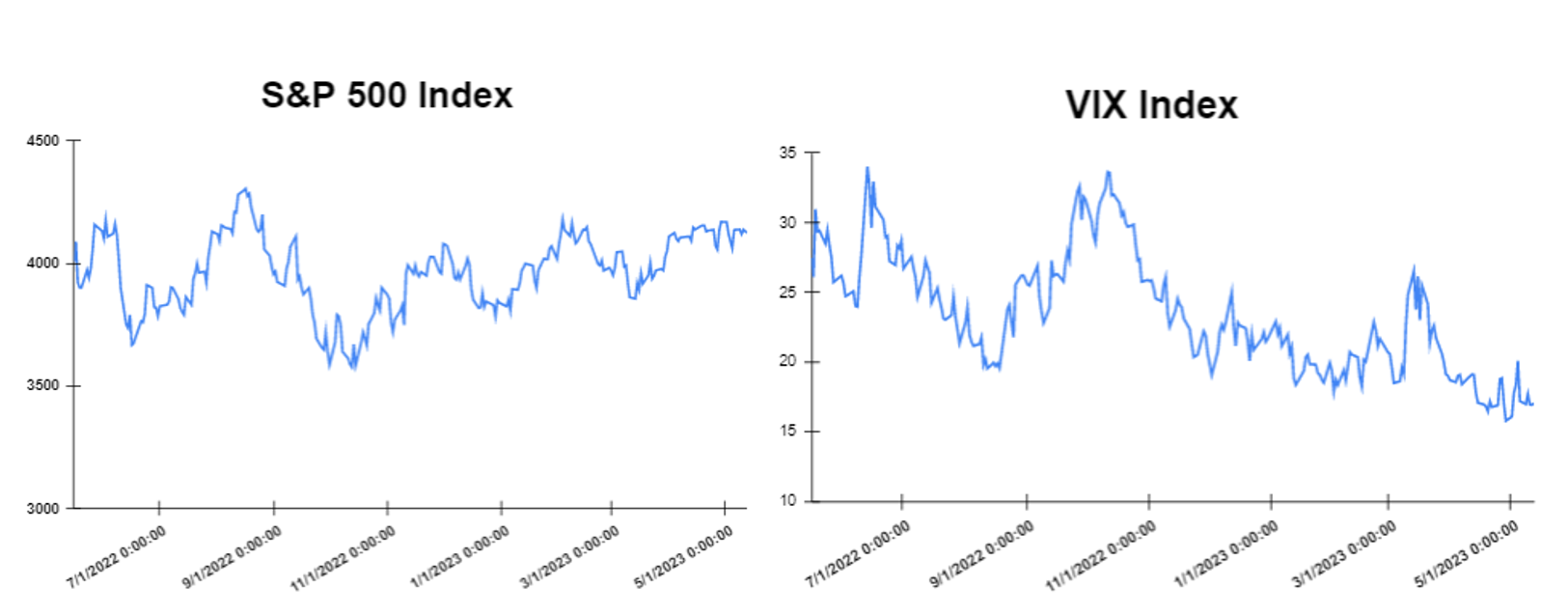

Stock indices performance

Key weekly events:

Monday -24 July 2023

Tuesday – 25 July 2023

Wednesday – 26 July 2023

Thursday – 27 July 2023

Friday – 28 July 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

July 18th, 2023 by Nikolay Alexandrov

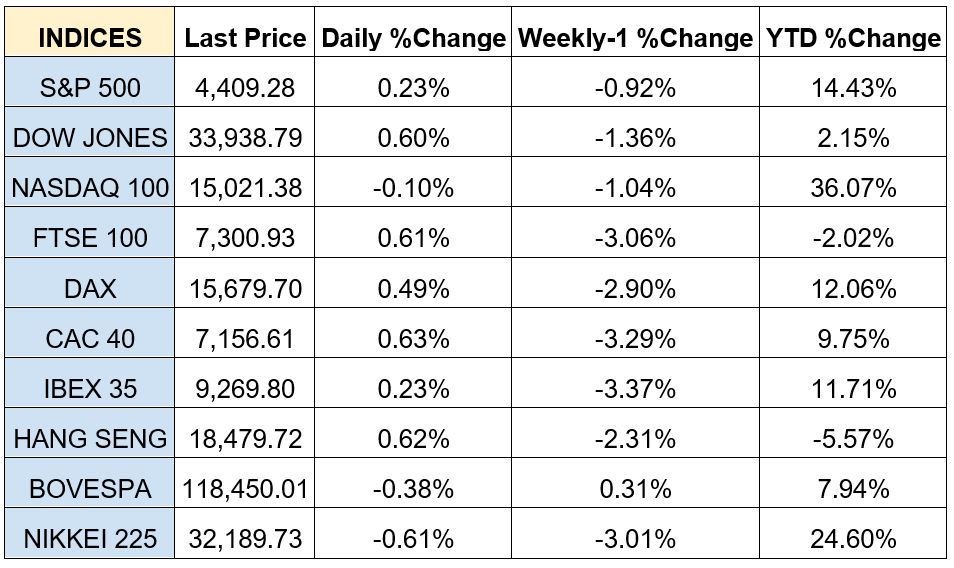

Global markets finished the week mixed

The global markets started the week higher as investors are waiting for the incoming economic data. On Tuesday, the unemployment rate in the United Kingdom clocked in at 4% in May, going up 0.2 percentage points in comparison to the previous month. On Wednesday, Global markets closed sharply higher as the annual inflation in the United States stood at 3.0% in June, going down from the4.0% registered in May and coming in slightly lower than analysts forecast. On Thursday, the gross domestic product (GDP) of the United Kingdom shrank by0.1% in May compared to the previous month. On the same day, the Producer Price Index (PPI) for final demand in the United States increased by 0.1% in June compared to the previous month. Following the above news, the Global market closed with strong gains on Thursday. On Friday the Global markets closed mixed as investors are waiting for the new economic data including those on the Eurozone and the United Kingdom’s inflation and Germany’s producer prices. Moreover, on the same day, the Consumer Sentiment Index in the United States observed a monthly rise of 12.7% in July hitting 72.6 points, its highest level since September 2021. The Dow Jones closed with a gain of 0.33% at the closing bell on Friday. The S&P fell by 0.10%. Furthermore, the DAX declined by 0.22% and the CAC 40 jumped by 0.13%. The FTSE 100 stood flat.

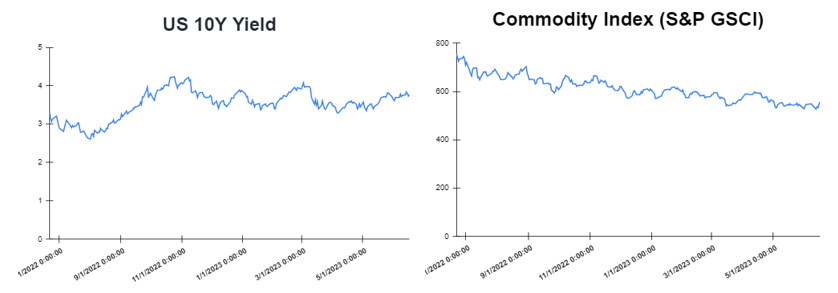

Treasury yields were advanced towards the end of the week

Yields were higher at the start of the week as investors awaited the latest comments from U.S. Federal Reserve officials and key inflation data due this week. However, yields moved lower on Wednesday after the inflation report in June showed an easing in prices. The consumer price index increased by 3% from a year ago, which is the lowest level since March 2021. On Friday, yields closed the week higher reversing some of the sharpest declines seen over the last two sessions on the back of cooler-than-expected consumer and wholesale inflation prints. Specifically, on Friday, the yield on the 2-year Treasury decreased to 4.738%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.811%, growing by about 5 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.9240%. The spread between the US 2’s and 10’s advanced to -92.7bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) advanced to – 135.4 bps

In addition, investors are looking forward to the Europe and Great Britain inflation (CPI) data expecting a decrease

Volatile week for USD

The US Dollar at the start of the week was lower affected by data reflecting lower inflation expectations and on the back of a decline in US Treasury yields. In the middle of the week the US Dollar declined as inflation data from the US led to sharp market moves. However, on Friday, the US dollar finished lower suffering its worst weekly loss since November of last year, falling below 100.00, to the lowest since April 2022. The Greenback remains vulnerable in the context of risk appetite and lower Treasury yields. The EURUSD increased to 1.18, while the GBPUSD increased to 1.31. Additionally, the USDJPY decreased to 137 Yen on Friday.

Oil and Gold traded mixed towards the end of the week

Gold started the week higher as investors were shifting their focus towards the United States Consumer Price Index (CPI) after the impact of the Nonfarm Payrolls (NFP) report. However, Gold traded higher at the end of the week sticking to near one-month highs as softer-than-expected U.S. inflation data saw investors reassess just how much further U.S. interest rates will rise. On the other hand, oil prices decreased on Monday after the newest report on China’s annual inflation in June showed no change compared to the previous month. However, oil finished lower at the end of the week, as the dollar strengthened and oil traders booked profits from a strong rally, with crude benchmarks recording their third-straight weekly gain. Meanwhile, Russia reiterated its intention to reduce its output by 500,000 barrels per day (bpd) in August by delivering fewer exports. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show a decrease of 6.851M.

Stock indices performance

Key weekly events:

Tuesday – 18 July 2023

Wednesday – 19 July 2023

Thursday – 20 July 2023

Friday – 21 July 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

July 14th, 2023 by Nikolay Alexandrov

Global markets finished the week mixed

The global markets started the week mixed after the big gains on Friday’s session. The US markets closed early on Monday ahead of the 4th of July holiday. Also, on the same day, the ISM’s manufacturing purchasing managers’ index for June came in slightly worse than expected in the US, signalling that economic activity was declining. On Wednesday, the European markets closed mostly lower as producer prices (PMI) in the Eurozone decreased by 1.9% in May compared to the month before. Furthermore, the Fed officials at their June meeting, noted that a decline in the country’s inflation is slower than expected and that additional hikes in interest rates will be appropriate. On Thursday, United States private payrolls soared by 497,000 in June, well above forecasts with a result of potential further raises by the Federal Reserve’s in interest rates. Following the above news, the US market closed lower on Thursday. On Friday the Global markets closed with gains after the release of the latest United States nonfarm employment data, which showed that employment grew less than expected in June. Specifically, the June employment report increased by 209,000 and the unemployment rate stood at 3.6%, down by 0.1 percentage points from the previous month. Moreover, on the same day, the annual rate of house price growth in the United Kingdom came in at negative 2.6% in June. The Dow Jones closed with a loss of 0.55% at the closing bell on Friday. The S&P fell by 0.28%. Furthermore, the DAX increased by 0.48% and the CAC 40 jumped by 0.42%. The FTSE 100 decreased by 0.32%.

Treasury yields were mixed towards the end of the week

Yields were higher in the middle of the week as investors absorbed the release of the Federal Reserve’s latest meeting minutes. However, yields moved up on Thursday after reaching a level not seen in 16 years as investors absorbed strong jobs data that could mean further tightening from the Federal Reserve. ADP’s employment report showed private sector jobs jumped by 497,000 in June, far above the 220,000 Dow Jones consensus estimate. It was also greater than the 267,000 gain in May. On Friday, yields closed the week mixed as the slightly weaker-than-expected increase in June payrolls failed to dissuade traders from betting on more rate hikes. Specifically, on Friday, the yield on the 2-year Treasury decreased to 4.937%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 4.062%, growing by about 2 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 4.03%. The spread between the US 2’s and 10’s declined to -87.5bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) declined to – 133.5 bps. In addition, investors are looking forward to US inflation data report on Wednesday, 12 of July, in which a decrease of 0.9% is expected.

Volatile week for USD

The US Dollar at the start of the week was lower following the release of the ISM Manufacturing PMI, which came in below expectations. In the middle of the week the US Dollar advanced as US yields rose, supporting the US Dollar. The DXY rose for the third day. However, on Friday, the US dollar finished lower as the June employment report showed a slowdown in nonfarm employment growth, seemingly leading investors to believe that the inflation picture could improve and the Federal Reserve will not have to raise interest rates aggressively anymore. The EURUSD increased to 1.095, while the GBPUSD increased to 1.2833. Additionally, the USDJPY decreased to 142.24 Yen on Friday.

Oil and Gold traded higher towards the end of the week

Gold started the week higher following the release of weaker-than-expected US economic data. However, Gold traded higher at the end of the week following a softer-than-expected U.S. jobs report for June suggesting some tempering in the Fed’s hawkishness when the central bank’s policy-makers sit for their next rate review in three weeks. On the other hand, oil prices decreased on Monday after two data reports pointed to a continued downturn in the United States manufacturing sector. However, oil finished at the end of the week with strong gains, after the report on the United States oil rigs counts showed a weekly decrease of 5 rigs. Meanwhile, Russia reiterated its intention to reduce its output by 500,000 barrels per day (bpd) in August by delivering fewer exports. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show a decrease of 0.648M.

Stock indices performance

Key weekly events:

Tuesday – 11 July 2023

Wednesday – 12 July 2023

Thursday – 13 July 2023

Friday – 14 July 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

July 7th, 2023 by Nikolay Alexandrov

Global markets finished the week higher

The global markets started the week mostly lower. On Monday, a survey showed that the business climate in Germany continued to deteriorate in June. The business climate index fell to 88.5, down from 91.7 in May and lower than forecasts suggested. On Tuesday, the markets closed on positive territory, as several economic releases, like durable goods orders, consumer confidence, and new home sales, all came in better than expected. On Wednesday, the European markets closed higher with the ECB President Christine Lagarde reaffirming further rate hikes lie ahead. Furthermore, Federal Reserve Chair Jerome Powell continued to insist that further rate hikes likely lie ahead. On Thursday, Germany’s annual rate of consumer inflation accelerated in June compared to the previous month to reach a higher-than-expected 6.4%. Furthermore, annual inflation in Spain stood at 1.9% in June, down from 3.2% in the previous month. Meanwhile, the United States gross domestic product (GDP) increased by 2% in the first quarter, higher than estimates and the weekly jobless claims fell to 239,000, lower than expected. Following the above news, the global market closed broadly higher on Thursday. On Friday the European markets closed with strong gains after annual inflation in the euro area ran at 5.5% in June, down from last month’s figure of 6.1%. Moreover, on the same day, the UK’s gross domestic product (GDP) came in in-line with initial projections, growing by 0.1% during the opening quarter of 2023, while the US personal consumption expenditure (PCE) inflation metrics came in also in-line with expectations for the month of May. Finally, the global stock markets ended the week higher, after a week full of important economic data and financial updates. The Dow Jones closed with a gain of 0.84% at the closing bell on Friday. The S&P rose by 1.23%. Furthermore, the DAX increased by 1.26% and the CAC 40 jumped by 1.19%. The FTSE 100 increased by 0.80%.

In addition, investors are looking forward to the Europe inflation (CPI) data expecting a decrease to 5.6% from 6.1%.

Treasury yields were mixed towards the end of the week

Yields started the week lower as investors awaited commentary from Federal Reserve speakers. However, yields moved up on Thursday after the stronger-than-expected economic data, which showed that the Fed will keep interest rates higher for longer. On Friday, yields closed the week mixed as the latest personal consumption expenditure price index data showed signs of easing inflation. Specifically, on Friday, the yield on the 2-year Treasury increased to 4.902%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.841%, declining by about 1 basis point. The 30-year Treasury yield, which is key for mortgage rates, hit 3.8540%. The spread between the US 2’s and 10’s advanced to -106.1bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) advanced to – 145.5 bps. In addition, investors are looking forward to the US Nonfarm Payrolls report on Friday, 7 of July, in which a decreased of 114K is expected.

Volatile week for USD

The US Dollar at the start of the week was lower as investors await new data and speeches from central bankers from the European Central Bank (ECB). In the middle of the week the US Dollar advanced as Powell hinted at several more rate hikes from the Fed over the summer. However, on Friday, the US dollar finished lower after economic data showed a cooling in consumer spending, raising some doubt about the potential aggressiveness of the Federal Reserve in fighting inflation. The EURUSD increased to 1.0911, while the GBPUSD increased to 1.2695. Additionally, the USDJPY decreased to 144.26 Yen on Friday.

Oil and Gold traded higher towards the end of the week

Gold started the week higher as investors looked for safer bets after the turmoil in Russia over the weekend which sparked new geopolitical concerns. However, Gold traded higher at the end of the week following the soft Personal Consumer Expenditures from the US, which fuelled a decline in US yields and, thereby, a weaker US Dollar, which boosted the yellow metal. On the other hand, oil prices for front-month deliveries climbed over 1% on Monday after OPEC Secretary General Haitham Al Ghais revealed that the commodity demand is expected to expand by 23% to 110 million barrels per day by 2045. Also, oil continued to move higher at the end of the week, after softer U.S. inflation data suggested that the Federal Reserve could be a little restrained in its hawkish talk to rein in price growth via rate hikes. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show an increase of 8.874M.

Stock indices performance

Key weekly events:

Key weekly events:

Monday – 03 July 2023

Tuesday – 04 July 2023

Wednesday – 05 July 2023

Thursday – 06 July 2023

Friday – 07 July 2023

Sources:

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

June 28th, 2023 by Nikolay Alexandrov

Global markets finished the week lower

The global markets started the week lower, after a strong gain last week. On Tuesday, the Producer prices in Germany rose by 1% on an annual basis in May, making this “the smallest increase since January 2021. Month on month, the reading declined by 1.4%. Also, the Housing starts in tge US, which is a leading indicator of economic health, increased in May with 1.63 million new homes starting construction, while the building permits were 1.49 million in May, up from 1.42 million in April. On Wednesday, the European markets were moderately lower after the UK’ Consumer Price Index increased more than expected, by 8.7% year over year and by 0.7% on a monthly basis in May. Furthermore, Federal Reserve Chair Jerome Powell continued to insist that further rate hikes likely lie ahead. On Thursday, the Bank of England surprised markets by increasing its key rate by the more-than-expected 50 basis points and bringing it to 5%. Meanwhile, the Fed Chair Powell hinted at two more rate increases this year, while the US initial jobless claims were 264,000, the same as the prior week and slightly above expectations. On Friday the Europe markets moved lower after the disappointing results in the private sector activity across the continent. Specifically, the HCOB Flash Eurozone PMI Composite Output Index, which measures the services and the manufacturing business activity, stood at 50.3 in June, representing a decrease of 2.5 index points compared to the previous month and landing at a five-month low. Also, on the same day, the US PMI index, reached 53.0 in June, down from 54.3 registered a month prior, raising concerns about the economic stability in the country. Finally, the global stock markets ended the week lower, after a week full of important economic data and financial updates. The Dow Jones closed with a loss of 0.64% at the closing bell on Friday. The S&P declined by 0.76%. Furthermore, the DAX decreased by 0.99% and the CAC 40 fell by 0.55%. The FTSE 100 declined by 0.54%.

In addition, investors are looking forward to the Europe inflation (CPI) data expecting a decrease to 5.6% from 6.1%.

Treasury yields declined towards the end of the week

Interest rates started the week lower with the 10-year Treasury yields moving below 3.75%. On Thursday, the yields climbed higher after Powell noted that two more rate hikes in 2023 are likely. However, yields closed the week lower on Friday as investors digested remarks from FED officials about the outlook for interest rates and the latest economic data. Specifically, on Friday, the yield on the 2-year Treasury decreased to 4.750%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.735%, declining by about 6 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.82%. The spread between the US 2’s and 10’s advanced to -101.5bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) advanced to – 137.9 bps. In addition, investors are looking forward to the GDP data which is expected to decrease to 1.4% from 2.6%.

Volatile week for USD

The US Dollar at the start of the week was higher as investors were focused on Federal Reserve Chairman Jerome Powell’s testimony before Congress. In the middle of the week the US Dollar declined as US Treasury yields declined. However, on Friday, the US dollar finished higher after Fed Powell’s comments about more rate hikes. The EURUSD decreased to 1.090, while the GBPUSD declined to 1.27. Additionally, the USDJPY increased to 144.00 Yen on Friday to monthly highs.

Oil and Gold traded opposite towards the end of the week

Gold started the week lower due to the People’s Bank of China (PBoC) announcement about cutting its interest rates by ten basis points and loosening its monetary policy. However, Gold traded higher at the end of the week after Federal Reserve Bank of Atlanta President Raphael Bostic shared that he would not be supporting further interest rate increases in 2023. On the other hand, prices of Oil moved higher at the start of the week after the People’s Bank of China cut its main interest rates by 10 basis points. However, at the end of the week oil moved lower, after concerns about the commodity’s demand. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show an increase of 5.246M.

Stock indices performance

Key weekly events:

Tuesday – 27 June 2023

Wednesday – 28 May 2023

Thursday – 29 June 2023

Friday – 30 June 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

June 23rd, 2023 by Nikolay Alexandrov

Global markets finished the week mixed

The global markets started the week higher, as investors were waiting for the reports on inflation in Germany, but also in the United States, and unemployment in the United Kingdom. Moreover, on Tuesday, Consumer prices in Germany rose to 6.1% in May as expected compared to the same month a year earlier but the figure marks a decline from April when inflation stood at 7.2%. Furthermore, the unemployment rate in the United Kingdom went up by 0.1 percentage point in the trimester to April compared to the previous quarter to land at 3.8%, marginally lower than market expectations. On the same day, the annual inflation in the United States came in at 4.0% in May, declining from the 4.9% registered in April and standing slightly lower than analysts predicted. On Wednesday, the United Kingdom’s gross domestic product (GDP) rose by 0.2% in April. According to the report, the GDP increased by 0.1% in the three months to April 2023. Furthermore, United States Federal Reserve’s Federal Open Market Committee (FOMC) announced on Wednesday that it has unanimously decided to suspend its interest rate increases in June, after 10 straight hikes, and leave the federal funds rate at 5.25%. Following the above news, the global market closed mix on Wednesday. The European Central Bank decided on Thursday to raise its three key interest rates for the eighth time in a row, this time by 25 basis points. Also, on the same day, the number of seasonally adjusted initial jobless claims in the United States remained unchanged at 262,000 in the week ending June 10. On Friday, the annual inflation in the euro area clocked in at 6.1% in May, while the monthly rate remained unchanged. Finally, the global stock markets ended the week mixed, after a week full of important economic data and financial updates. The Dow Jones closed with a loss of 0.32% at the closing bell on Friday. The S&P declined by 0.37%. Furthermore, the DAX rose by 0.54% and the CAC 40 increased by 1.34%. The FTSE 100 rose by 0.19%. In addition, investors are looking forward to the BoE Interest Rate Decision expecting an increase to 4.75% from 4.50%.

Treasury yields advanced towards the end of the week

Yields started the week lower as investors braced themselves for the latest inflation data and the Federal Reserve’s next policy meeting and interest rate decision. However, yields closed the week higher on Friday as investors considered the path ahead for interest rates and awaited data that could provide hints about the state of the economy. Specifically, on Friday, the yield on the 2-year Treasury increased to 4.720%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.769%, advanced by about 4 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.8560%. The spread between the US 2’s and 10’s advanced to -95.1bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) declined to – 134.8 bps.

Volatile week for USD

The US Dollar at the start of the week was higher as investors were waiting for upcoming important economic data. In the middle of the week the US Dollar declined as the Federal Reserve kept its interest rate unchanged. On Friday, the US dollar finished lower after having the worst week in months as US data showed that inflation continues to slow down. The EURUSD increased to 1.090, while the GBPUSD increased to 1.28 climbing for the third consecutive week and reaching the highest levels since April 2022. Additionally, the USDJPY increased to 141.5 Yen on Friday.

Oil and Gold traded opposite towards the end of the week

Gold started the week lower due to caution ahead of upcoming U.S. consumer inflation data and a Federal Reserve meeting. However, Gold traded lower at the end of the week as bond yields moved higher. Prices of Oil moved lower at the start of the week as the unpredictability concerning the United States Federal Reserve’s latest decision on interest rates scheduled for this week seemingly discouraged investors. However, at the end of the week oil moved higher, as higher Chinese demand and OPEC+ supply cuts lifted prices, despite an expected weakness in the global economy and the prospect for further interest rate hikes. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show a decrease of 6.046M.

Stock indices performance

Key weekly events:

Tuesday – 20 June 2023

Wednesday – 21 May 2023

Thursday – 22 June 2023

Friday – 23 June 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/

https://www.investing.com/

https://www.fxstreet.com/

https://www.cnbc.com/world/

June 15th, 2023 by Nikolay Alexandrov

Global markets finished the week mixed

The global markets started the week lower, after data showed that the services sector in the United States expanded at a slower pace, adding to concerns about the stability of the country’s economic condition. Also on Monday, the Purchase Managers’ Index (PMI) came in at 50.3%, 1.6 percentage points lower than in April and slightly lower than expected, signalling a slowdown in the growth of the US services sector. On the same day, the private sector activity in the United Kingdom (PMI) softened in May, led by a drop in manufacturing production, declining to 54 from 54.9 in April. Moreover, on Wednesday, the Bank of Canada announced that it has decided to raise its key interest rate by 25 basis points to 4.75% while stating that it will continue with its policy of quantitative tightening. Furthermore, House prices in the United Kingdom decreased by 1% in May, on an annual basis, according to the Halifax House Price Index report on Wednesday, with the reading being negative for the first time since December 2012. On Thursday, the GDP growth was revised down to 1%, on a yearly basis, both in the Eurozone and in the EU from 1.3% and 1.2% respectively. Also, on the same day, the number of seasonally adjusted initial jobless claims in the United States jumped by 28,000 to 261,000, more than expected and this was the highest level since October 2021. Lastly, on Friday, the stock markets ended the week mixed, leaving markets to focus on upcoming inflation and Fed announcements. On June 14, the Fed will announce its interest rate decision and most traders seem to be expecting a pause in the rate-hiking process. Moreover, the European stocks ended Friday’s session in the red territory following Thursday’s news from Eurostat that the Eurozone’s economy entered recession at the start of the year. The Dow Jones closed with a gain of 0.13% at the closing bell on Friday. The S&P jumped by 0.11%. Furthermore, the DAX declined by 0.25% and the CAC 40 dropped by 0.12%. The FTSE 100 lost 0.49%.

In addition, investors are looking forward to the ECB Interest Rate Decision expecting an increase to 4.00% from 3.75%. while the Fed is expected to keep the interest rates at 5.25%.

Treasury yields advanced towards the end of the week

Yields started the week lower as investors monitored the path for interest rates and weighed key economic data that could affect the Federal Reserve’s next policy moves. However, yields closed the week higher on Friday after looking ahead to the Federal Reserve monetary policy meeting next week, where officials will announce a fresh interest rate decision. Specifically, on Friday, the yield on the 2-year Treasury increased to 4.606%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.747%, advanced by about 3 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.8870%. The spread between the US 2’s and 10’s advanced to -85.9bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) advanced to – 139.bps. In addition, investors are looking forward to US CPI (YoY) on Tuesday which is expected to decrease to 4.1% from 4.9%.

Volatile week for USD

The US Dollar at the start of the week was lower due to economic data from the US weighing on the US dollar. In the middle of the week the US Dollar rose as the US Treasury yields surged. On Friday, the US dollar finished higher as investors awaited inflation data and the Federal Reserve’s interest rate decision next week. The EURUSD declined to 1.0749, while the GBPUSD increased to 1.2576. Additionally, the USDJPY increased to 139.40 Yen on Friday.

Oil and Gold traded higher towards the end of the week

Gold started the week higher due to the release of disappointing ISM Services PMI data for May. However, Gold traded lower at the end of the week after the expectations for the pause on rate hikes by the Federal Reserve acted as a tailwind for Gold, while rising US bond yields limit its upside potential. Prices of Oil moved higher at the start of the week after the world’s top exporter Saudi Arabia pledged to cut production by a further 1 million barrels per day (bpd) from July. However, at the end of the week oil moved higher, after the White House denied a report claiming that a nuclear deal between the U.S. and Iran was in the offering. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show an increase of 1.933M.

Stock indices performance

Key weekly events:

Tuesday – 13 June 2023

Wednesday – 14 May 2023

Thursday – 15 June 2023

Friday – 16 June 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/

https://www.investing.com/

https://www.fxstreet.com/

https://www.cnbc.com/world/

June 9th, 2023 by Nikolay Alexandrov

Global markets finished the week higher

The global markets started the week positively, but the enthusiasm faded throughout the day, finishing mostly in red, after the news of a debt ceiling deal. Biden and McCarthy announced that they have agreed upon a deal to raise the debt ceiling, but the case is not fully closed as the deal will need to pass through Congress. On the same day, the United States Consumer Confidence Index came in at 102.3 in May, down by1.4 index points compared to revised figures from the previous month. Moreover, on Wednesday, annual inflation in Germany stood in at 6.1% in May lower than expected. Furthermore, the number of job openings in the United States stood at 10.1 million in April, 358K more than expected. The stock markets on that day closed lower as investors are concerned about the global economy. On Thursday, annual inflation in the euro area dropped to 6.1% in May from 7% in April lower than expected. Also, on the same day, the number of seasonally adjusted initial jobless claims in the United States rose by 2,000 to 232,000 in the week ending May 27, but lower than expected. Lastly, on Friday, the stock markets ended the week sharply higher after the progress on the U.S. debt-ceiling deal and the release of the jobs report. Specifically, the United States Senate followed the House of Representatives and voted in favor of the bill seeking to suspend the debt ceiling until January 1, 2025, preventing thus the country’s first-ever default. Also on the same day, nonfarm payroll employment in the United States surged by 339,000 in May, far surpassing expectations, thus showing the resilience of the US labor market. However, the global markets closed the week with gains. The Dow Jones closed with a gain at the closing bell on Friday of 2.12%. The S&P jumped by 1.45%. Furthermore, the DAX gained 1.32% and the CAC 40 rose by 1.95%.

Treasury yields advanced towards the end of the week

Yields started the week lower as investors monitored debt ceiling deal negotiations. However, yields closed the week higher on Friday after investors digested higher-than-expected payroll data. Jobs data from the Labor Department on Friday showed payrolls increased by 339,000 last month, far better than expected. Specifically, on Friday, the yield on the 2-year Treasury increased to 4.503%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.698%, falling by about 1 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.9690%. The spread between the US 2’s and 10’s advanced to -80.5bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) declined to – 132.6bps.

Volatile week for USD

The US Dollar at the start of the week was lower due to lower yields. In the middle of the week the US Dollar rose as the Inflation data from Germany and France showed a decline in annual rates. On Friday, the US dollar finished higher after May’s non-farm payrolls report showed that employment numbers surged. The report showed that payrolls in the public and private sector increased by 339,000 in May. The EURUSD declined to 1.07135, while the GBPUSD increased to 1.2526. Additionally, the USDJPY increased to 139.90 Yen on Friday.

Oil and Gold traded higher towards the end of the week

Gold started the week higher due to complete collapse in confidence that comes with a U.S. default which would trigger a de-risking moment. However, Gold traded lower at the end of the week after the latest jobs report from the United States, showed an increase in nonfarm employment of 339,000 while the unemployment rate increased by 0.3 percentage points to 3.7%. Prices of Oil moved lower at the start of the week as the crude demand outlook continued to be shaken by the precariousness surrounding the United States debt limit situation. However, at the end of the week oil moved higher, as the United States Senate passing the bill to suspend the debt ceiling, and prevent the nation from defaulting, sparked investor optimism. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show a decrease of 3.466M.

Stock indices performance

Key weekly events:

Monday – 05 June 2023

Tuesday – 06 June 2023

Wednesday – 07 May 2023

Thursday – 08 June 2023

Friday – 09 June 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/

https://www.investing.com/

https://www.fxstreet.com/

https://www.cnbc.com/world/

June 2nd, 2023 by Nikolay Alexandrov

Global markets finished the week higher

The global markets started the week mostly in red after investors looked toward a possible breakthrough in the Congressional negotiations to raise the debt ceiling to avoid a government default before next month. Moreover, on Wednesday, the United Kingdom Consumer Price Index (CPI) stood at 8.7% on a yearly basis in April higher than expected. The stock markets on that day closed lower as investors are concerned about the global economy. On Thursday, the German economy saw a decrease of 0.3% in the first quarter of 2023 versus the previous trimester. Also, on the same day, the gross domestic product (GDP) of the United States rose by 1.3% in the first trimester of 2023 on an annual level and the number of seasonally adjusted initial jobless claims in the United States increased by 4,000 to 229,000. Lastly, on Friday the Congressional negotiations to raise the United States debt ceiling before the June deadline, came to a halt after Republican negotiators blamed the White House for resisting spending cuts. However, the global markets closed the week with gains. The Dow Jones closed with gain at the closing bell on Friday by 1%. The S&P jumped by 1.31%. Furthermore, the DAX gained 1.20%, the CAC 40 rose by 1.24% and the FTSE 100 advanced by 0.74%. In addition, investors are looking forward to the Eurozone Consumer Price expecting to stand at 7.0%

Treasury yields advanced towards the end of the week

Yields started the week higher as investors monitored debt ceiling deal negotiations and assessed what could be next for Federal Reserve interest rate policy after mixed messages from officials. On Thursday yields rose after the path of the economy as debt ceiling negotiations continued and uncertainty about the interest rate outlook intensified. However, yields were mixed on Friday after investors awaited economic data that could affect Federal Reserve interest rate policy and as debt ceiling deal talks continued. Specifically, on Friday, the yield on the 2-year Treasury increased to 4.568%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.810%, falling by about 1 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.9690%. The spread between the US 2’s and 10’s advanced to -75.8bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) advanced to – 139.5bps. investors are looking forward to the US Nonfarm Payrolls report on Friday, 2 of June, in which a decreased of 73K is expected.

Volatile week for USD

The US Dollar at the start of the week was flat due to talks between U.S. lawmakers over raising the debt ceiling. In the middle of the week the US Dollar rose as the ongoing risk aversion sentiment continues to support the US Dollar. On Friday, the US dollar finished lower but finished third straight weekly gain as markets raised bets on higher-for-longer interest rates and amid closely watched last-ditch talks on the U.S. debt ceiling. The EURUSD gained to 1.0731, while the GBPUSD increased to 1.2352. Additionally, the USDJPY decreased to 140.60 Yen on Friday.

Oil and Gold traded higher towards the end of the week

Gold started the week almost flat due to sharp losses from Friday’s stronger than expected nonfarm payrolls data. Gold traded lower in the middle of the week after investors waited for the summary of the new statements of the Federal Reserve’s latest meeting. However, Gold traded higher at the end of the week as ongoing negotiations on raising the United States debt ceiling without an apparent conclusion in sight seemingly made them a safety net for investors. Prices of Oil moved lower at the start of the week, after the uncertainty looming over the debt ceiling negotiations in the United States. However, at the end of the week oil moved higher, as concern about the commodity’s supply persisted ahead of the next OPEC+ meeting. Meanwhile, the Crude Oil Inventories report will be released on Thursday which is expected to show an increase of 11.355M.

Stock indices performance

Key weekly events:

Tuesday – 30 May 2023

Wednesday – 31 May 2023

Thursday – 01 June 2023

Friday – 02 June 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/

https://www.investing.com/

https://www.fxstreet.com/

https://www.cnbc.com/

May 17th, 2023 by Nikolay Alexandrov

Global markets finished the week mixed

The global markets started the week mixed after the jobs-report rally on Friday. Without any major economic data in the calendar on Monday and Tuesday, the clear headliner of this week was Wednesday’s release of the US CPI reading. Specifically, the annual inflation in the United States clocked in at 4.9% in April, edging down slightly from March’s figure of 5%. Moreover, on Wednesday, Germany’s Consumer Price Index (CPI) stood at 7.2% on a yearly basis in April as expected. The stock markets on that day closed mixed as the inflation is still elevated, above the 2% target level. Also, the president of the European Central Bank Christine Lagarde and Bundesbank’s head Joachim Nagel both confirmed that the Eurozone’s main financial institution will introduce more raises of interest rate in the future to combat inflation. On Thursday, the Bank of England’s (BoE) Monetary Policy Committee (MPC) announced an increase in key interest rates by a quarter percentage point to 4.50%, the highest level in 15 years. Also, on the same day, the US PPI index came out better-than-expected, showing a 0.2% monthly gain. Lastly, on Friday the United Kingdom’s gross domestic product (GDP) rose by 0.1% in the first quarter of 2023, however, the global markets closed the week mixed, after fears of dept limit crisis in the US. The Dow Jones closed flat at the closing bell on Friday. The S&P decreased by 0.16%. Furthermore, the DAX gained 0.50%, CAC 40 rose by 0.45% and the FTSE 100 advanced by 0.31%. In addition, investors are looking forward to the Eurozone Consumer Price expecting an increase to 7.0% from 6.9%

Treasury yields advanced towards the end of the week

Yields started the week higher as investors braced for key inflation data slated for release this week. Yields in the middle of the week fell after the latest CPI report showed inflation rose in April. Month on month, the Consumer Price Index (CPI) was up by 0.4%. However, yields increased on Friday after investors digested this week’s inflation data and assessed what it could mean for the future of the economy and Federal Reserve monetary policy. Specifically, on Friday, the yield on the 2-year Treasury increased to 3.994%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.459%, up by about 6.4 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.7770%. The spread between the US 2’s and 10’s advanced to -53.5bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) advanced to – 121.5bps.

Volatile week for USD

The US Dollar at the start of the week was higher following higher US Yields. In the middle of the week after Consumer Price Index (CPI) ticked lower in April to 4.9% from 5% in March, the US dollar dropped. On Friday, the US dollar finished strong following a US Yields increase despite evidence of slowing inflation and easing labor market conditions in the US. The EURUSD dropped below 1.0850, while the GBPUSD decreased to 1.2450. Additionally, the USDJPY raised to 135.70 yen on Friday.

Oil and Gold traded opposite towards the end of the week

Gold started the week flat due to sharp losses from Friday’s stronger than expected nonfarm payrolls data. Gold traded higher in the middle of the week after the United States Labor Statistics Bureau revealed that the inflation in the country slowed to 4.9% year over year, with the core inflation also cooling slightly. However, Gold traded lower at the end of the week following a stronger dollar. Prices of Oil moved higher at the start of the week, after recession fears continue to recede. However, at the end of the week oil continued to moved higher, after concerns over slowing U.S. economic growth. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show a decrease of 4.251M.

Stock indices performance

Key weekly events:

Tuesday – 16 May 2023

Wednesday – 17 May 2023

Thursday – 18 May 2023

Friday – 19 May 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/

https://www.investing.com/

https://www.fxstreet.com/

https://www.cnbc.com/world/