Market Outlook Week 29-02 June

Posted on June 9, 2023 by Nikolay Alexandrov

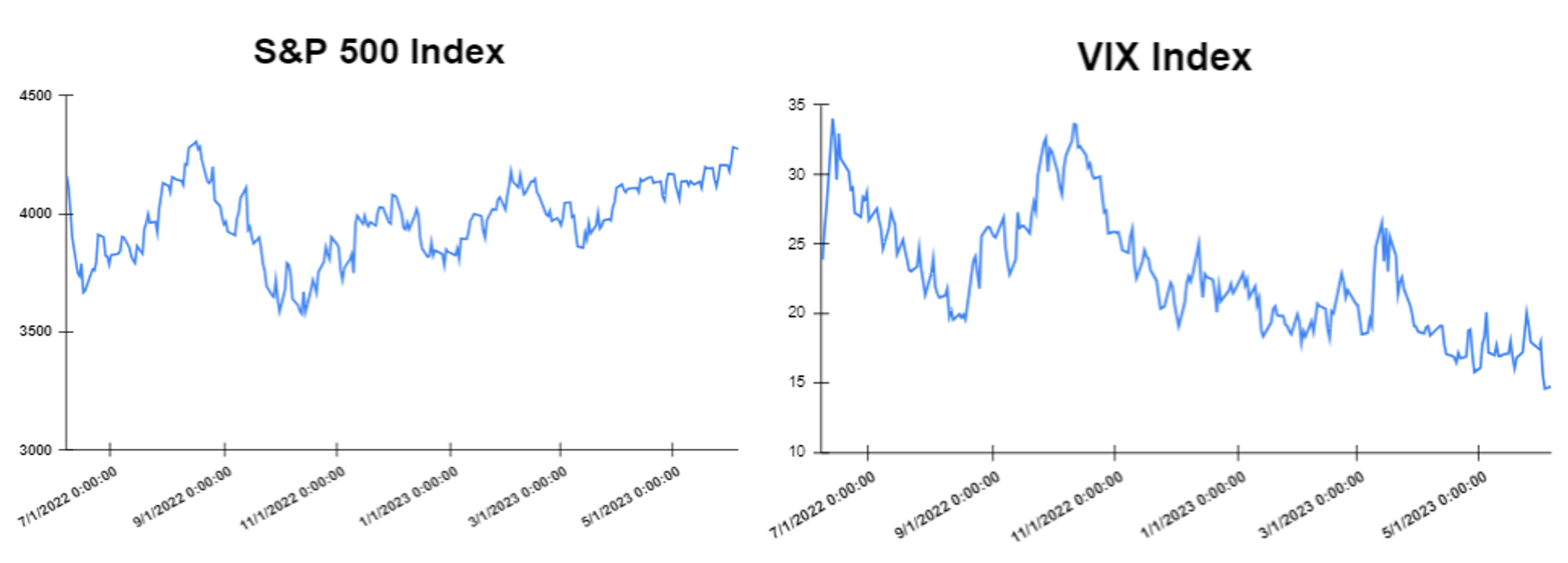

Global markets finished the week higher

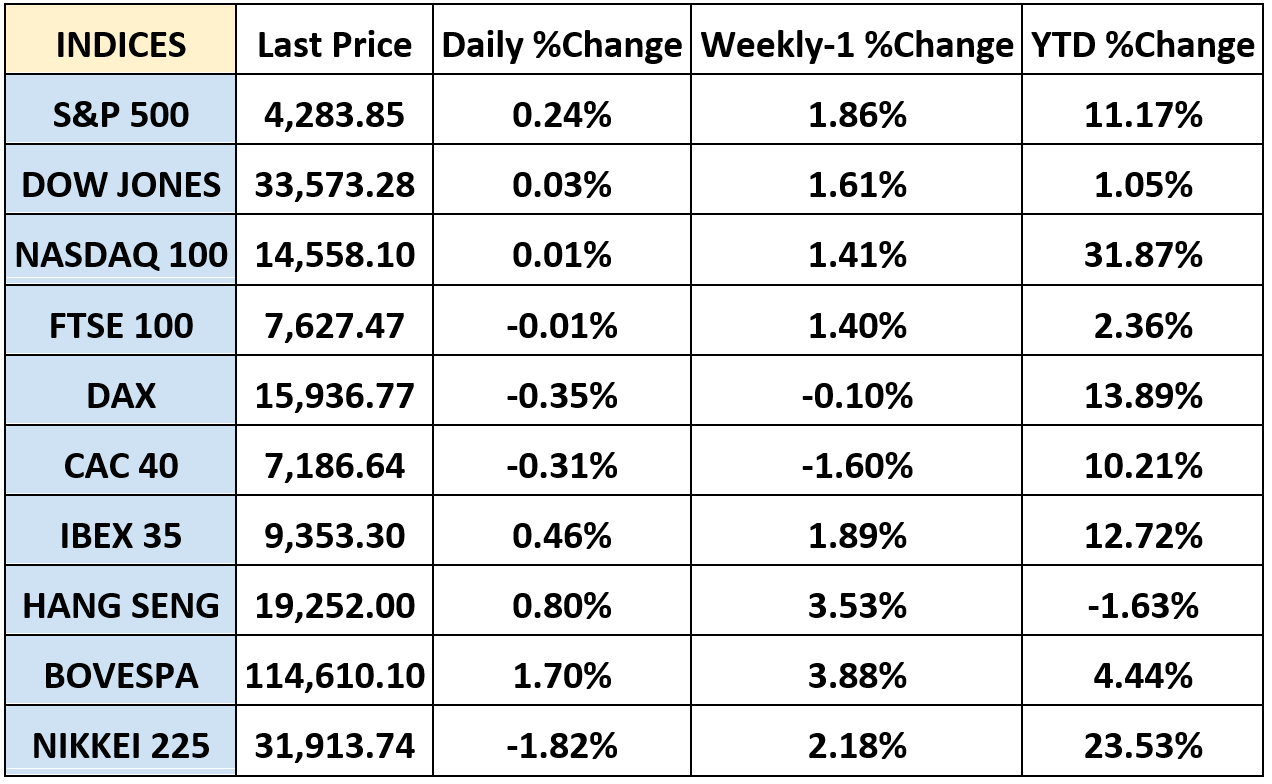

The global markets started the week positively, but the enthusiasm faded throughout the day, finishing mostly in red, after the news of a debt ceiling deal. Biden and McCarthy announced that they have agreed upon a deal to raise the debt ceiling, but the case is not fully closed as the deal will need to pass through Congress. On the same day, the United States Consumer Confidence Index came in at 102.3 in May, down by1.4 index points compared to revised figures from the previous month. Moreover, on Wednesday, annual inflation in Germany stood in at 6.1% in May lower than expected. Furthermore, the number of job openings in the United States stood at 10.1 million in April, 358K more than expected. The stock markets on that day closed lower as investors are concerned about the global economy. On Thursday, annual inflation in the euro area dropped to 6.1% in May from 7% in April lower than expected. Also, on the same day, the number of seasonally adjusted initial jobless claims in the United States rose by 2,000 to 232,000 in the week ending May 27, but lower than expected. Lastly, on Friday, the stock markets ended the week sharply higher after the progress on the U.S. debt-ceiling deal and the release of the jobs report. Specifically, the United States Senate followed the House of Representatives and voted in favor of the bill seeking to suspend the debt ceiling until January 1, 2025, preventing thus the country’s first-ever default. Also on the same day, nonfarm payroll employment in the United States surged by 339,000 in May, far surpassing expectations, thus showing the resilience of the US labor market. However, the global markets closed the week with gains. The Dow Jones closed with a gain at the closing bell on Friday of 2.12%. The S&P jumped by 1.45%. Furthermore, the DAX gained 1.32% and the CAC 40 rose by 1.95%.

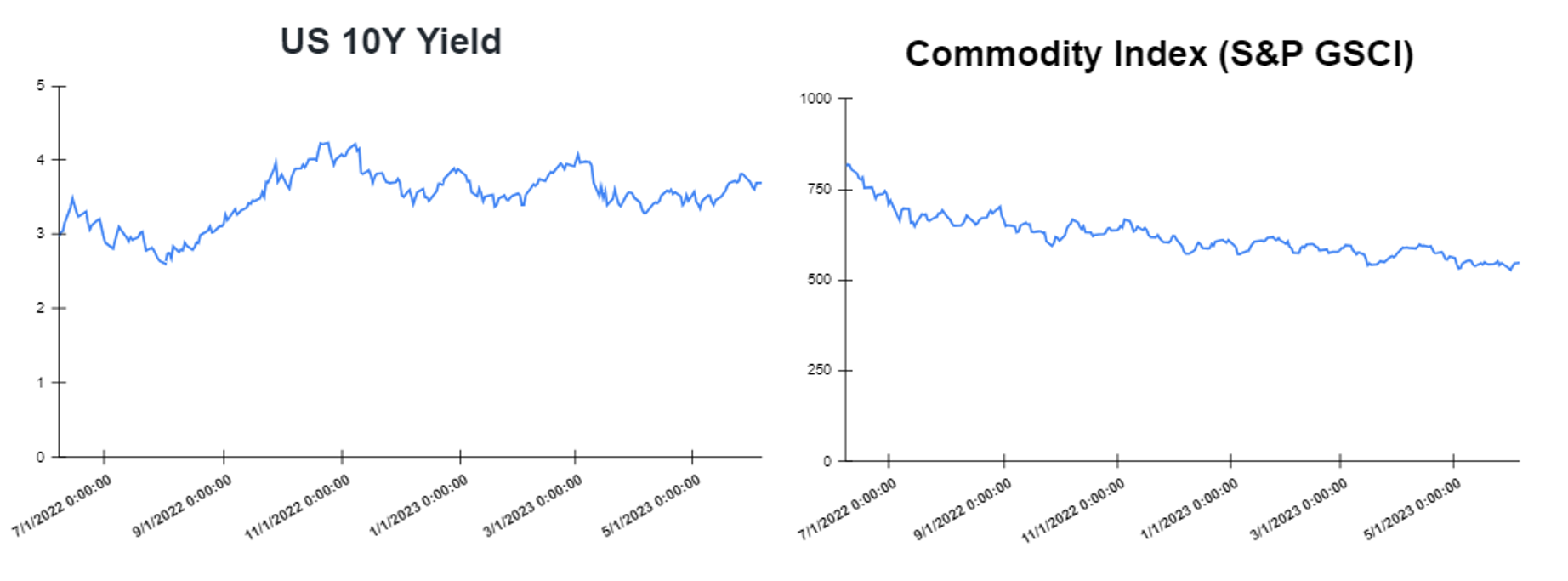

Treasury yields advanced towards the end of the week

Yields started the week lower as investors monitored debt ceiling deal negotiations. However, yields closed the week higher on Friday after investors digested higher-than-expected payroll data. Jobs data from the Labor Department on Friday showed payrolls increased by 339,000 last month, far better than expected. Specifically, on Friday, the yield on the 2-year Treasury increased to 4.503%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.698%, falling by about 1 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.9690%. The spread between the US 2’s and 10’s advanced to -80.5bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) declined to – 132.6bps.

Volatile week for USD

The US Dollar at the start of the week was lower due to lower yields. In the middle of the week the US Dollar rose as the Inflation data from Germany and France showed a decline in annual rates. On Friday, the US dollar finished higher after May’s non-farm payrolls report showed that employment numbers surged. The report showed that payrolls in the public and private sector increased by 339,000 in May. The EURUSD declined to 1.07135, while the GBPUSD increased to 1.2526. Additionally, the USDJPY increased to 139.90 Yen on Friday.

Oil and Gold traded higher towards the end of the week

Gold started the week higher due to complete collapse in confidence that comes with a U.S. default which would trigger a de-risking moment. However, Gold traded lower at the end of the week after the latest jobs report from the United States, showed an increase in nonfarm employment of 339,000 while the unemployment rate increased by 0.3 percentage points to 3.7%. Prices of Oil moved lower at the start of the week as the crude demand outlook continued to be shaken by the precariousness surrounding the United States debt limit situation. However, at the end of the week oil moved higher, as the United States Senate passing the bill to suspend the debt ceiling, and prevent the nation from defaulting, sparked investor optimism. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show a decrease of 3.466M.

Stock indices performance

Key weekly events:

Monday – 05 June 2023

Tuesday – 06 June 2023

Wednesday – 07 May 2023

Thursday – 08 June 2023

Friday – 09 June 2023

Sources:

https://www.tradingview.com/