January 27th, 2023 by Nikolay Alexandrov

Global markets finished the week mixed

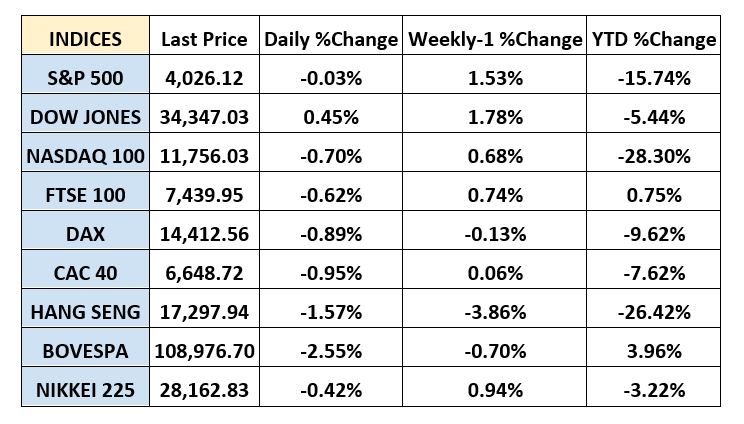

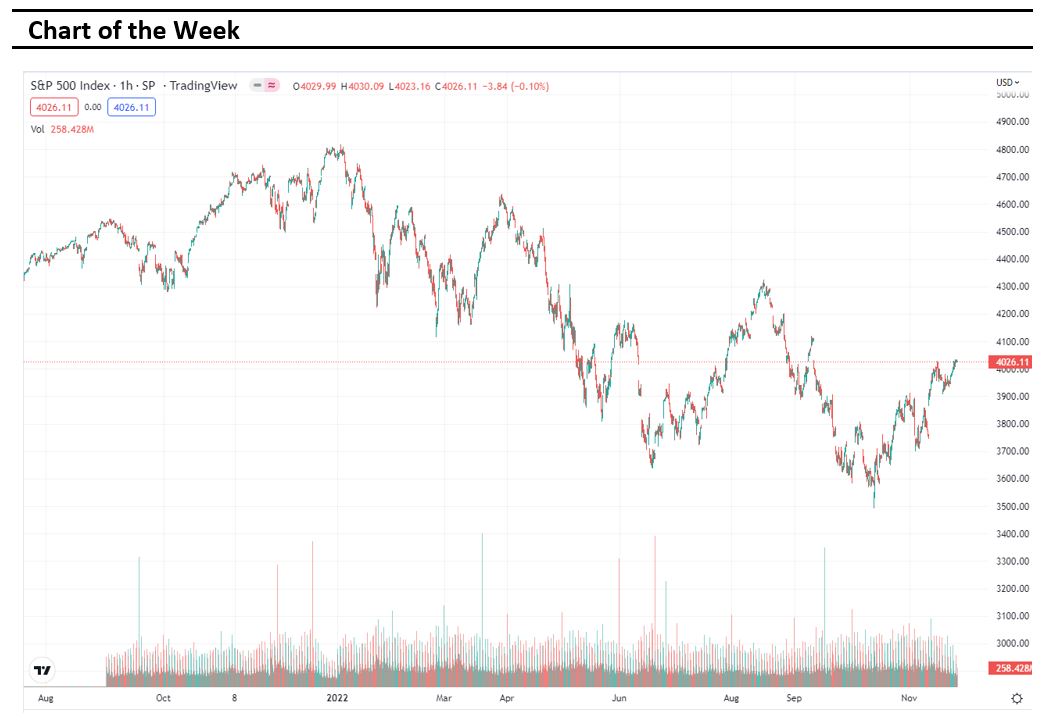

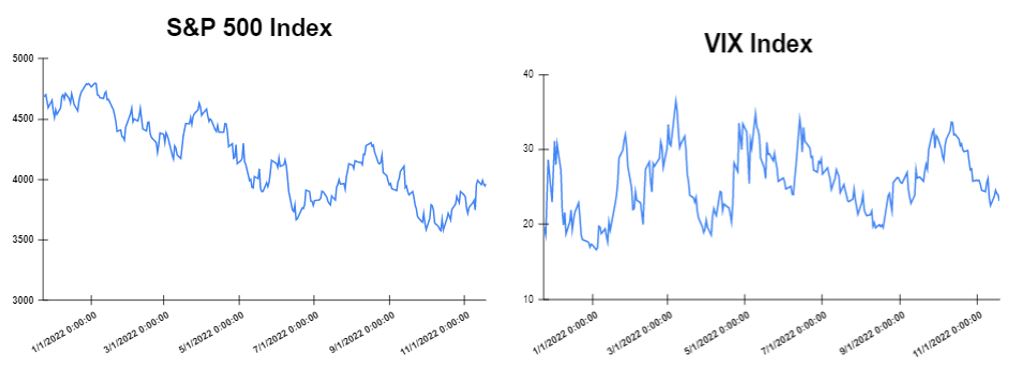

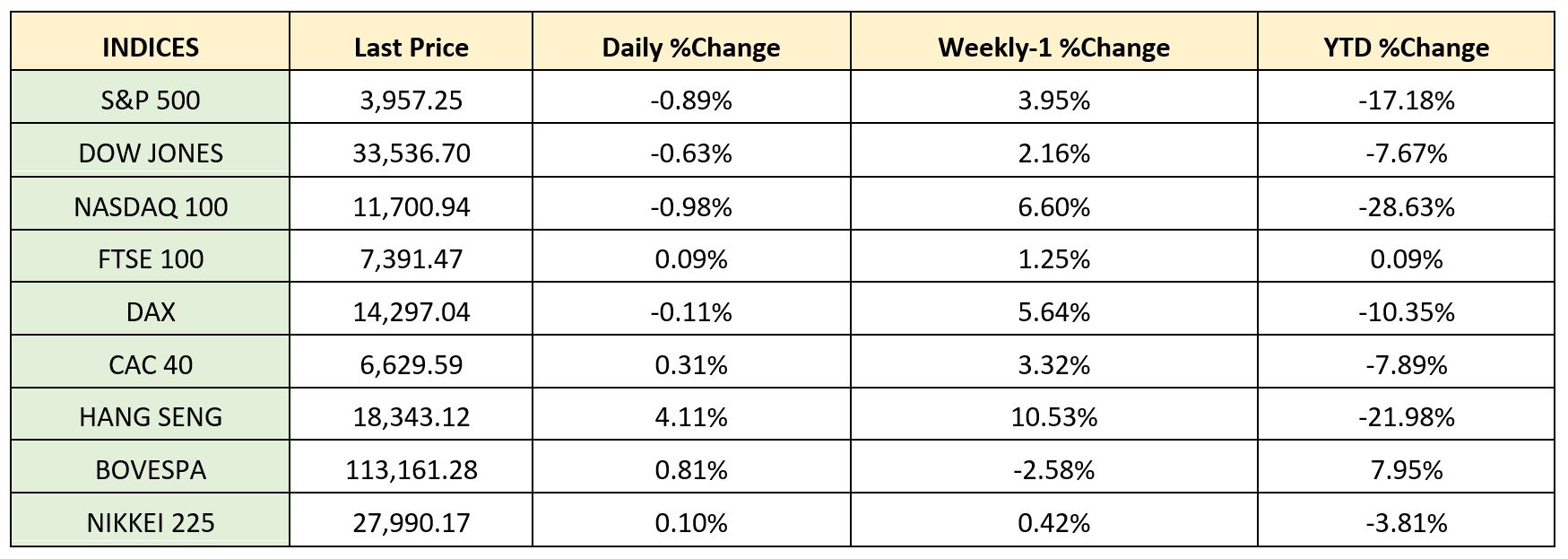

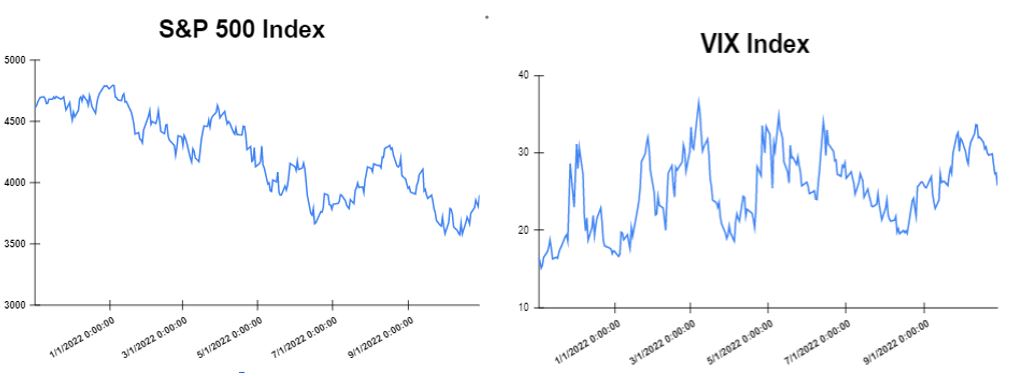

Global markets started the week lower as investors saw that the European Central Bank and US Federal Reserve are more likely to continue raising interest rates in order to reduce the inflation. In addition, global markets had gains in the middle of the week after the US federal Reserve hinted investors that the pace of rate hikes could slow down from December. Also, the Britain and Germany service manufacturing sectors updates offered some relief over economy entering recession. Furthermore, the Dow Jones gained 0.45% at the closing bell on Friday. The S&P 500 was flat. Moreover, the DAX also was closed flat. The CAC 40 went up by 0.08% and the FTSE 100 surged by 0.28%.

Treasury yields declined towards the end of the week

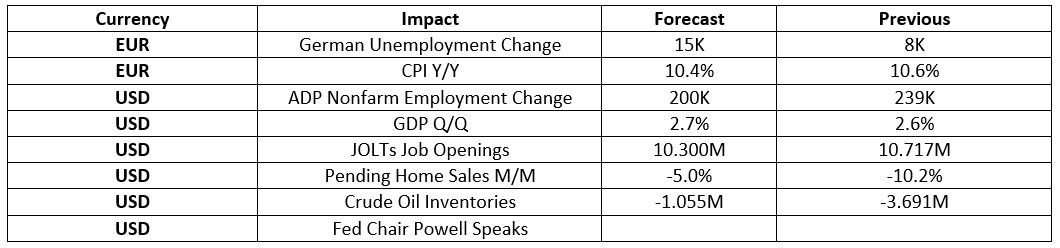

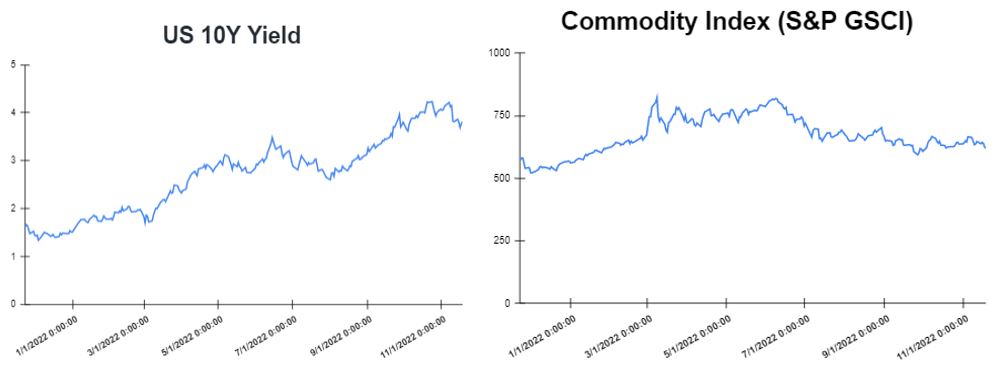

Yields declined after the Federal Reserve officials meeting suggested a slowdown in tightening ahead. A smaller interest rate increase is expected by the Federal Reserve in the next meetings. The yield on the 2-year Treasury dropped to 4.475%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.698% down, about 1 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.75%. The spread between the US 2’s and 10’s widened to -77.7bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) narrowed to – 168.9bps.

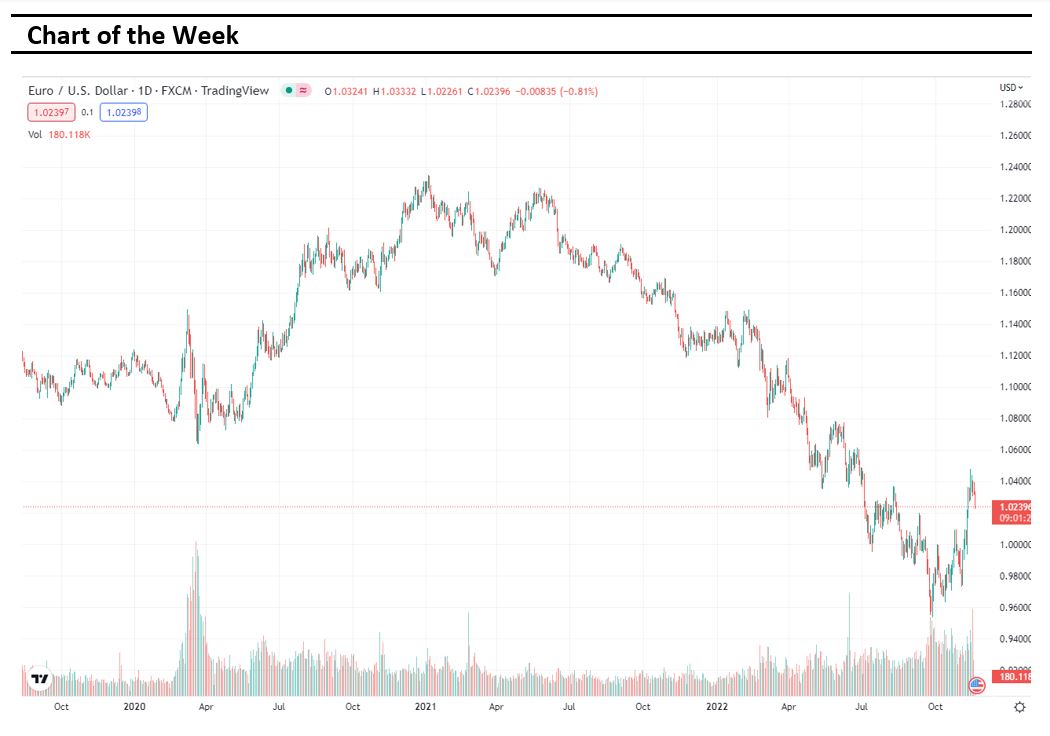

Volatile week for USD

The US Dollar moved lower this week after Consumer confidence across the United States worsened by just over 5% in November compared to the previous month. Moreover, in the United States, initial jobless claims increased by 17K to 240k, which was more than expected. This was not welcomed by the market as the EURUSD traded lower at 1.04015. Furthermore, the GBPUSD ended the week higher at 1.2084 and the USDJPY traded near 139.14 on Friday. Following a period of high volatility for US Dollar, the United States will release Nonfarm Payrolls on Friday 02nd of December, which is expected to confirm a drop on Nonfarm Payrolls to 200K.

Oil and Gold traded higher

Gold started the week with losses as investors are concerned following the new measures against Covid-19. However, Gold traded higher at the end of the week following the United States Federal Reserve policymakers meeting. Prices of Oil traded lower on Monday, as supply concerns stormed the global oil markets once again. However, oil dropped more in the middle of the week, as media reports that the price cap on Russian crude might be higher than the current price of it. The prices of oil futures increased on Friday as talks regarding the price cap on Russian Oil continued. Meanwhile, in the Crude Oil Inventories report on Wednesday, an increase is expected in the number of barrels held by US firms by 2.636M.

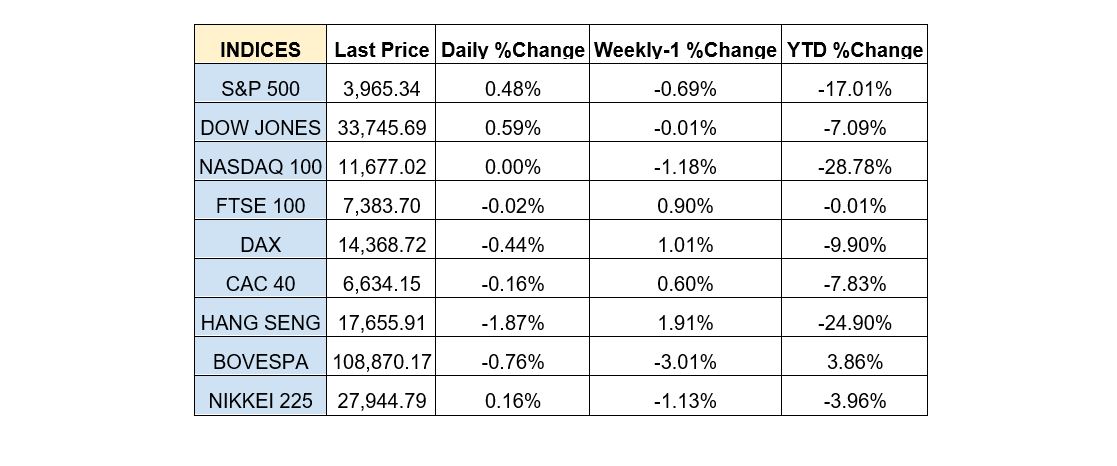

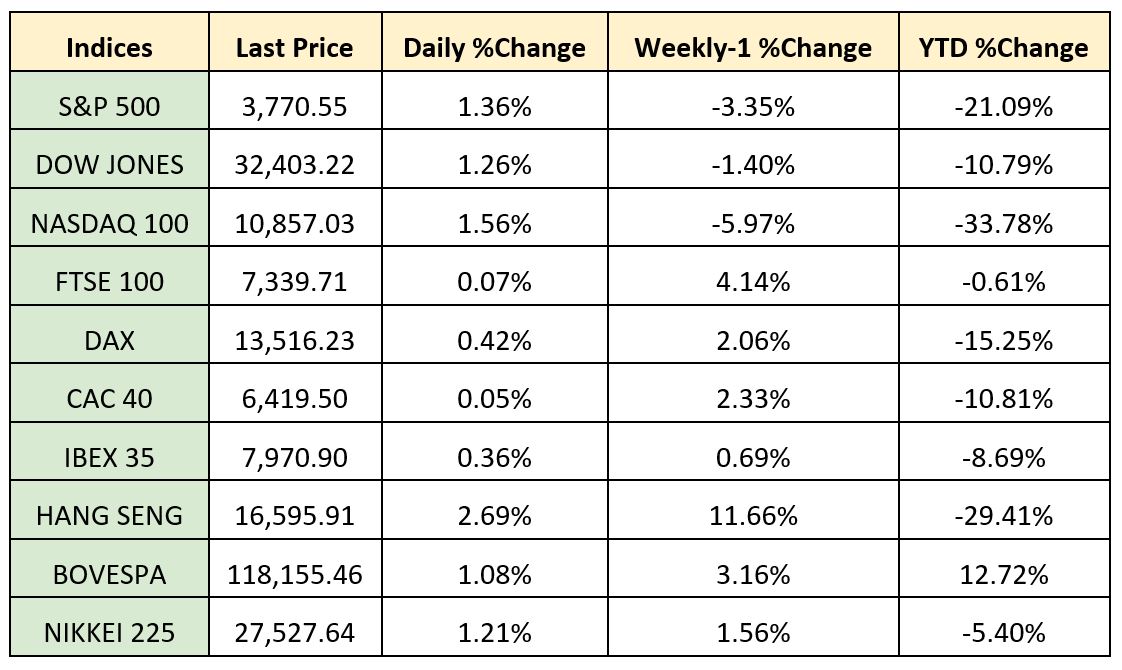

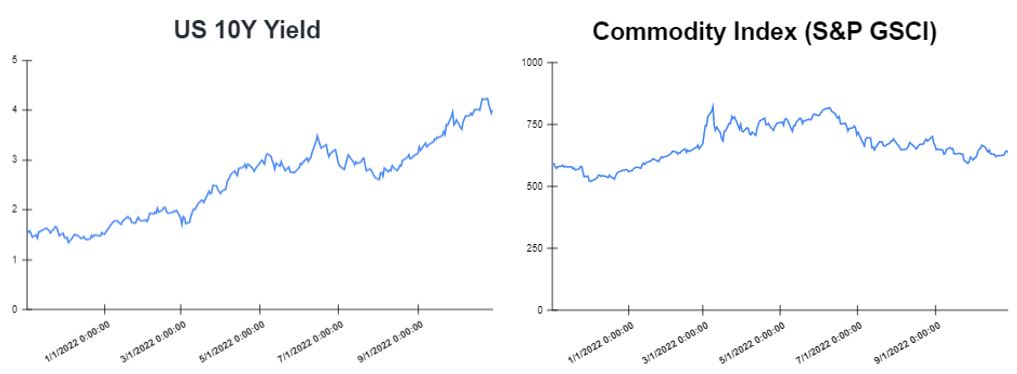

Stock indices performance

Key weekly events:

Monday – 28 November 2022

Tuesday – 29 November 2022

Wednesday – 30 November 2022

Thursday – 01 December 2022

Friday – 02 December 2022

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

January 27th, 2023 by Nikolay Alexandrov

Global markets finished the week lower

The news this week were generally good, but this was not reflected in global markets as it was a relatively flat week. The US producer price index (PPI) report was better-than-expected, showing that inflation pressures are moderating. Also, Wednesday’s retail sales came with stronger-than-expected data as they showed a 1.3% increase in spending. That means that the consumers remain resilient despite the fact that the policymakers continue to highlight that more rate hikes are needed to smooth inflation. In addition, investors were bracing themselves for the inflation to be published this week in Europe and UK. Markets were mostly lower after the October CPI in Europe came in lower than expected, still arriving at a record high of 10.6%. The UK inflation reached 11.1%, so it came out much higher than expected. Furthermore, the Dow Jones gained 0.159% at the closing bell on Friday. The S&P 500 rose by 0.48%. Moreover, the DAX gained 1.16%. The CAC 40 went up by 1.04% and the FTSE 100 surged by 0.53%.

Treasury yields advance towards the end of the week

Yields advanced after Federal Reserve officials suggested interest rates would go higher still, after recent economic data had given investors hope about inflation easing. A smaller than expected rise in consumer prices for the month of October and last week annual inflation has given investors hope that inflation could be coming down. The yield on the 2-year Treasury raised to 4.51%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.819% up, about 4 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.932%. The spread between the US 2’s and 10’s widened to -69.1bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) widened to -181bps.

Volatile week for GBP

The British pound moved higher this week after the better than expected inflation report in UK. Moreover, in the United Kingdom retail sales increased by 0.6% in October, which was slightly more than 0.5% which was expected. This was welcomed by the market as the GBPUSD appreciated to 1.1894. Furthermore, the EUR/USD ended the week lower at 1.0329 and the USDJPY traded near 140.32 on Friday. Following a period of high volatility for US Dollar, the United States will release Initial Jobless Claims on Wednesday 23th of November, in which is expected to confirm a rise on initial jobless to 225K.

Oil and Gold traded opposite

Gold started the week with gains as investors are betting that the federal reserve would ease off on big interest rate hikes following inflation data. Gold traded lower in the middle of the week following United States economic data. However, Gold traded slightly higher at the end of the week as of Thursday as Federal Reserve officials boosted the dollar with the prospect of more interest rate hikes. Prices of Oil traded lower on Monday, as supply concerns stormed the global oil markets once again. However, oil dropped more in the middle of the week, as Iraq’s State Organization for Marketing of Oil said that the Iraqi Energy Ministry is aiming to increase crude oil output rates. The prices of oil futures remained lower on Friday by the uncertainties over demand in China.

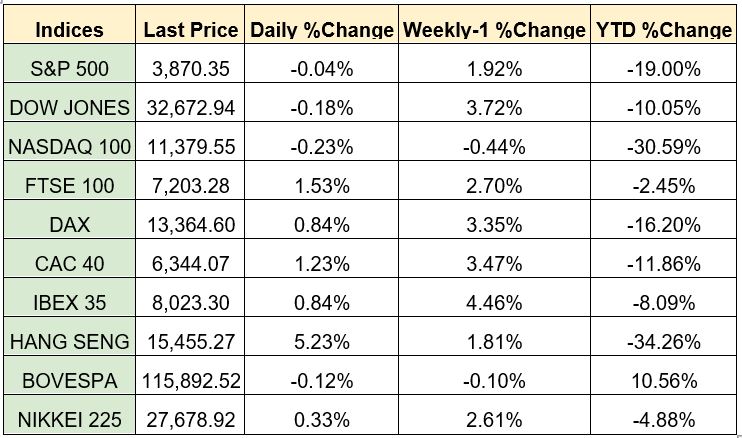

Stock indices performance

Key weekly events:

Tuesday – 22 November 2022

Wednesday– 23 November 2022

Thursday– 24 November 2022

Friday– 25 November 2022

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

January 27th, 2023 by Nikolay Alexandrov

Global markets finished the week higher

Global markets started the week mostly higher after the release of new economic data on housing, industrial production, and investor confidence in Europe. In addition, investors were bracing themselves for the forthcoming data on inflation to be published this week and ahead of the U.S. midterm elections. Historically, the stock market has tended to perform well following the mid-term election results, no matter which party wins. However, the most important driver of market outcomes this year remains the inflation. Markets were sharply up after the October CPI came in lower than expected. The headline inflation posted a 7.7% y/y increase, compared to the expected 7.9%. In response to this surprise, stocks surged, treasury yields sank and the dollar weekend. The Dow Jones gained 0.10% at the closing bell on Friday. The S&P 500 rose by 0.92%. Moreover, the DAX gained 0.56%. The CAC 40 went up by 0.58% and the FTSE 100 tumbled by 0.78%.

Treasury yields declined towards the end of the week

Yields tumbled after Labor Statistics Bureau confirmed the October CPI at a lower-than-expected 7.7%, with the figure dropping for the fourth consecutive month pulled by the Federal Reserve’s strong rate hikes. For investors this was a signal that price increases have possibly peaked and that a slowdown to 0.5% rate hike in December seems to be the most probable move for FED. The yield on the 2-year Treasury dropped to 4.397%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.946% down, about 19.6 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 4.196%. The spread between the US 2’s and 10’s narrowed to -45.1bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) tightened to -173.4bps.

Volatile week for USD

Traders were on risk-on mood after the softer than expected inflation report. The Dollar fell across the board for a second straight day on Friday. Therefore, EUR/USD ended the week higher at 1.036. Moreover, in the United Kingdom the gross domestic product (GDP) decreased by 0.2% in the third quarter, which was significantly above the -0.5% consensus. This was welcomed by the market as the GBPUSD appreciated to 1.1853. The services sector slowed to flat output, while production slid by 1.5% in the three-month period with manufacturing dropping by 2.3%. The USDJPY went on a free fall this week and traded near 138.55 on Friday. Following a period of high volatility for the British pound, the United Kingdom will release CPI Y/Y on Wednesday 16th of November, in which is expected to confirm a rise on inflation by 0.6% to total 10.7%.

Oil and Gold traded higher

Gold started the week with losses as China’s recommitment to its zero-COVID policy ramped up concerns over slowing economic growth and boosted the dollar. Gold traded higher in the middle of the week after United States report on the annual inflation. However, Gold traded higher at the end of the week as of Thursday as U.S. inflation registered its slowest annual reading in nine months, heightening speculation that the Federal Reserve will back off from the aggressive rate hikes it has executed since March, sending the dollar crashing. Prices of Oil traded higher on Monday, as supply concerns stormed the global oil markets once again. However, oil gained more in the middle of the week, as investors digested the cooler-than-expected inflation reading in the United States. The prices of oil futures remained higher on Friday but fell week by week after health authorities in China eased some of the country’s heavy COVID-19 curbs. Meanwhile, in the Crude Oil Inventories report on Wednesday, decrease is expected in the number of barrels held by US firms by 2.565M.

Stock indices performance

Key weekly events:

Monday – 14 November 2022

Tuesday – 15 November 2022

Wednesday – 16 November 2022

Thursday – 17 November 2022

Friday – 18 November 2022

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

*Disclaimer: The information contained in this publication does not constitute investment advice and is not a personal recommendation from NaxexInvest. Nothing contained herein constitutes the solicitation of the purchase or sale of type of financial instrument. Any investment activities undertaken using this information will be at the sole risk of the relevant investor. NaxexInvest expressly disclaims all liability for the use or interpretation (whether by visitor or by others) of information contained herein. Decisions based on this information are the sole responsibility of the relevant investor. Any visitor to this page agrees to hold NaxexInvest and its affiliates and licensors harmless against any claims for damages arising from any decisions that the visitor makes based on such information.

January 27th, 2023 by Nikolay Alexandrov

Global markets finished the week higher

Global markets started the week mix after Eurostat put the Eurozone inflation estimate at another all-time high in October. In addition, investors were bracing themselves for another Federal Reserve meeting. Later in the week Federal Reserve’s and Bank of England raised interest rates by additional 75 basis points, which initially moved the market mostly lower. However, the Equity markets closed higher in Europe as investors digested the latest batch of economic data, alongside the central banks’ monetary policy decisions. Therefore, Markets on Wall Streat closed Friday in the green following data on the country’s employment, as well as the Federal Reserve’s remarks. The Dow Jones gained 401 points or 1.26% at the closing bell on Friday. The S&P 500 rose 1.36%. Moreover, the DAX gained 2.51%. The CAC 40 went up 2.77% and the FTSE 100 soared by 2.03%.

Treasury yields advance towards the end of the week

Yields climbed after October’s jobs report painted a mixed picture of the labor market. U.S. nonfarm payrolls surged by 261,000, according to data from the Bureau of Labor Statistics. That was much higher than the 205,000 add that economists expected. At the same time, the unemployment rate ticked up slightly to 3.7% from 3.5% a month earlier. The yield on the 2-year Treasury moved up to 4.663%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, which hit 4.171% up about 5 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 4.18%. The spread between the US 2’s and 10’s widened to -71.2bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) narrowed to -186.2bps. Meanwhile, investors are looking to October’s consumer inflation figures, due to be released on Thursday, in which a pullback is expected in the y/y headline rise to 8.0% from 8.2% in September.

Volatile week for USD and GBP

EUR/USD ended the week at 0.9960, after the common currency has erased the previous four days’ losses. However, the greenback was under pressure this week ahead of interest rate decision. The Federal Reserve and Bank of England raised rates by 75 bps. In addition, after the U.S. nonfarm payrolls report for October showed the world’s largest economy created more new jobs than expected, but also flashed signs of a slowdown with a higher unemployment rate and lower wage inflation. The EUR/USD pair was higher at the end of the week at 0.9960, while USD/JPY is at 146.65 and GBP/USD is at 1.14. Following a period of high volatility for the British pound, the United Kingdom will release third quarter GDP figures on Friday 11th of November, in which is expected to confirm a contraction rate of -0.2% q/q.

Oil and Gold traded higher

Gold started the week with losses as the Federal Reserve (Fed) is set to tighten its policy further to combat rigid inflation. Gold traded lower in the middle of the week after Chairman Jerome Powell dashed hopes that interest rate hikes will end soon. However, Gold traded higher at the end of the week the release of the latest economic data in the United States. The country’s Bureau of Labor Statistics stated earlier that total nonfarm payroll employment went up by 261,000 last month. Prices of Oil traded lower on Monday, after the latest reports on China’s manufacturing activity, which showed that the sector tumbled into the contraction territory in October, seemingly raised concerns on the demand side. However, oil gained in the middle of the week. The data could suggest that demand is holding up despite the continued interest rate hikes in major world. The prices of oil futures surged on Friday as supply concerns pushed up the prices of the commodity. Meanwhile, in the Crude Oil Inventories report on Wednesday, it is expected an increase in the number of barrels held by US firms by 0.367M.

Stock indices performance

Key weekly events:

Monday – 07 November 2022

Tuesday – 08 November 2022

Wednesday – 09 November 2022

Thursday – 10 November 2022

Friday – 11 November 2022

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

January 27th, 2023 by Nikolay Alexandrov

Global markets finished the week higher

Global markets started the week with gains after the announcement of Rishi Sunak as the new UK Prime Minister. In addition, investors were bracing themselves for a series of earnings reports a number of important companies will release throughout the week. Later in the week European Central Bank’s raised interest rates by additional 75 basis points making the third straight increase, which initially moved the market mix. However, the Equity markets closed higher in Europe following newest reports on inflation in countries such as Germany and France showed figures somewhat below or matching expectations. Therefore, Markets on Wall Streat closed Friday in the green following Data reports, alongside earnings. The Dow Jones gained 828 points or 2.59% at the closing bell on Friday. The S&P 500 rose 2.46%. Moreover, the DAX gained 0.21%. The CAC 40 went up 0.45% and the FTSE 100 declined by 0.45%.

Treasury yields advance towards the end of the week

Yields climbed after an employment cost index for September pretty much matched forecasts, signalling nothing to derail the central bank from imposing another three quarters percentage point rate hike on the economy at a policy meeting next week. The yield on the 2-year Treasury moved up by 10 basis points to 4.424%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, which hit 4.006% up about 7 basis points, one day after the yield fell as much as 11 basis points on Thursday. The 30-year Treasury yield, which is key for mortgage rates, hit 4.144%. The spread between the US 2’s and 10’s widened to -44.9bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) widened as well to -192.3bps.

Volatile week for EUR

EUR/USD ended the week at of 0.9966, the European Central Bank hiked the main rates, for the third consecutive time, by 75 bps. However, the message on growth and economic developments was most discouraging. In addition, the greenback was under pressure this week ahead of the Federal Reserve’s Nov. 1-2 policy setting meeting. The Federal Reserve is expected to raise rates by 75 bps, while the Bank of Japan bucked the trend among other major central banks and stuck with ultra-low interest rates. The EUR/USD pair was flat at the end of the week at 0.9966, while USD/JPY is at 147.48 and GBP/USD is at 1.1614.

Oil and Gold in opposite trades

Gold started the week with gains as investors are highly optimistic after third consecutive bullish settlement of the S&P500. Gold traded more higher in the middle of the week after a series of companies posted growth in the third quarter. However, Gold dropped at the end of the week after the United States Bureau of Economic Analysis reported that the Personal consumption expenditures (PCE) price index, excluding food and energy, jumped 5.1%. Prices of Oil traded lower on Monday, as data showing demand from China remained lackluster in September and a strong U.S. dollar weighed, while weakening U.S. business activity data eased expectations for more aggressive interest rate hikes and limited price decline. However, oil gained in the middle of the week as supply fears still seemingly persisted. The prices of oil futures tumbled on Friday, Prices of crude oil futures tumbled on Friday as demand concerns seemingly stirred the stability in global markets

Stock indices performance

Key weekly events:

Monday – 31 October 2022

Tuesday – 01 November 2022

Wednesday – 02 November 2022

Thursday – 03 November 2022

Friday – 04 November 2022

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

January 27th, 2023 by Nikolay Alexandrov

Global markets finished the week in Europe mix and US higher

Global markets started the week with gains after Investors look forward to the release of the inflation report in the Euro Zone. In addition, investors are optimistic about the result of economic and earnings reports. Later in the week inflation in the United Kingdom went up by 10.1% on an annual level in September, matching the record set in July and coming in slightly higher than analysts projected, which initially moved the market lower. However, the Equity markets closed mix in Europe following the resignation of Prime Minister Liz Truss. Therefore, Markets on Wall Streat closed Friday in the green after an earlier report from the Wall Street Journal stated that some Fed officials are concerned about overtightening with considerable rate hikes. The Dow Jones gained 748 points or 2.47% at the closing bell on Friday. The S&P 500 rose 2.37%. Moreover, the DAX declined 0.29%. The CAC 40 slid 0.85% and the FTSE 100 rose 0.37%.

Treasury yields falls after a potential slowdown in Fed hikes

Yields declined after a report that some Federal Reserve officials are concerned about overtightening with rate hikes. Market expectations for a 0.75 percentage point hike in December dipped after the report, though a hike of that size in November is widely viewed as locked in. The yield on the 2-year Treasury fell more than 12 basis points to 4.481%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, which hit 4.337% at one point during the session, fell less than one basis point to 4.219%. The 30-year Treasury yield, which is key for mortgage rates, jumped 12 basis points to 4.335%. The spread between the US 2’s and 10’s tightened to -29.6bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) widened to -181.9bps.

Volatile week for GBP

GBP/USD ended the week at of 1.1250, Prime Minister Liz Truss resigned after 44 days in office, after failing to order the financial system. In addition, Consumer prices in the United Kingdom went up by 10.1% on an annual level in September. Also, despite of possible recession a report from the Wall Street Journal stated that some Fed officials are concerned about overtightening with considerable rate hikes. The EUR/USD pair jumped at the end of the week at 0.9863, while USD/JPY is at 150.41.

Oil and Gold traded higher

Gold started the week with gains as investors react to uncertainties related to inflation and the energy crisis. Gold traded lower in the middle of the week after as the yields rose but gold managed to increased a little bit at the end of the week by 0.76%. Prices of Oil held steady Monday, after investors worried that economic storm clouds could foreshadow a global recession. The prices of oil futures gains on Friday, as traders weighed up slowing economic growth on the back of higher interest rates as well as cuts to supply from a group of top producers.

Stock indices performance

Key weekly events: Monday – 24 October 2022

Tuesday – 25 October 2022

Wednesday – 26 October 2022

Thursday – 27 October 2022

Friday – 28 October 2022

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/2022/10/21/10-year-treasury-climbs-to-fresh-14-year-high.html

June 10th, 2022 by Nikolay Alexandrov

The global economy has suffered two unprecedented shocks in a short amount of time. First came the Covid pandemic in 2020 and this was followed by the war in Ukraine in February 2022. Both already have a serious effect on markets and especially on economic policy. These shocks have created new geopolitical priorities by exposing major vulnerabilities in what proves to be an excessively interdependent globalized economy. Which equity sectors are performing better, and which are faltering in this environment?

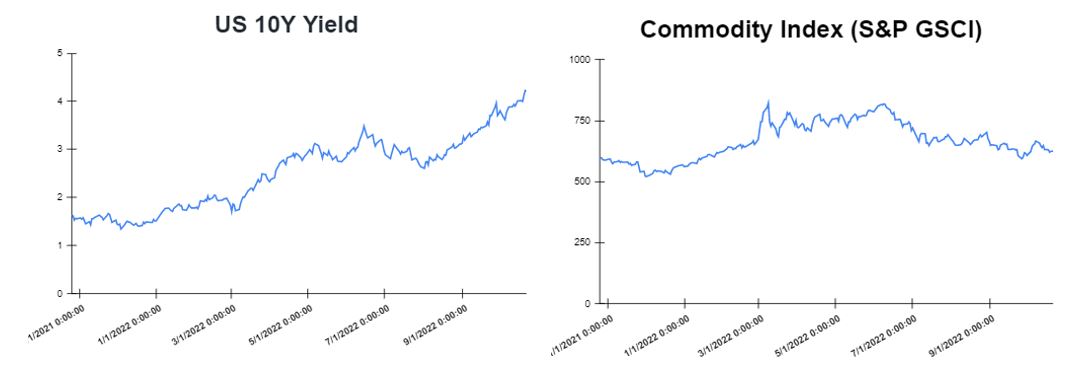

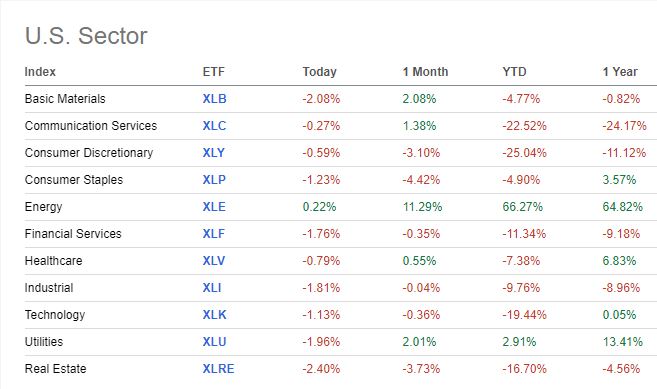

Year to date, the S&P 500 energy sector has been the strongest of the benchmark’s eleven sectors, rising 66.27% through June 8th, while the broad S&P 500 was down 13.80%. During a year in which the price of West Texas Intermediate crude oil based on continuous forward-month contract quotes has increased close to 60% to $122.00 a barrel (June 8th figure) and gasoline prices have soared, investors already know that commodities are a bright spot in a down market for stocks and bonds.

The Utilities sector has tended to perform relatively better when concerns about slowing economic growth resurface, and to underperform when those worries fade. That is partly because of the sector’s traditional defensive nature and steady revenues because people need water, gas, and electric services during all phases of the business cycle. Recent signs of peaking economic growth provide a relative tailwind for this defensive sector, particularly as market volatility rises. However, expectations for higher short- and long-term interest rates somewhat counterbalance the defensive attributes.

Apart from the Utilities sector (XLU) that is 2.91% up on a YTD (year to date) basis, it is worth mentioning that defensive sectors or “non-cyclical”* sectors like Staples (XLP), Healthcare (XLV) and Finance (XLF) are in the red on a YTD basis, however though still overperforming the general S&P500 Index.

Consumer staples stocks crumbled recently due to a plunge in shares of Walmart, Costco, and others. The once-bulletproof sector started faltering after Walmart reported disappointing earnings. The megaretailer complained about the rising cost of labor, fuel and shipping, as well as a rapidly shifting demand environment in which consumers spent more on low-margin food and gas purchases and less on discretionary items. Competitor Target mentioned the same forces when discussing its underwhelming margins right after Walmart remarks. With only Energy and Utilities sectors in the green for 2022, Consumer Staples remain “in the doghouse” for now.

Unlike Consumer staples, consumer discretionary stocks such as Target, Amazon and Tesla, were already deep in the red for the year. The latest retail woes intensified those losses. To understand the situation, the XLY (The Consumer Discretionary Select Sector SPDR Fund) ETF was down by a whopping 30% YTD in May led by steep declines in Amazon and Tesla, the two of which make up a whopping 38% of the ETF. The sector has recovered slightly and was down 25.04% by June 8th.

As we roll into June, the major U.S. stock indexes have all flirted with or succumbed to bear markets. A bear market is considered to occur when an index or an asset’s price has declined more than 20% from a recent high.

The question now is whether the late May rally signals the worst of the selloff is over. Inflation could be plateauing, and the focus of market worries appears to be shifting to economic growth, particularly as the Federal Reserve is committed to keep raising interest rates.

*Non-cyclical sectors are sectors to which consumers will continue to consume their products even during an economic downturn.

Sources

home.saxo, seekingalpha.com, morningstar.com schwab.com, etf.com, forbes.com .

*Disclaimer: The information contained in this publication does not constitute investment advice and is not a personal recommendation from Fortissio. Nothing contained herein constitutes the solicitation of the purchase or sale of type of financial instrument. Any investment activities undertaken using this information will be at the sole risk of the relevant investor. Fortissio expressly disclaims all liability for the use or interpretation (whether by visitor or by others) of information contained herein. Decisions based on this information are the sole responsibility of the relevant investor. Any visitor to this page agrees to hold Fortissio and its affiliates and licensors harmless against any claims for damages arising from any decisions that the visitor makes based on such information.

June 2nd, 2022 by Nikolay Alexandrov

Why is gold generally considered a good inflationary hedge? Gold is a valuable resource with many benefits that make it an ideal investment. These benefits include its scarcity, durability, portability, divisibility, and liquidity.

Gold prices are not moving up as most investors would expect even amid globally rising inflation. Traditionally, gold was one of the best hedges against inflation. However, in the current global economic conditions, gold prices seem to be trending in a tight range even when inflation is on the rise at unprecedented pace. The last few days, the price of spot gold ranges roughly between a low of $1830 and a high of $1870 per troy ounce.

The aim of a hedge-asset is to protect finances from risky situations. The higher the risk of loss, the greater the importance of protection against it. However, rarely does a hedge investment completely eliminate the potential for losses.

Some very good reasons that can explain the current stagnancy of the gold include the stronger dollar and U.S. Treasury yields alongside a global inflation surge expectation that could lead to more aggressive monetary policy measures. According to a CNBC’s article rising real yields in the United States and continental Europe and a firm dollar are negative factors for gold at this particular moment. Higher U.S. interest rates increase the opportunity cost of holding gold. At the same time, the ECB is under pressure to end its ultra-looser monetary policy and is expected to raise interest rates.

There is a clear positioning from the US Fed that the rate hikes will continue until inflation is under control. The rising rates will make it more attractive for investors to stay in the currency and earn the higher currency yield. This has also led to a strengthening US currency. Hence, gold being quoted in US Dollars, the price is expected to come down.

Another view however is that gold is having a decent year, if only by not losing. Year-to-date returns show gold as one of the few asset classes in positive territory, even with a modest 2% return. Gold’s gains may be small, but they’re far better than double-digit losses in equities, credit, and U.S. Treasuries.

Blackrock analysts suggest that going forward, gold’s efficiency as a hedge will be guided by the market’s largest headwind. To the extent volatility remains mostly a function of central bank tightening, gold may continue to struggle as monetary conditions normalize. However, if attention re-focuses on the war in Europe and all the impossible to quantify outcomes, gold will probably hold up relatively well amidst the chaos.

t2conline.com, financialexpress.com, economictimes.indiatimes.com, cnbc.com, seekingalpha.com, blackrock.com .

*Disclaimer: The information contained in this publication does not constitute investment advice and is not a personal recommendation from Fortissio. Nothing contained herein constitutes the solicitation of the purchase or sale of type of financial instrument. Any investment activities undertaken using this information will be at the sole risk of the relevant investor. Fortissio expressly disclaims all liability for the use or interpretation (whether by visitor or by others) of information contained herein. Decisions based on this information are the sole responsibility of the relevant investor. Any visitor to this page agrees to hold Fortissio and its affiliates and licensors harmless against any claims for damages arising from any decisions that the visitor makes based on such information.

May 26th, 2022 by Nikolay Alexandrov

Natural gas is the third most important source of energy behind oil and coal. The use of natural gas is growing quickly and is expected to overtake coal in the second spot by 2030. Natural gas was first developed commercially in the United States in 1825 but became a major source of energy globally in the 1970s. Today, natural gas is used by power plants to generate electricity, as well as for domestic heating and cooking.

The world’s biggest producers of natural gas are the United States, Russia, Iran, Qatar, Canada, China and Norway. These countries provide excess natural gas that can be exported to other countries, which is either transported through pipelines or as liquefied natural gas (LNG).

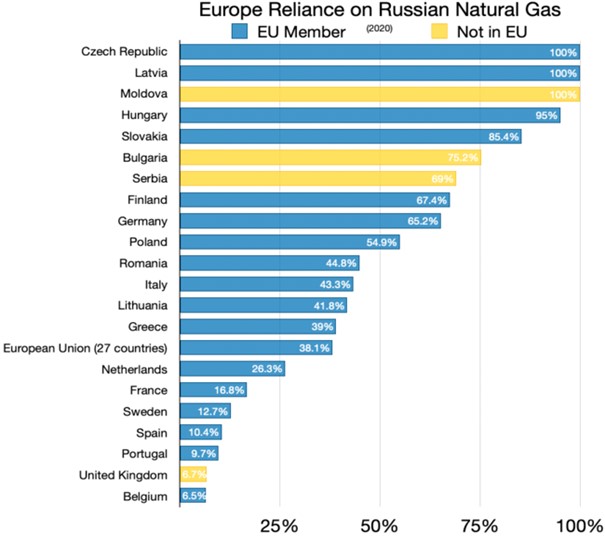

Europe – The European Union has entered the process of phasing out the use of Russian oil and gas throughout the continent by the end of the year in response to the invasion of Ukraine. Before the conflict, Russia supplied the EU with a large chunk of its oil and gas and it has now shut gas supply for a few EU member countries as a response to sanctions. All this turmoil has caused energy costs in Europe to surge, which is resulting in major concerns for Europeans who in many cases cannot afford their utility bills. It’s also not clear when costs will go down again. Without pipelines to get natural gas from western Europe to the east where excess quantities exist, the EU must figure out how to transport it to countries that need a steady supply, especially if Russia starts cutting off supply to even more countries. Countries like Germany are highly reliant on Russian gas to generate electricity and heat their homes. Germany currently relies on Russia for 35 percent of its natural gas. And to some experts, the recent Poland cut-off is just a hint that they could be next. That would cause major issues for the German economy and could lead to an energy crisis.

United States – Natural gas was the largest source – about 38% – of U.S. electricity generation in 2021. America produces more natural gas than it uses, so exports to Europe are possible. In 2020, the United States was able to export 2.7 trillion cubic feet of natural gas. The EU uses about 45 billion cubic feet of natural gas per day and imports 80% of that. So even if the US sent all their extra natural gas to Europe, it would only provide about 75 days’ worth of supply. Even though the amount of gas produced can be increased, that would take state and local governments to revoke their regulations that prevent more production. State and local government obstruction is not the only barrier. The Biden administration is doing everything it can to limit more natural gas production. Biden’s aversion towards natural gas and other fossil fuels is obvious. This creates regulatory uncertainty for firms that then reduce their investments in new production.

US Natural Gas pricing – In a free-market environment like in the US, supply and demand will determine energy prices. The U.S. natural gas prices more than doubled since the start of the year, and this summer’s air-conditioning season could send them soaring by at least another 25%. The higher natural gas prices are heavily hitting U.S. businesses and consumers at a time when gasoline and diesel fuel prices are also at record levels. Analysts say that utilities that normally switch to coal for power when natural gas prices surge are finding that coal is even more expensive — the equivalent of gas at $9 to $10 MMBtu.

US and EU influence on US natural gas – The U.S. has become the world’s leading exporter of liquefied natural gas, meaning that American consumers are increasingly competing with buyers overseas for their own country’s gas production. Most of these exports go to European allies seeking to lessen their reliance on Russian natural gas in response to Moscow’s invasion of Ukraine. While US voters are focusing on the rising prices at the pump and Republicans found an additional reason to attack Biden for what they consider are anti-oil policies, the dynamics around natural gas are shadier. Output of the fuel reached a record last year under Biden and is expected to top that mark this year, despite the promises given to various activist groups and the vows taken at the world economic forum for greener practices.

With the above in mind and especially with the U.S. now increasing its export levels, if the Biden administration chooses to limit Gas production to satisfy their voters base, then in the event of any unpredictable situation, a deficit in the U.S. natural gas market could send prices skyrocketing. This could prove to be a double-edged sword for the Biden administration. The world is seemingly entering into a prolonged energy crisis where the end game is hard to predict.

Sources

repsol.us, cmegroup.com, popsci.com, eia.gov, forbes.com, cnbc.com, politico.com, tradingview.com .

*Disclaimer: The information contained in this publication does not constitute investment advice and is not a personal recommendation from Fortissio. Nothing contained herein constitutes the solicitation of the purchase or sale of type of financial instrument. Any investment activities undertaken using this information will be at the sole risk of the relevant investor. Fortissio expressly disclaims all liability for the use or interpretation (whether by visitor or by others) of information contained herein. Decisions based on this information are the sole responsibility of the relevant investor. Any visitor to this page agrees to hold Fortissio and its affiliates and licensors harmless against any claims for damages arising from any decisions that the visitor makes based on such information.

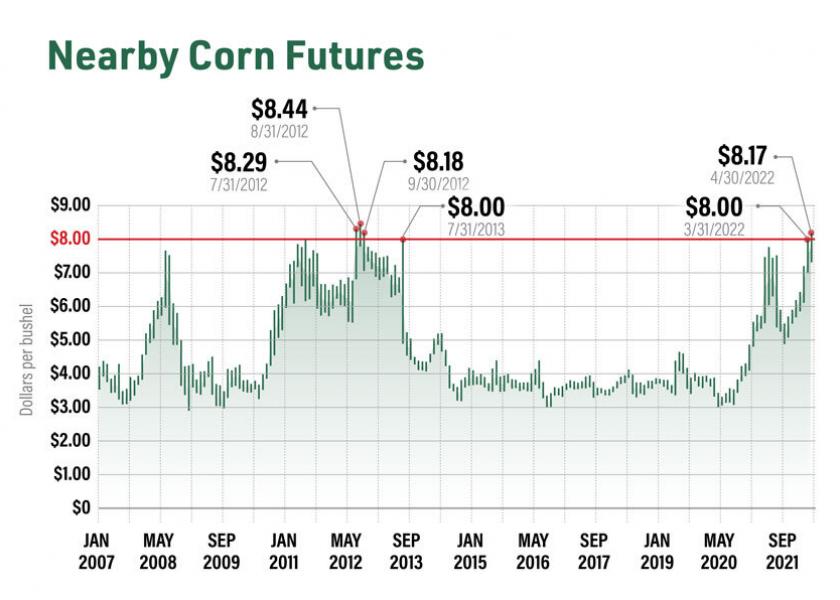

May 18th, 2022 by Nikolay Alexandrov

Corn futures are exchange-traded contracts on the Chicago Board of Trade (CBOT) and are amongst the top 5 most-commonly traded commodity futures. Corn is the most widely grown crop across the United States, and corn futures contracts are the most active commodity in grains and oilseeds.

Corn’s major use is to serve as livestock and poultry feed. It also serves as a crucial ingredient in many of the foods we consume daily as humans such as corn oil for margarine, corn starch for gravy, and corn sweeteners for soft drinks, just to name a few. Non-food uses of corn among others include alcohol for ethanol fuel, absorbing agent for disposable diapers, and adhesives for paper products.

Corn futures are traded electronically on the Globex platform from 01:00 a.m. GMT to 7:20 p.m. GMT, at 5,000 bushels per contract. On March 31, May corn futures traded above $800. Since then, prices have traded close to that level which was last seen in 2013.

China is the second largest producer of Corn, yet even they seem to have problems with covering their needs. The US department of Agriculture reported in April, sales of more than 1 million metric tons of U.S. corn to Chinese buyers. The USDA daily grain sale report showed a Chinese purchase of over 1 million tons of U.S. corn, with 676,000 tons for delivery in the current 2021-22 marketing year and 408,000 tons for delivery in 2022-23. China bought millions of tons of U.S. corn last year as well, most of which it did not take possession, but left on the books. That corn stayed on the books as China ramped up purchases from Ukraine. But after the Russian invasion, China started claiming that U.S. corn.

The sale comes at the same time that a USDA report showed a smaller-than-expected U.S. corn crop this year as well as amid the war in Ukraine that has cut off Ukrainian exports.

Corn is just one of several agriculture commodities that has seen prices surging in the past few weeks, partially due to the war in Ukraine. Ukraine is a major exporter of wheat and other items, such as sunflower oil, while Russia is a key producer of wheat and many of the chemicals used in fertilizer. That is leading futures traders to bet that higher input costs and more demand for corn as a substitute food item will drive up the price.

Even prior to the war, agricultural commodities experienced upward pressure amid supply chain disruptions and high transportation costs that are contributing to inflation throughout the economy.

Another factor for the prices we see today is the drought in the western U.S. and elsewhere in the world, which has also driven prices higher. As of May 1, USDA estimated 14% of the U.S. corn crop has been planted. That compares to a five-year average of 33% planted by this time in the year. Last year, 42% was planted by May 1. This year’s planting pace is the slowest since 2013.

Another determining factor for higher corn prices is ethanol production, which consumes roughly 40% of the U.S. corn crop refined into ethanol. Ethanol processors are still looking for bushels to buy, and are bidding aggressively in the cash market, thus raising the prices.

Fundamentals: It seems lately that better forecasts for producers to close the gap in the planting delay in the US are likely playing a role to the latest correction seen on corn prices. Analysts are expecting the upcoming weekly Crop Progress reports to show the U.S. corn crop increasing but still remaining behind the 5-year average.

Technicals: Corn futures are seen breaking below the support from 770-780. If the Bulls cannot hold the ground above this pocket, we could see additional long liquidation taking prices down towards 747-753. It’s too early to say that the support has cracked. The next days or weeks could prove detrimental for the prices of corn. For now corn steadily holds near the 800-level.

Will corn futures soar even higher towards new historical highs, or will the prices remain under control and correct to lower levels in 2022?

Sources

schwab.com, agweb.com, cnbc.com, agri-pulse.com.

*Disclaimer: The information contained in this publication does not constitute investment advice and is not a personal recommendation from Fortissio. Nothing contained herein constitutes the solicitation of the purchase or sale of type of financial instrument. Any investment activities undertaken using this information will be at the sole risk of the relevant investor. Fortissio expressly disclaims all liability for the use or interpretation (whether by visitor or by others) of information contained herein. Decisions based on this information are the sole responsibility of the relevant investor. Any visitor to this page agrees to hold Fortissio and its affiliates and licensors harmless against any claims for damages arising from any decisions that the visitor makes based on such information.