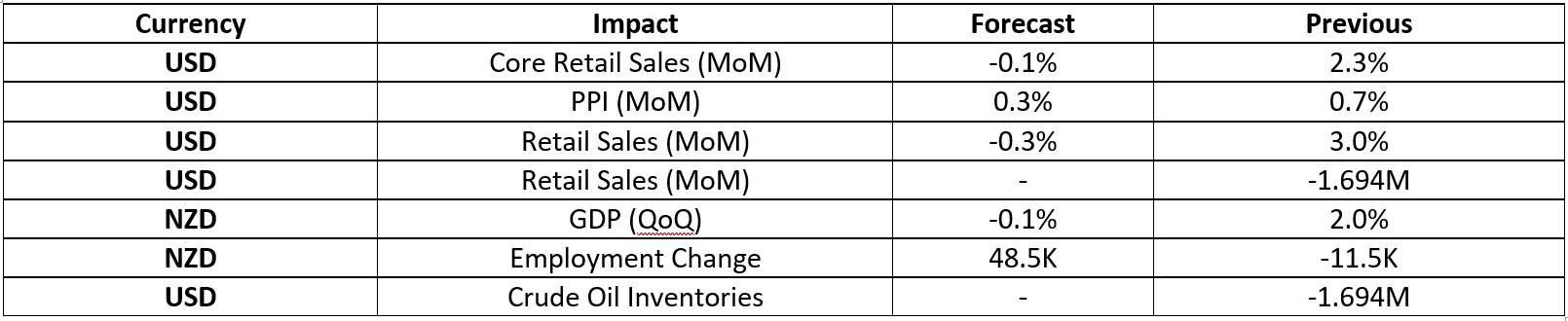

May 10th, 2023 by Nikolay Alexandrov

Global markets finished the week higher

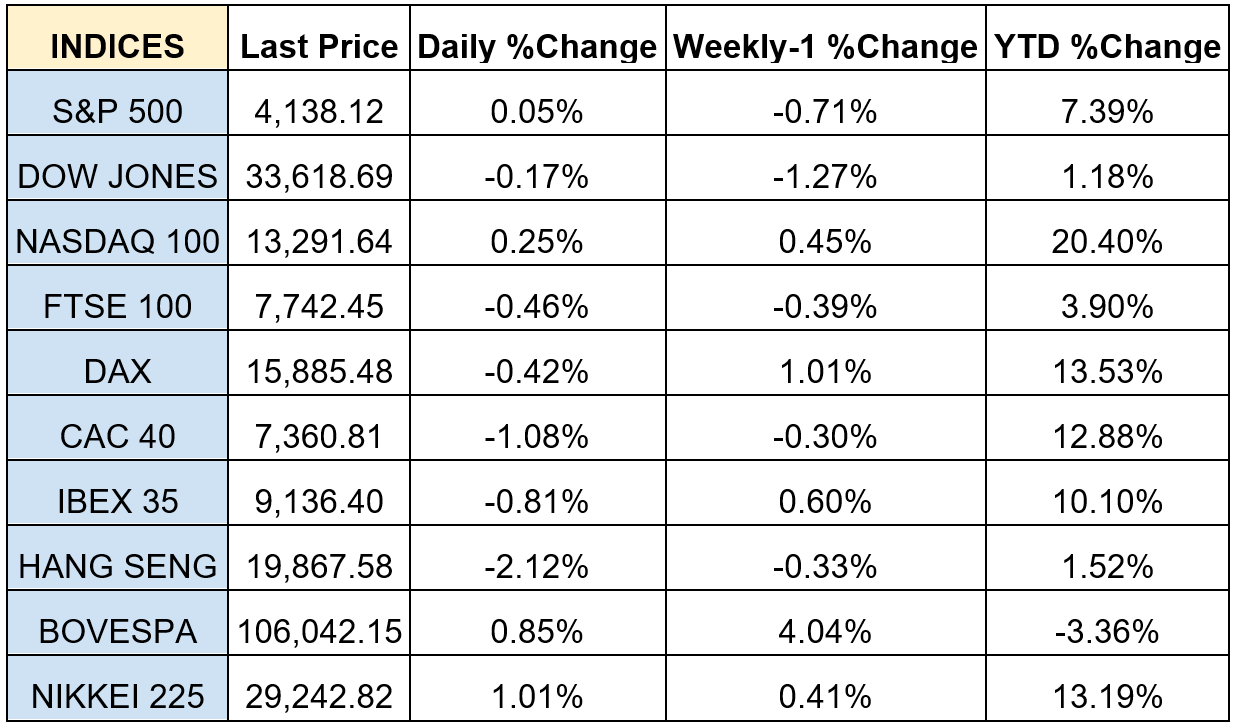

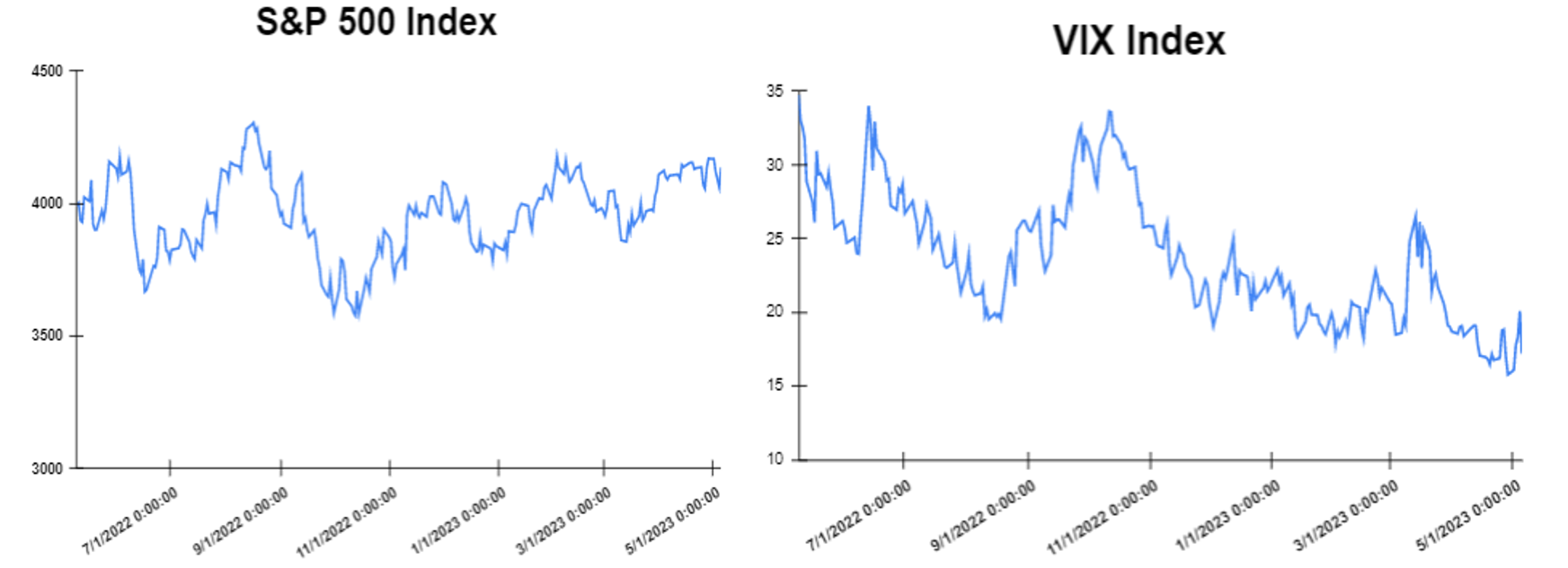

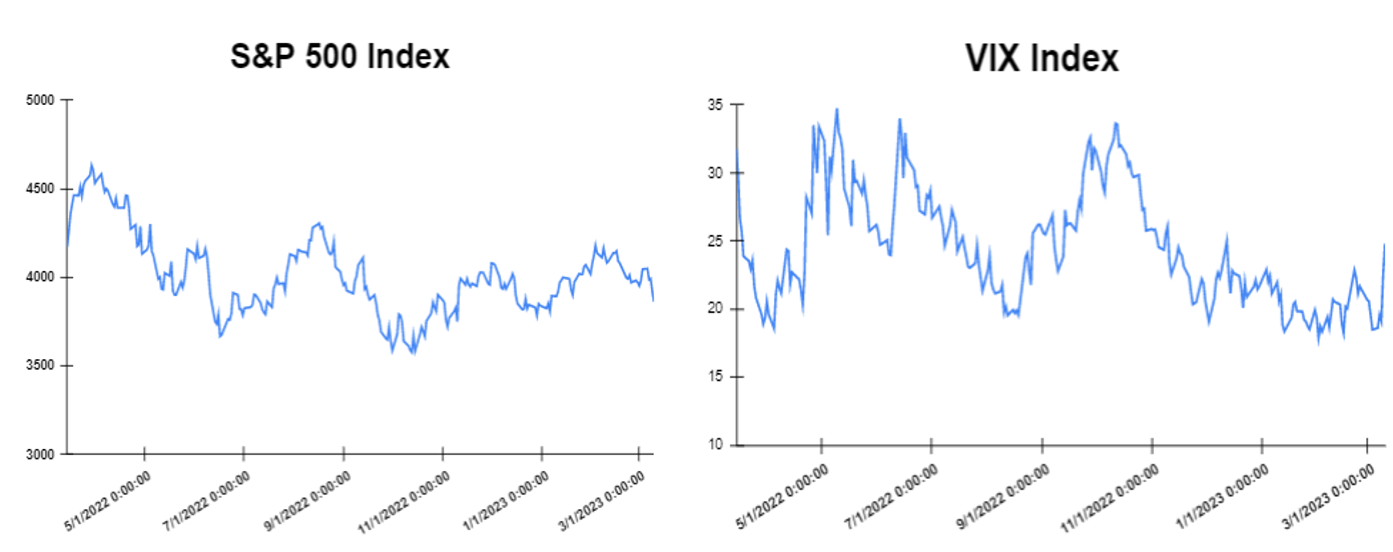

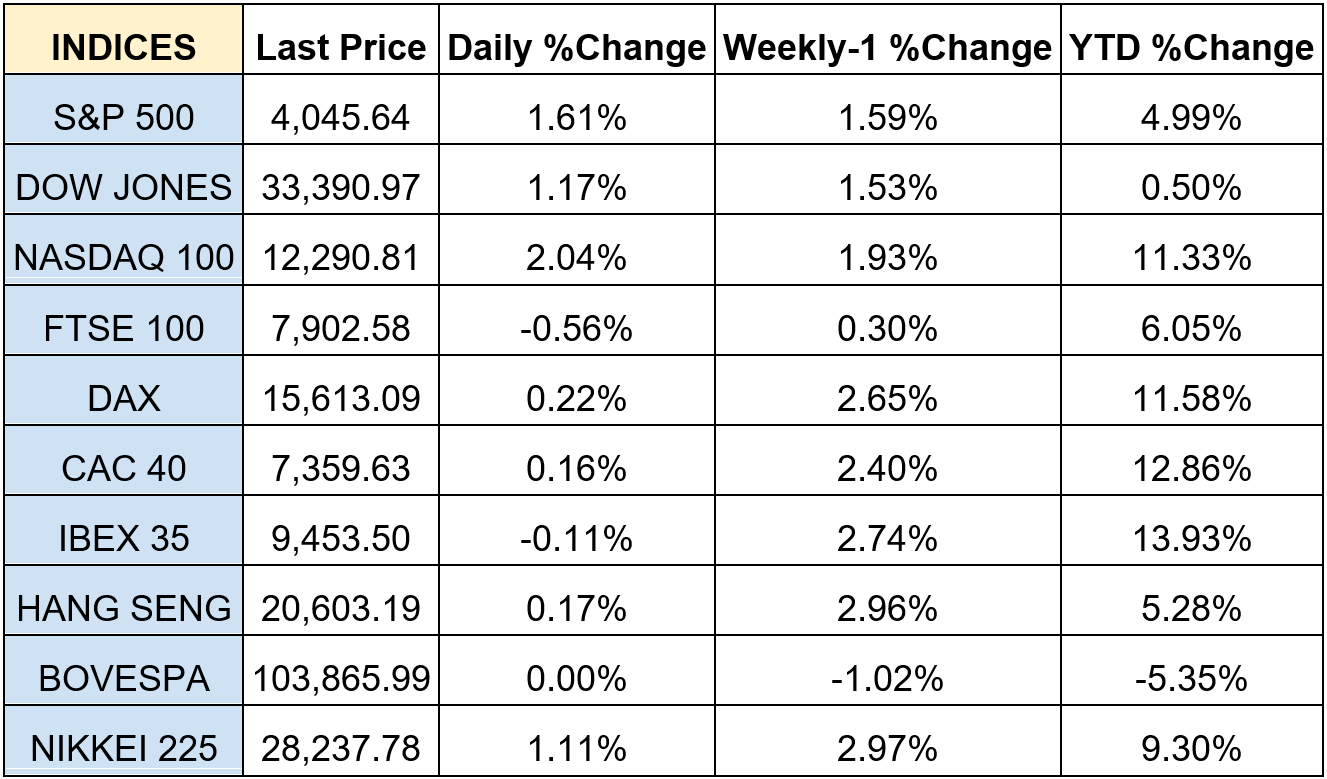

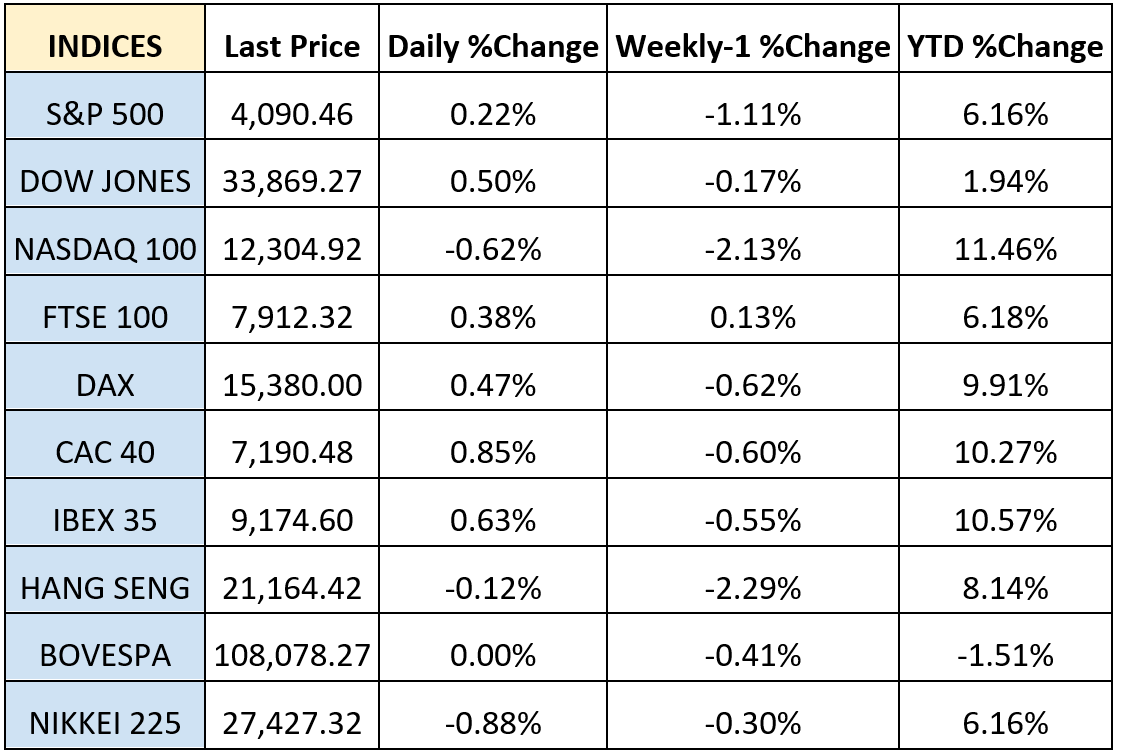

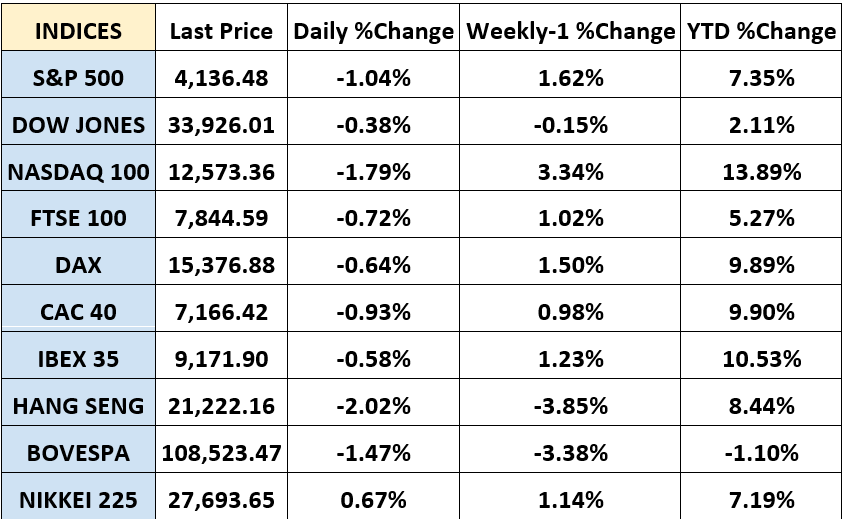

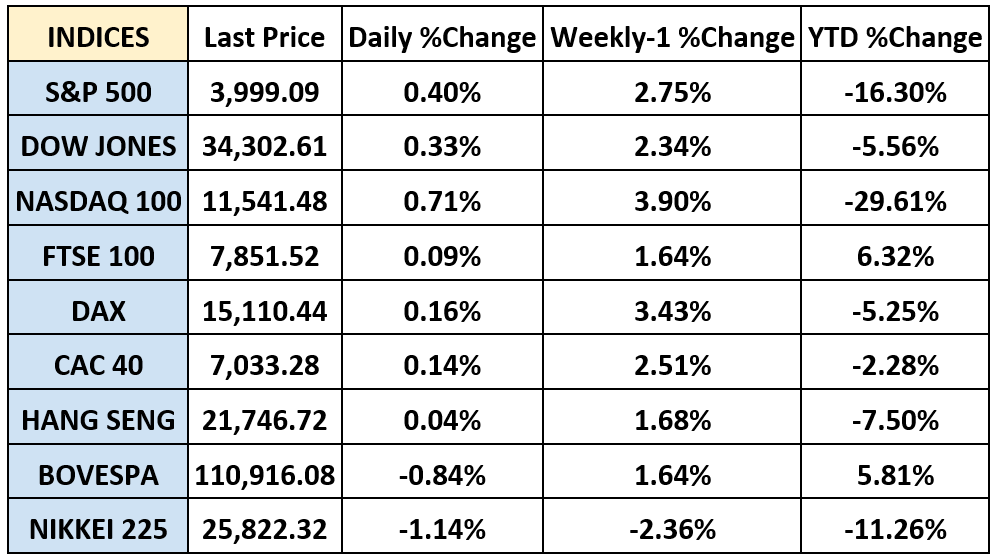

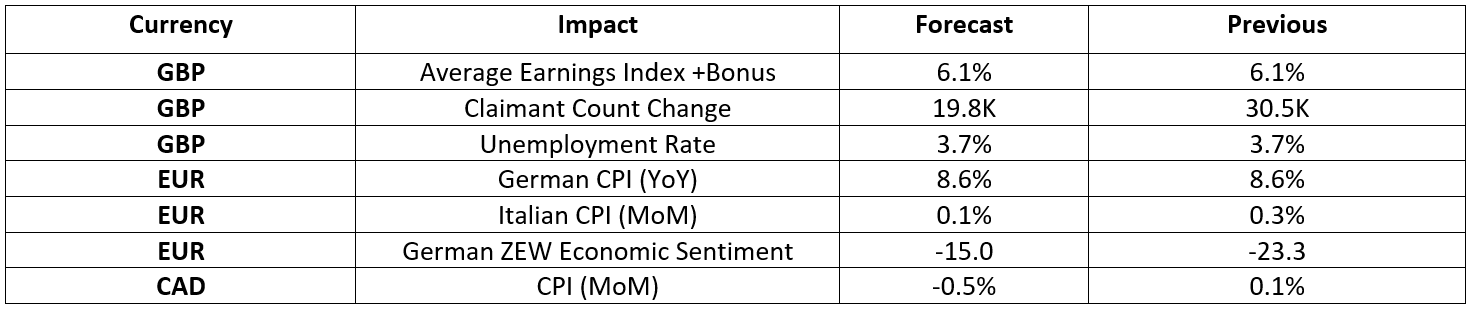

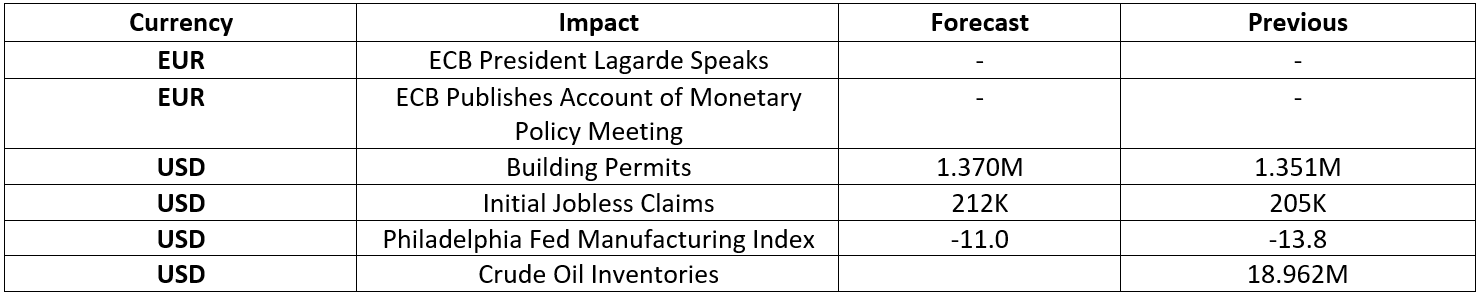

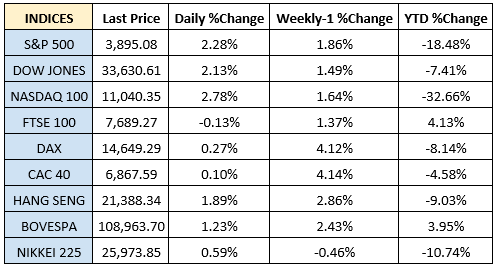

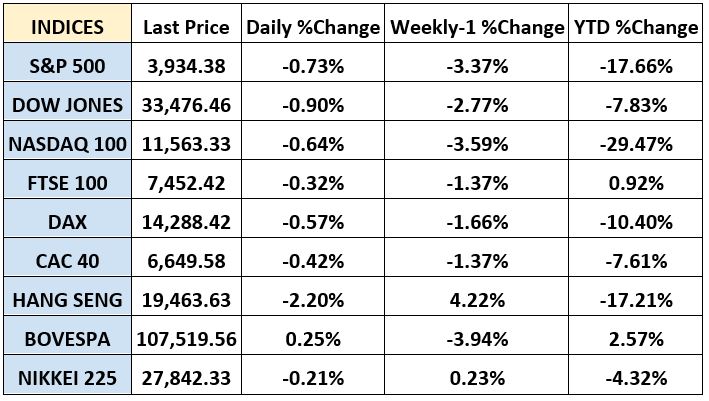

The US market started the week lower after the United States Manufacturing Purchasing Manager’s Index (PMI) stood at 50.2 in April, decreasing by 0.2 index points. Inflation in the Eurozone increased slightly on a yearly basis in April, Eurostat said in a preliminary report on Tuesday. The Consumer Price Index (CPI) grew by 7% year-on-year in April, compared to a 6.9% annual inflation recorded in March, somewhat higher than the forecast. Moreover, on Wednesday, the Federal Reserve of the United States announced a raise in the key interest rate by another 25 basis points and showed uncertainty on whether there will be new hikes in the near future and how much they will be. Specifically, the stock markets on that day closed lower as Chair Powell said that there won’t be any rate cuts if inflation remains high. On Thursday, the European Central Bank (ECB) announced its decision to hike its key interest rate by another 25 basis points as the Governing Council determined that inflation remained too high despite easing somewhat recently. However, on Friday the global market closed with gains after total nonfarm payroll employment in the United States grew by 253,000 in April more than expected, which showed that the labor market remains in healthy shape. Dow Jones traded higher at the closing bell by 1.65% on Friday. The S&P went up by 1.85%. Furthermore, the DAX gained 1.42%, CAC 40 rose by 1.31% and the FTSE 100 advanced by 0.98%. In addition, investors are looking forward to the Bank of England Interest Rate Decision expecting an increase to 4.50% from 4.25%.

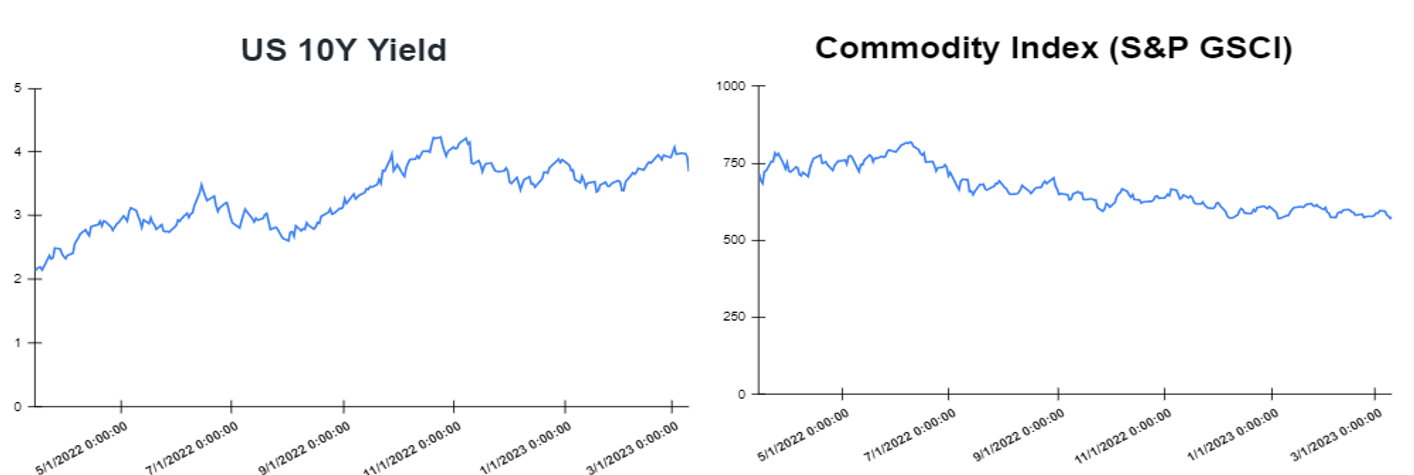

Treasury yields advanced towards the end of the week

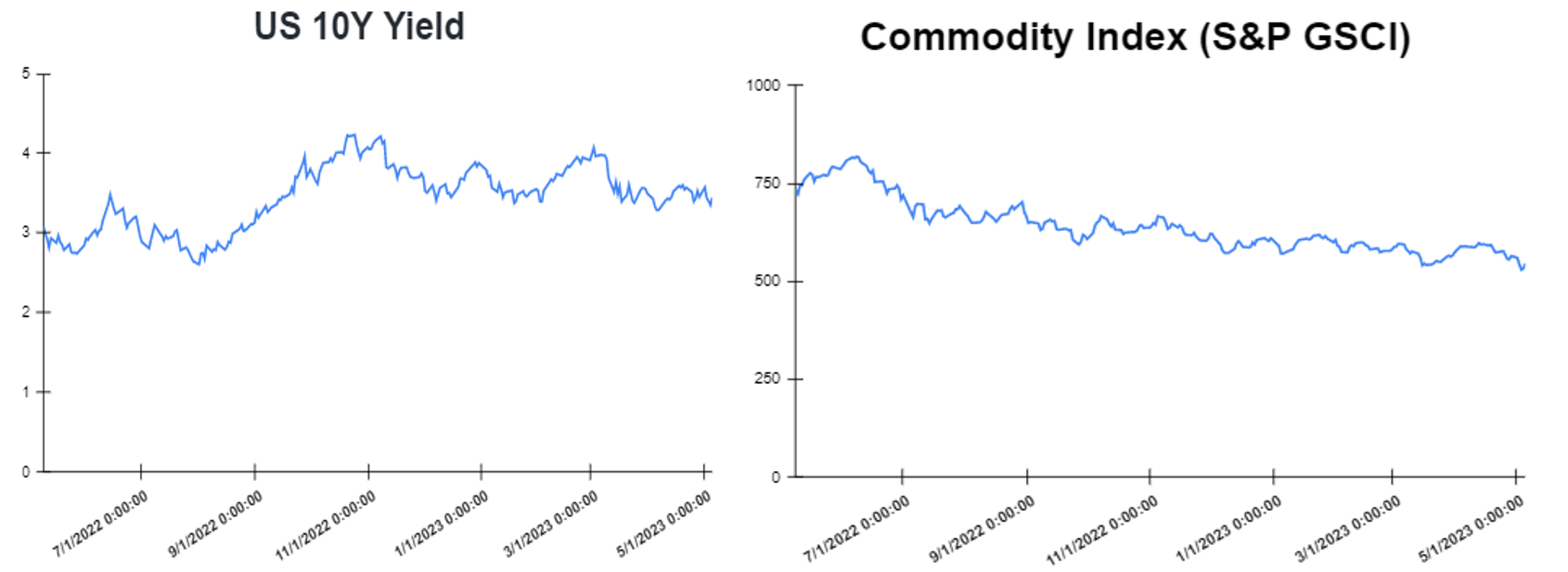

Yields started the week lower as investors sought safe-haven assets and as the Fed softened it’s language about rates hikes. However, yields increased on Friday after the release of nonfarm payrolls in April with the U.S. adding 253,000 new jobs, 73,000 more than expected. Specifically, on Friday, the yield on the 2-year Treasury increased to 3.914%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.439%, up by about 9 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.7620%. The spread between the US 2’s and 10’s declined to -47.5bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) advanced to – 118.4bps. In addition, investors are looking forward to US CPI (YoY) on Wednesday which are expected to stay still at 5%.

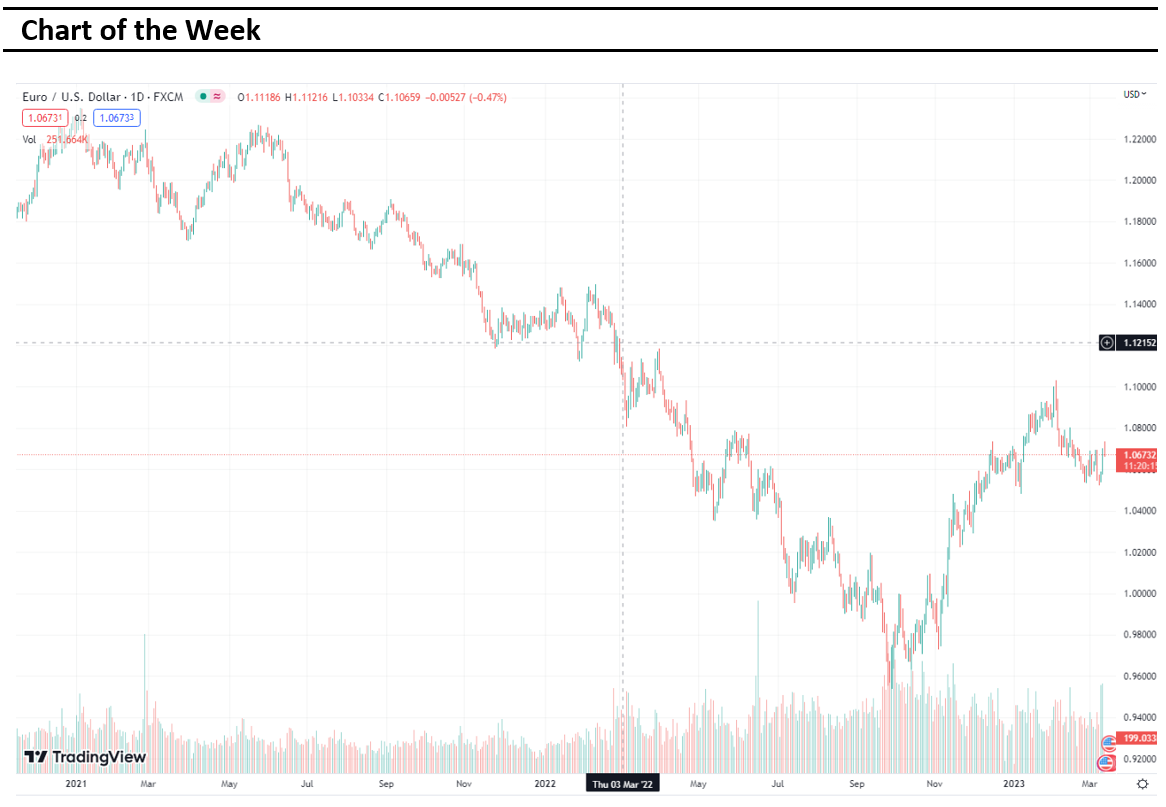

Volatile week for USD

The US Dollar was under a selling pressure at the start of the week following the Fed’s rate decision and Chairman Powell’s comments on the policy outlook. However, after the ECB raised its key interest rates by 25 basis points, the Euro lost ground against the US dollar, with EURUSD dropping below 1.1000. On Friday, the announcements of Nonfarm Payrolls and Unemployment Rate, which ticked down to 3.4%, initially helped the US Dollar to get some demand, but finally it erased its recovery gains. The EURUSD climbed to 1.1026, while the GBPUSD increased to 1.2641. Additionally, the USDJPY raised to 134.79 yen on Friday.

Oil and Gold traded opposite towards the end of the week

Gold started the week higher as the banking sector uncertainties persist. Gold traded lower at the end of the week after a report by the United States Bureau of Labor Statistics revealed that nonfarm employment in the country rose by 253,000 in April, going above analysts’ projections and showing that the labor market is still able to withstand tight monetary conditions. Prices of Oil moved lower at the start of the week, after manufacturing data from China over the weekend fell short of expectations and reignited worries about the global economic recovery. China’s Manufacturing Purchasing Manager’s Index (PMI) stood at 49.2% in April, falling by 2.7 percentage points from the previous month. However, at the end of the week oil moved higher, after Russia promised to continue cutting theoil output, with a target of 500,000 barrels per day. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show a decrease of 0.320M.

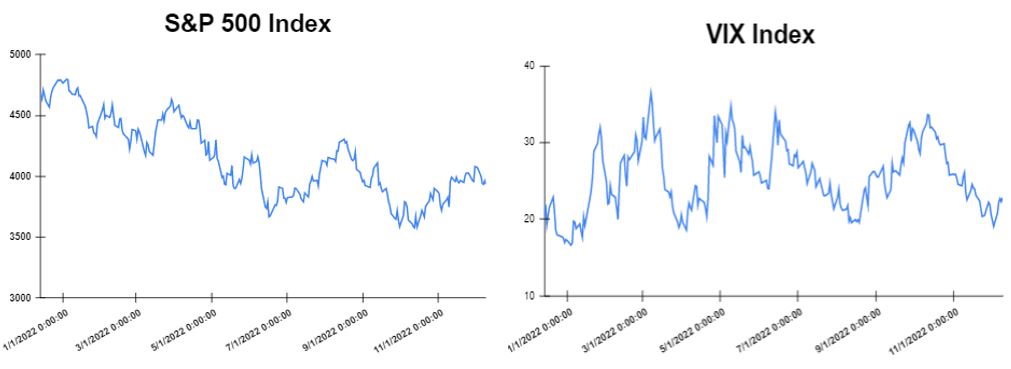

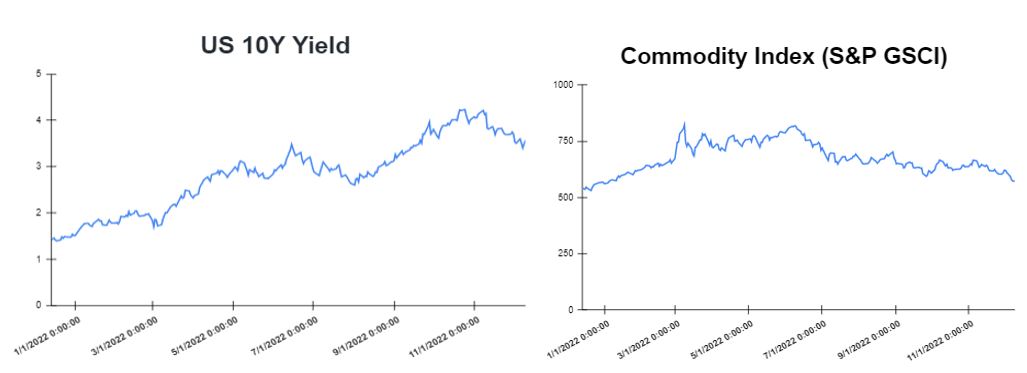

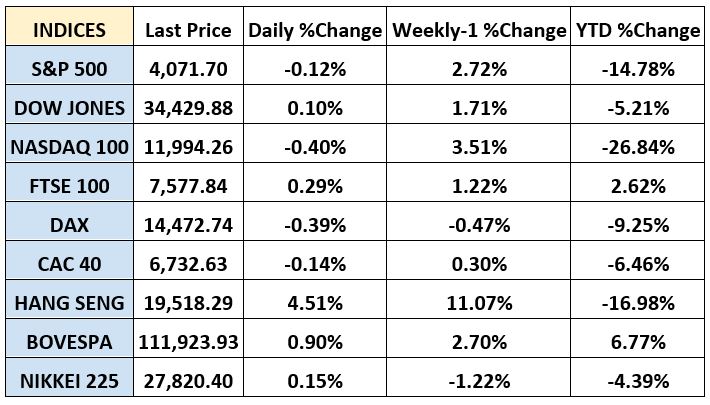

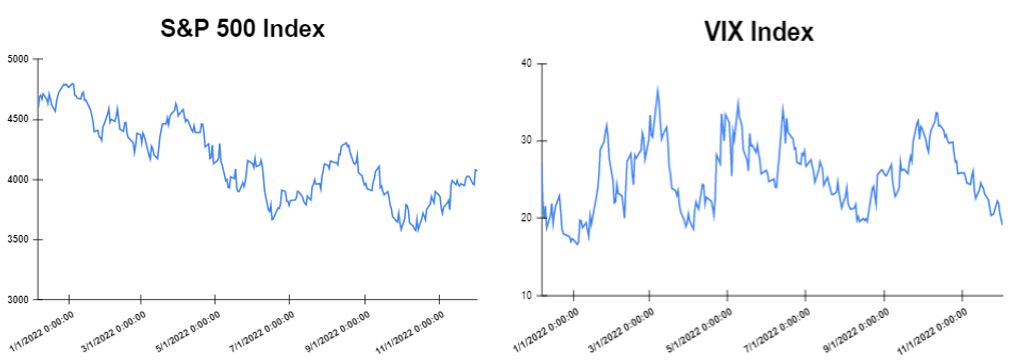

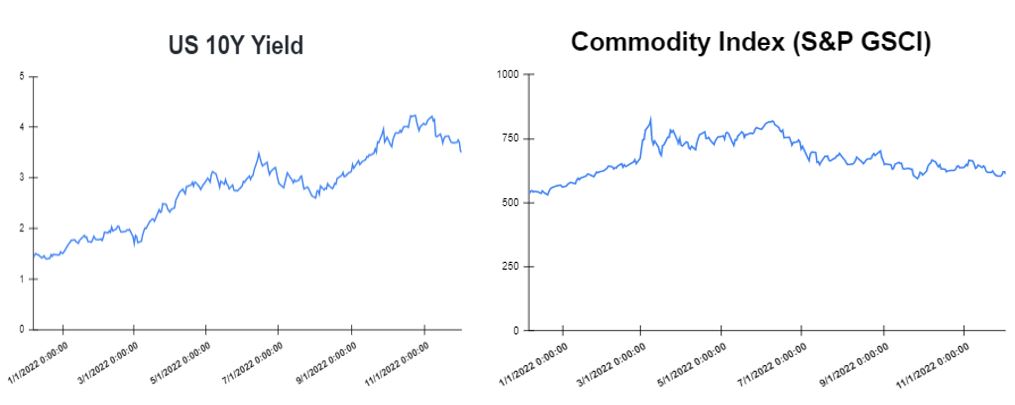

Stock indices performance

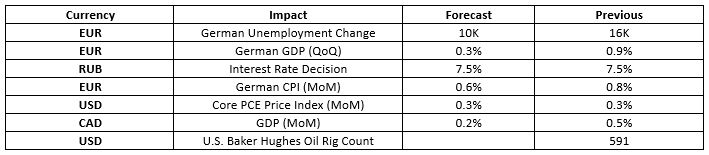

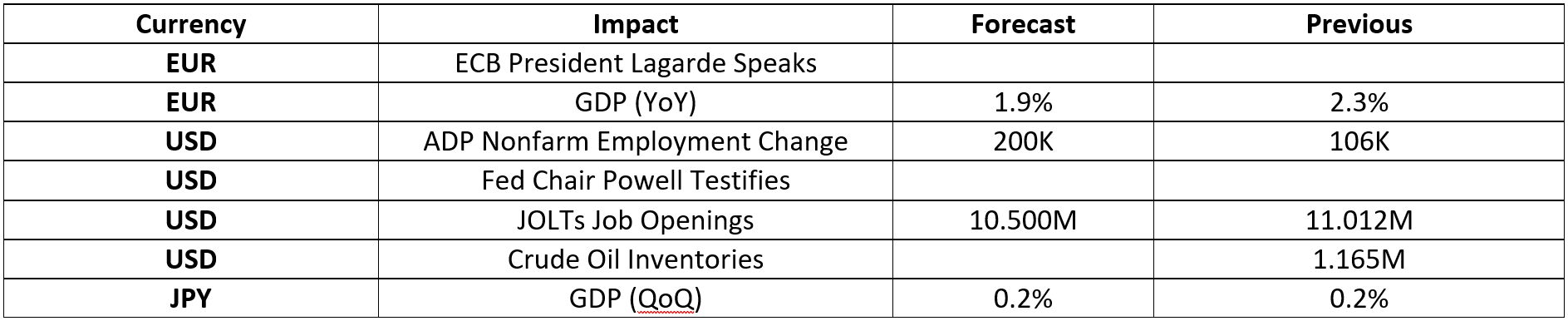

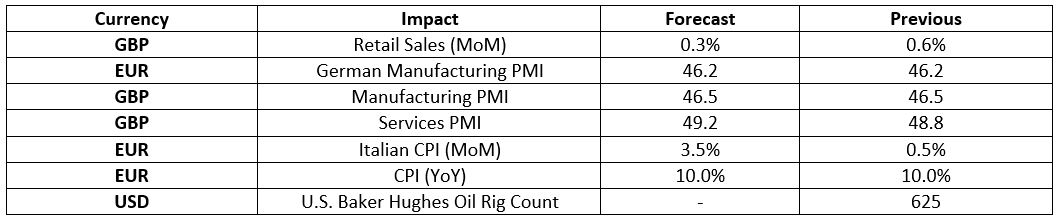

Key weekly events:

Monday – 08 May 2023

Tuesday – 09 May 2023

Wednesday – 10 May 2023

Thursday – 11 May 2023

Friday – 12 May 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/

https://www.investing.com/

https://www.fxstreet.com/

https://www.cnbc.com/

April 25th, 2023 by Nikolay Alexandrov

Global markets finished the week higher

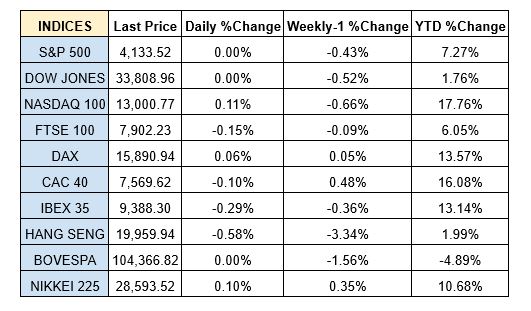

Global markets started the week mixed as investors waited for more first-quarter corporate reports, economic data and statements by Federal Reserve officials that could indicate where the United States central bank will go when it comes to monetary policy in May. In Europe inflation came to 6.9% as expected on a year to year basis. United Kingdom inflation came to 10.1% higher than expected. However, on Friday the market closed with gains according to PMI data for Germany, the euro area and the United Kingdom showed growth in business activity and investors looked toward the next week’s batch of first-quarter corporate earnings results. Dow Jones traded higher at the closing bell by 0.07% on Friday. The S&P went up by 0.09%. Furthermore, the DAX gained 0.54%, CAC 40 rose by 0.51% and the FTSE 100 advanced by 0.15%. In addition, investors are looking forward to US GDP (QoQ) data which expected a decrease to 2.0% from 2.6%.

Treasury yields advanced towards the end of the week

Yields increased on Friday after the release of the United States PMI, reaching its highest point in 11 months which came to 53.5 in April. On Friday, the yield on the 2-year Treasury increased to 4.182%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.568%, up by about 2 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.777%. The spread between the US 2’s and 10’s advanced to -61.4bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) declined to – 104.1bps.

Volatile week for USD

The US Dollar moved sideways after the US showed an increase in Initial Jobless Claims to 245,000. Therefore, on Friday US Dollar was slightly higher as business activity data suggested that the world’s largest economy remained resilient, supporting expectations of another 25-basis-point interest rate increase by the Federal Reserve at next month’s policy meeting. The EURUSD climbed to 1.0982. GBPUSD declined by 0.1% to 1.2431. Additionally, the USDJPY dropped to 134.17 yen on Friday.

Oil and Gold traded lower towards the end of the week

Gold started the week lower after comments from Federal Reserve officials on the path of interest rate hikes triggered a heavy dose of profit taking in the prior session. Gold traded lower at the end of the week after Federal Reserve officials hinted at additional monetary tightening, offsetting optimism that the policymakers could soon wrap up the interest rate cycle. Prices of Oil moved lower at the start of the week, after Federal Reserve Bank of Richmond President Thomas Barkin said that more is still needed to prove that inflation in the United States is on a consistent way down. However at the end of the week, the U.S. rate hike and recession fears have cut into the OPEC+-hyped rally in crude, handing oil bulls their first week of losses after a four-week winning streak. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show a decrease of 3.493M.

Stock indices performance

Key weekly events:

Monday – 24 April 2023

Tuesday – 25 April 2023

Wednesday – 26 April 2023

Thursday – 27 April 2023

Friday – 28 April 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

March 14th, 2023 by Nikolay Alexandrov

Global markets finished the week lower

Global markets started the week mixed as investors digested the latest batch of economic data in Europe, which sent mixed signals about the state of the continent’s economy. On Tuesday markets moved sharply lower (S&P dropped by 1.5%) after Federal Reserve Chair Jerome Powel warned that the central bank will likely have to increase its key interest rates higher than policymakers initially expected because latest economic data have come stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated. Moreover, initial jobless claims in the United States on Thursday, increased higher than expected by 21,000 to reach 211,000 in the week ending March 3, raising hopes that a softening labor market will reduce the likelihood of the Federal Reserve reaccelerating the pace of its rate hikes. However, the nonfarm payroll employment in the United States increased to 311,000 in February, well above the expectation of 215,000, which demonstrates the strength of the labor market. In other news, it was confirmed on Friday morning that the Silicon Valley Bank (SVB) was shut down as it was not able to raise capital to boost its finances, causing regulators to take possession of the bank. As a result, the stock markets moved sharply lower. Specifically, the Dow Jones dropped by 1.07% at the closing bell on Friday. The S&P further 500 declined by 1.45%. Furthermore, the DAX sank by 1.64%, CAC 40 tumbled by 1.30% and the FTSE 100 dropped by 1.67%. In addition, investors are looking forward to European Central Bank interest rates decision in which an increase to 3.50% from 3.00% is expected.

Treasury yields declined towards the end of the week

Yields significantly declined on Friday after new jobs data showed thatthe unemployment rate rose by 0.2% points to 3.6 signalling that the labor market may be cooling off. Also, this decline is due to investors increasing their demand for bonds which are seen as a safe-haven asset, after this uncertainty and the potential economic slowdown. On Friday, the yield on the 2-year Treasury decreased to 4.738%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.81%, down by about 11.3 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.804%. The spread between the US 2’s and 10’s widened to -92.8bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) widened to – 127.6bps.

Volatile week for USD

The US Dollar fell after the US employment report, which showed a slower wage growth and a rise in the unemployment rate to 3.6%. The EURUSD rose ny 0.57% to 1.0650, while the GBPUSD rose ended the week higher at 1.2040 (up by 0.83%). Additionally, the USDJPY fell to 135.022 yen on Friday after the Bank of Japan kept its policy rate, the Yield Curve Control parameters and guidance unchanged. Furthermore, the USDCHF suffered the worst weekly loss since November (-1.5%) and the USDCAD gained over 200 pips over the week, posting above 1.3800, the second-highest weekly close since May 2020.

Oil and Gold traded higher towards the end of the week

Gold started the week lower as the investors prepared for Congressional testimony from Federal Reserve Chair Jerome Powell this week and monthly U.S. jobs data, both of which could influence interest rate policy. Gold traded higher at the end of the week after better-than-expected nonfarm payrolls jobs report, which showed that the US added 311,000 jobs in February, while the unemployment rate unexpectedly rose by 0.2 percentage points to 3.6%. Prices of Oil moved lower at the start of the week, as investors worry about a potential recession and a reduce future oil demand. However, on Friday, the prices of oil futures gained as optimism about increased demand in the United States grew. Meanwhile, the Crude Oil Inventories report will be released on Wednesday.

Stock indices performance

Key weekly events:

Tuesday – 14 March 2023

Wednesday – 15 March 2023

Thursday – 16 March 2023

Friday – 17 March 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

March 9th, 2023 by Nikolay Alexandrov

Global markets finished the week higher

Global markets started the week higher following their worst week of the year. Pending home sales in the United States, which was released on Monday, jumped 8.1% in January higher than expected, after a slight decline in mortgage rates in December and January. On the same day, the European Union and the United Kingdom confirmed reaching a deal on the “Windsor Framework”, that is expected to resolve some issues in Northern Ireland that were left unaddressed by the two sides’ post-Brexit trade agreement, sealed over three years ago. Moreover, on Wednesday markets were mostly lower after Federal Reserve hinted that they will be open to rate hikes between 25-50 basis points in the next central bank meeting. In other news, the Eurozone business activity accelerated further in February as the Eurozone Purchasing Managers’ Index (PMI) Composite Output Index came in at 52.0, reaching its eight-month high. Moreover, growth in activity in the United States services industry (ISM Services PMI) stood at 55.1% in February, 0.1 percentage point lower than January’s reading of 55.2 percent. The Dow Jones gained 1.17% at the closing bell on Friday. The S&P 500 advanced by 1.61%. Furthermore, the DAX jumped by 1.64%, CAC 40 rose by 0.88% and the FTSE 100 ended the session flat. In addition, investors are looking forward to the US Nonfarm Payrolls report on Friday, 10 of March, which is expected to post an increase of 200K for February, versus a 517K increase for January.

Treasury yields declined towards the end of the week

Yields slightly declined on Friday after investors weigh the prospect of further interest rate hikes by the Federal Reserve. The yields moved markedly higher over the last month, prompting a pullback for the Stock markets in February. This rise indicates that traders are convinced that rates will stay higher for longer. On Friday, the yield on the 2-year Treasury decreased to 4.863%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.969%, down by about 10 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.888%. The spread between the US 2’s and 10’s widened to -89.4bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) tightened to – 124.9bps.

Volatile week for USD

The US Dollar fell by 0.3% to 104.60, from as high as 105.36 at the start of the week, its strongest level since January. 6th and moved lower towards the end of the week after the Institute for Supply Management’s (ISM) non-manufacturing index dipped to 55.1 from 55.2 in January. The EURUSD traded higher by 0.3% at 1.0628, after starting the week at a nearly two-month low of 1.0533. Furthermore, the GBPUSD rose by 0.7%, ending the week higher at 1.2032. The pound’s gains came as Britain struck a post-Brexit Northern Ireland trade deal with the European Union. Additionally, the USDJPY eased by 0.4% to 136.26 yen on Friday, after climbing to 137.10 on Thursday, the highest since December. 20th .

Oil and Gold traded higher towards the end of the week

Gold started the week higher after US dollar fell after missed expectation on series of USA data. Gold traded higher at the end of the week after Atlanta Fed President Raphael Bostic reiterated the case for a 25 basis point hike in March. Prices of Oil moved lower at the start of the week, as investors worry about Federal Reserve’s future monetary policy. In addition, on Friday, the prices of oil futures gained as global economy raised demand concerns. Meanwhile, the Crude Oil Inventories report will be released on Wednesday. A decrease is expected in the number of barrels held by US firm by 3.764M.

Stock indices performance

Key weekly events:

Monday- 06 March 2023

Tuesday – 07 March 2023

Wednesday – 08 March 2023

Thursday – 09 March 2023

Friday – 10 March 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

February 17th, 2023 by Nikolay Alexandrov

Global markets finished the week mix.

Global markets started the week lower. Euro Retail sales decreased by 2.8% year-on-year in December, a third consecutive drop, and slightly worse than market forecasts of a 2.7% decline. Investors were still concerned over the FED future interest rates increases. However, the markets have been taking some encouragement off recent remarks from Fed Chairman Jerome Powell, who has said that he is seeing disinflationary signs. Moreover, on Thursday US market was lower after higher-than-expected initial jobless claims. Initial jobless claims in the United States rose by 13,000 to 196,000 in the week ending February 4. The Dow Jones increased by 0.50% at the closing bell on Friday. The S&P 500 gained by 0.22%. Furthermore, the DAX fell by 1.39%, CAC 40 declined by 0.88% and the FTSE 100 retreated by 0.36%. In addition, investors are looking forward for inflation data for GBP and USA on Tuesday and Wednesday on which a decrease for both is expected.

Treasury yields advanced towards the end of the week.

Yields advanced after a better-than-expected consumer confidence, in which there was an increase by 2.3% on a monthly basis to 66.4 points in February. The yield on the 2-year Treasury increased to 4.53%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.745%, up by about 6 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.823%. The spread between the US 2’s and 10’s tightened to -70.7bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) widened to – 138.9bps.

Volatile week for USD.

The US Dollar moved higher towards the end of the week after investors concerns about US inflation reports next week. The EURUSD fell by 0.2% on Friday to 1.0777 despite German industrial orders rising by a larger than expected 3.2% in the month in December. The GBPUSD fell by 0.1% to 1.2040, having touched a one-month low of 1.2031 earlier on Monday. The UK economy stagnated in the fourth quarter as expected. On a monthly basis, the Gross Domestic Product contracted by 0.5%. Moreover, the AUDUSD rose by 0.1% to 0.6924, NZDUSD fell by 0.2% to 0.6320, while USDCNY rose by 0.1% to 6.7806, with the yuan weakening on the rising political tensions with the U.S.

Oil and Gold traded opposite towards the end of the week.

Gold started the week lower after fears that the FED would continue to keep raising interest rates. However, Gold traded lower at the end of the week after a rising form short-term yields. Prices of Oil moved higher at the start of the week, as European Union put embargo on Russian refined petroleum products imports. However, Oil traded higher in the middle of the week after crude oil inventories in the United States increased by 2.4 million barrels to 455.1 million barrels in the week ending February 3. In addition, on Friday, the prices of oil futures rose following news that Russia plans to cut oil production by 500,000 barrels per day in March. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show a decrease by 2.102M.

Stock indices performance

Key weekly events:

Monday- 13 February 2023

Tuesday – 14 February 2023

Wednesday – 15 February 2023

Thursday – 16 February 2023

Friday – 17 February 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/

https://www.investing.com/

https://www.fxstreet.com/

https://www.cnbc.com/world/

February 8th, 2023 by Nikolay Alexandrov

Global markets finished the week mix

Global markets started the week lower. Germany’s gross domestic product (GDP) declined by 0.2% in the fourth quarter of 2022 compared to the previous three-month period, slightly more than analysts predicted. In addition Consumer confidence in the United States declined in January, at 107,1 down from the predicted 109.0. Moreover, on Wednesday markets were mix after lower than expected inflation in Europe. Furthermore, US Federal Reserve interest rate rose by 25 basis points. Lastly, both European Central Bank and Bank Of England’s raised their interest rates by 50 basis points as expected. The Dow Jones dropped by 0.38% at the closing bell on Friday. The S&P 500 declined by 0.25%. Furthermore, the DAX fell by 0.21%, CAC 40 rose by 0.94% and the FTSE 100 surged 1.04%, reaching its all-time high. In addition, investors are looking forward for the Initial Jobless Claims on Thursday, which is expected to grow to 190K from the previous 183k.

Treasury yields advanced towards the end of the week

Yields advanced after a better than expected Nonfarm payrolls. Increased by 517000 jobs for January, particularly above the 187,000 additions estimated by Dow Jones. In addition, the unemployment rate fell to 3.4%, lower than the 3.6% expected by Dow Jones. The yield on the 2-year Treasury increased to 4.299%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.526%, up by about 12 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.627%. The spread between the US 2’s and 10’s widened to -77.3bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) widened to – 131.3bps.

Volatile week for USD

The US Dollar moved higher towards the end of the week after better than expected non – farm payrolls in USA potentially giving the Federal Reserve more leeway to keep hiking interest rates. In addition, initial jobless claims in the United States declined by 3,000 to 183,000 in the week ending January 27. Therefore, the EURUSD traded lower at 1.08040. Furthermore, the GBPUSD ended the week lower at 1.20550 and the USDJPY traded higher at 131.20 on Friday.

Oil and Gold traded lower towards the end of the week

Gold started the week lower after concerns over economic key events. However, Gold traded higher in the middle of the week further to the Federal Reserve’s decision to raise interest rates by another 25 basis points. Gold traded lower at the end of the week after better than expected non – farm payrolls in USA showing the labor market still remaining strong despite a tight monetary policy. Prices of Oil moved lower at the start of the week, as investors waited for the next meeting between the Organization of the Petroleum Exporting Countries (OPEC) and its Russia-led partners due on February. However, Oil traded lower in the middle of the week after crude oil in the country’s stockpiles increased by 4.1 million barrels since a week ago. In addition, on Friday, the prices of oil futures fell as global economy raised demand concerns. Meanwhile, the Crude Oil Inventories report will be released on Wednesday. A decrease is expected in the number of barrels held by US firm by 3.764M

Stock indices performance

Key weekly events:

Monday- 06 February 2023

Tuesday – 07 February 2023

Wednesday – 08 February 2023

Thursday – 09 February 2023

Friday – 10 February 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/

https://www.investing.com/

https://www.fxstreet.com/

https://www.cnbc.com/

January 27th, 2023 by Nikolay Alexandrov

Global markets finished the week higher

Global markets started the week mixed. European Central Bank noted that “the near-term growth outlook is weaker for the Euro Area than for the United States” and ECB official Isabel Schnabel stated that interest rates will have to “rise significantly.” In addition, US markets gained in the middle of the week after Boston Federal Reserve President Susan Collins said she would support a 25 basis point rate hike that would allow the central bank to “assess the incoming data before we make each decision”. Furthermore, the annual inflation rate in the United States marked the sixth consecutive decline in December, landing at the expected 6.5%. The week finished higher, as both the United Kingdom’s and Eurozone trade deficits shrunk, while the Euro Area’s industrial production increased by 1% and the UK GDP rose by 0.1%. The Dow Jones gained 0.33% at the closing bell on Friday. The S&P 500 increased by 0.40%. Moreover, the DAX rose up by 0.19%. The CAC 40 increased by 0.69% and the FTSE 100 was up by 0.64% at the close. In addition, investors are looking forward for the inflation data in Europe and UK on Wednesday.

Treasury yields advanced towards the end of the week

Yields advanced after the latest inflation report. Thursday’s consumer price index report was in line with expectations, showing that prices of goods and services fell by 0.1% in December on a monthly basis. Investors are now concerned regarding the Fed’s next increase rate decision on February 1, as uncertainty about whether the Central Bank will then hike rates by 25 or 50 basis points has spread. The yield on the 2-year Treasury increased to 4.224%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.504%, up by about 5 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.624%. The spread between the US 2’s and 10’s widened to -72bps, while the

Volatile week for USD

The US Dollar moved lower this week after data showed U.S. inflation was easing, prompting bets that the Federal Reserve will be less aggressive with rate hikes going forward. U.S. data showed the consumer price index (CPI) dipped by 0.1% last month, marking the first decline in the data since May 2020, when the economy was reeling from the first wave of COVID-19 infections. Therefore, the EURUSD traded higher at 1.0845. Furthermore, the GBPUSD ended the week higher at 1.22195 and the USDJPY traded lower at 127.92 on Friday. Adding up, investors are looking forward to the Initial Jobless Claims in US, due to be released on Thursday, in which an increase to 213K from 205K is expected.

Oil and Gold traded higher

Gold started the week with profits after signs of a cooling jobs market pushed up expectations for a softer U.S. inflation. However, Gold traded higher in the middle of the week amid bets that a U.S. inflation report due in the next 24 hours would push the Federal Reserve to go easier with its rate hikes this year. Gold traded higher at the end of the week after softening U.S. inflation and rate hike expectations boosted contrarian safe-haven trades. Prices of Oil moved higher at the start of the week, amid expectations that China’s decision to ease some of its measures imposed to curb the spread of COVID-19 would boost demand for the commodity. However, on Friday, the prices of oil futures jumped higher, as optimism about increased demand grew in the world’s second largest importer of the commodity. Meanwhile, the Crude Oil Inventories report will be released on Thursday.

Stock indices performance

Key weekly events:

Monday- 16 January 2023

Tuesday – 17 January 2023

Wednesday – 18 January 2023

Thursday – 19 January 2023

Friday – 20 January 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/

https://www.investing.com/

https://www.fxstreet.com/

https://www.cnbc.com/

January 27th, 2023 by Nikolay Alexandrov

Global markets finished the week higher

Global markets started the week mixed. The Germany CPI rose by 8.6% in December, lower than the 9% which was the forecast on consumer prices. Moreover, manufacturing activity in the United States declined further in December, according to a report released by S&P Global on Tuesday. The adjusted S&P Global US Manufacturing Purchasing Managers Index (PMI) came in at 46.2, down from the 47.7 recorded in November and unchanged from the preliminary estimate for December. In addition, European markets continue with gains in the middle of the week after Eurozone Services Business Activity Index rose to 49.8 in December, up from the 48.5 in the previous month, signalling the lowest decrease since August. Furthermore, according to the Mortgage Bankers Associations, mortgage applications in the United States dropped by 13.2% from two weeks earlier, hitting the lowest level since 1996. The week finished higher, as the potential weakening in monetary tightening brought optimism in global markets Adding up, the latest jobs report showed nonfarm payrolls grew by a larger-than-expected 223,000. The Dow Jones gained 2.13% at the closing bell on Friday. The S&P 500 increased by 2.28% %. Moreover, the DAX rose up by 1.20%. The CAC 40 increased by 1.39% and the FTSE 100 was up by 0.87% at the close. In addition, investors are looking forward for the Initial Jobless Claims on Thursday, which is expecting to grow to 215k from previous 204k.

Treasury yields declined towards the end of the week

Yields declined after the better-than-expected Nonfarm payrolls. Total nonfarm payroll employment in the United States rose by 223,000 in December 2022, the country’s Bureau of Labor Statistics revealed in its report published on Friday. The figure topped analyst expectations, but came in lower than the November reading of 263,000. The yield on the 2-year Treasury decreased to 4.264%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.567%, down by about 16 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.689%. The spread between the US 2’s and 10’s narrowed to -69.7bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) narrowed to – 133.7bps. Meanwhile, investors are looking to December consumer inflation in the US, due to be released on Thursday, in which a pullback is expected in the y/y to 6.5% from 7.1%.

Volatile week for USD

The US Dollar moved lower this week after stronger than expected nonfarm payroll employment in the United States, which was rose by 223,000 in December 2022. Specifically, the dollar initially fell on Friday after U.S. Wages also grew by 0.3% last month, less than the 0.4% in November and below forecasts of 0.4%. That lowered the year-on-year increase in wages to 4.6% from 4.8% in November. Therefore, the EURUSD traded higher at 1.0645. Furthermore, the GBPUSD ended the week higher at 1.21691 and the USDJPY traded lower at 132.07 on Friday.

Oil and Gold traded opposite

Gold started the week with profits as investors are focusing on the Federal Reserve, as the central bank is expected to reveal its minutes from the last monetary policy meeting on Wednesday. However, Gold traded lower in the middle of the week following uncertainty over the upcoming Fed minutes. Gold traded higher at the end of the week after better than expected nonfarm payrolls. Prices of Oil moved lower at the start of the week, as the reports showed that manufacturing activity in China, the United States and the United Kingdom continued to decline in December. Prices of Oil moved lower in the middle of the week, as investors are concerned about a recession. However, on Friday, the prices of oil futures was flat, as the US Jobs growth couldn’t help the increase of oil. Meanwhile, the Crude Oil Inventories report will be released on Wednesday.

Stock indices performance

Key weekly events:

Tuesday – 10 January 2023

Wednesday – 11 January 2023

Thursday – 12 January 2023

Friday – 13 January 2023

Sources:

www.tradingview.com/

www.breakingthenews.net/

www.investing.com/

www.fxstreet.com/

www.cnbc.com

January 27th, 2023 by Nikolay Alexandrov

Global markets finished the week mixed

Global markets started the week lower as for the fifth straight month in November the Eurozone economic activity declines. The Eurozone Purchasing Managers’ Index (PMI) Composite Output Index settled at 47.8 in November. Moreover, ISM service sector data increased for the 30th consecutive month reaching 56.5%. In addition, European markets continue with losses in the middle of the week after European Central Bank predicted inflation will continue to rise over the next months, despite eurozone’s GDP which came above expectations. Furthermore, in US there is a possibility of a recession. This had a negative reaction on the market, with the NSDQ shrinking by 0.45% on the day, the 10-year yield moving below 3.431% and the US dollar falling around 0.38%. The week finished mixed in global markets as there are concerns about potential rate hikes next week. The Dow Jones gained 0.10% at the closing bell on Friday. The S&P 500 declined by 0.12%. Moreover, the DAX edged up 0.27%. The CAC 40 dropped by 0.17% and the FTSE 100 stood flat at the close. In addition, investors are looking forward for the interest rate decision in Europe, UK and US on Wednesday and Thursday.

Treasury yields advanced towards the end of the week

Yields advanced after the better-than-expected November’s producer price index. Producer prices in the United States rose by 0.3% in November on a monthly basis, the Bureau of Labor Statistics revealed in its report on Friday. The figure was slightly above the estimates of 0.1% growth. The yield on the 2-year Treasury increased to 4.346%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.595%, up about 10 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.568%. The spread between the US 2’s and 10’s narrowed to -75.1bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) narrowed to – 163.2bps. Meanwhile, investors are looking to December consumer inflation in the US, due to be released on Tuesday, in which a pullback is expected in the y/y to 7.3% from 7.7%.

Volatile week for USD

The US Dollar moved higher this week after U.S. producer inflation data for November came in slightly hotter than expected. Specifically, the dollar initially jumped on Friday after U.S. producer prices (PPI) rose 0.3% last month, data showed, above the 0.2% forecast by economists. Therefore, the EURUSD traded higher at 1.0546. Furthermore, the GBPUSD ended the week higher at 1.2273 and the USDJPY traded near 136.46 on Friday. Following a period of high volatility for US Dollar, the United States will announce interest rate decision on Wednesday 14 of December, which is expected to confirm an increase of 0.5 percentage point.

Oil and Gold traded opposite

Gold started the week with losses as investors were concerned over the results of US job sectors. However, Gold traded higher in the middle of the week following concerns about an economic downturn. Gold traded lower at the end of the week as investors are waiting for next week inflation data. Prices of Oil moved lower on Monday, as their concerns about a new rate hike will cause business activity to slow down. Prices of Oil moved lower in the middle of the week, as crude oil inventories declined more than expected to -5.2 millions. However, on Friday, the prices of oil futures increased, due to a possible reduction of production by Moscow. Meanwhile, in the Crude Oil Inventories report on Wednesday, an increase is expected in the number of barrels held by US firms by 4.507M.

Stock indices performance

Key weekly events:

Monday – 12 December 2022

Tuesday – 13 December 2022

Wednesday – 14 December 2022

Thursday – 15 December 2022

Friday – 16 December 2022

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/

January 27th, 2023 by Nikolay Alexandrov

Global markets finished the week mixed

Global markets started the week lower as the European Central Bank’s president Christine Lagarde comments that Eurozone is not done with the inflation and the interest rates will continue to increase. Moreover, investors are concerned that the fresh lockdowns in China could affect the supply chain. In addition, global markets had gains in the middle of the week after inflation in Europe came less than expected and stood at 10% in November. Also, Federal Reserve Chair Jerome Powell suggested the central bank to start slowing the pace of interest hikes from December. This had a positive reaction on the market, with the NSDQ jumping 4% on the day, the 10-year yield moving below 3.70% and the US dollar falling around 1%. The week finished with the strong November jobs report. The U.S. economy added 263,000 jobs last month, more than the 200,000 expected, while the unemployment rate remained at 3.7%. This was considered as bad news as it shows that the jobs market is still resilient on FED’s tightening policy. Furthermore, the Dow Jones gained 0.10% at the closing bell on Friday. The S&P 500 declined by 0.12%. Moreover, the DAX edged up 0.27%. The CAC 40 dropped by 0.17% and the FTSE 100 stood flat at the close.

Treasury yields advanced towards the end of the week

Yields advanced after the better-than-expected nonfarm payroll employment in the United States rose by 263,000. Regardless of Federal Reserve efforts to slow down the pace of interest rates. The yield on the 2-year Treasury increased to 4.352%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.598% down, about 1 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.658%. The spread between the US 2’s and 10’s narrowed to -75.4bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) narrowed to – 168.6bps.

Volatile week for USD

The US Dollar moved lower this week after a Federal Reserve official said rate hikes moved lower. Specifically, the dollar initially jumped on Friday after the hot November jobs report, but then retreated as market concerns prevailed. Therefore, the EURUSD traded higher at 1.0537. Furthermore, the GBPUSD ended the week higher at 1.228 and the USDJPY traded near 134.38 on Friday. Following a period of high volatility for US Dollar, the United States will release Initial Jobless Claims on Thursday 08th of December, which is expected to confirm an increase on Initial Jobless Claims to 230K.

Oil and Gold traded lower towards the end of the week

Gold started the week with losses as investors were concerned over the comments from Federal Reserve regarding the monetary policy. However, Gold traded higher in the middle of the week following a forecast of smaller interest rate hikes by Federal Reserve. Gold traded lower at the end of the week after nonfarm payroll employment in the United States rose by 263,000. Prices of Oil moved higher on Tuesday, after OPEC+ talked for production cut at its December meeting and on the prospects that China could be loosening its COVID-19 restrictions. However, on Friday, the prices of oil futures decreased, ahead of a meeting of the Organization of the Petroleum Exporting Countries and its allies (OPEC+). Meanwhile, in the Crude Oil Inventories report on Wednesday, an increase is expected in the number of barrels held by US firms by 9.822M.

Stock indices performance

Key weekly events:

Monday – 05 December 2022

Tuesday – 06 December 2022

Wednesday – 07 December 2022

Thursday – 08 December 2022

Friday – 09 December 2022

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/